Basel Ii Risk Weighted Assets . Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The main innovation of basel ii in comparison to basel i is that it. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the.

from www.chegg.com

The main innovation of basel ii in comparison to basel i is that it. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the.

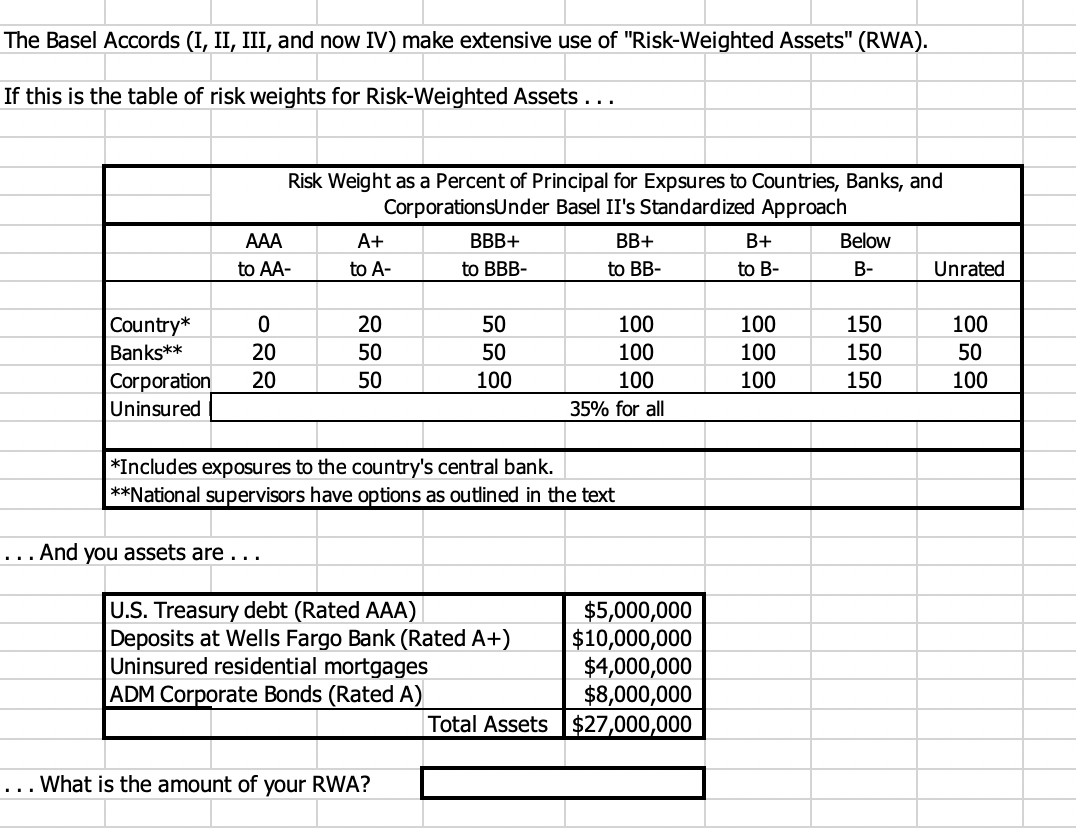

Solved The Basel Accords (I, II, III, and now IV) make

Basel Ii Risk Weighted Assets The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The main innovation of basel ii in comparison to basel i is that it. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk.

From blog.dandkmotorsports.com

Basel 3 Risk Weighted Assets Calculation Blog Dandk Basel Ii Risk Weighted Assets Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according. Basel Ii Risk Weighted Assets.

From www.youtube.com

Risk Weighted Assets RWA under Basel 2 clear explanation with an Excel Basel Ii Risk Weighted Assets The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. The main innovation of basel ii in comparison to basel i is that it. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. This categorisation is applied to measure default. Basel Ii Risk Weighted Assets.

From blog.dandkmotorsports.com

Risk Weighted Assets Calculation Under Basel 3 Blog Dandk Basel Ii Risk Weighted Assets The main innovation of basel ii in comparison to basel i is that it. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. The basel risk weight functions. Basel Ii Risk Weighted Assets.

From www.slideshare.net

Basel II Risk Weighted Assets 2011 Basel Ii Risk Weighted Assets The main innovation of basel ii in comparison to basel i is that it. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the.. Basel Ii Risk Weighted Assets.

From www.slideshare.net

Basel II Risk Weighted Assets 2011 Basel Ii Risk Weighted Assets The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The main innovation of basel ii in comparison to basel i is that it. The basel framework. Basel Ii Risk Weighted Assets.

From www.slideserve.com

PPT Risk Weighted Asset calculation under BASEL PowerPoint Basel Ii Risk Weighted Assets Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. This categorisation is applied to. Basel Ii Risk Weighted Assets.

From www.slideserve.com

PPT Risk Weighted Asset calculation under BASEL PowerPoint Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The main innovation of basel ii in comparison to basel i is that it. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold.. Basel Ii Risk Weighted Assets.

From www.scribd.com

Understanding the Internal Capital Adequacy Assessment Process and Key Basel Ii Risk Weighted Assets The main innovation of basel ii in comparison to basel i is that it. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The basel framework describes how to calculate. Basel Ii Risk Weighted Assets.

From www.federalreserve.gov

Basel II Capital Accord Notice of proposed rulemaking (NPR Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. The. Basel Ii Risk Weighted Assets.

From www.slideshare.net

Basel II Risk Weighted Assets 2011 Basel Ii Risk Weighted Assets Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The main innovation of basel ii in comparison to basel i is that it. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. The basel framework describes how to calculate. Basel Ii Risk Weighted Assets.

From www.slideserve.com

PPT Risk Weighted Asset calculation under BASEL PowerPoint Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The main innovation of basel ii in comparison to basel i is that it.. Basel Ii Risk Weighted Assets.

From www.chegg.com

Solved The Basel Accords (I, II, III, and now IV) make Basel Ii Risk Weighted Assets Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The basel framework describes how to calculate rwa for credit risk, market risk and. Basel Ii Risk Weighted Assets.

From www.scribd.com

Basel II Risk Weight Functions PDF Basel Ii Risk Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The basel framework describes how to calculate rwa for credit risk, market risk and. Basel Ii Risk Weighted Assets.

From www.wallstreetmojo.com

RiskWeighted Asset Definition, Formula, Examples, Advantages Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. The. Basel Ii Risk Weighted Assets.

From www.researchgate.net

Basel II risk weights and credit assessments Download Scientific Diagram Basel Ii Risk Weighted Assets Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. The main innovation of basel ii in comparison to basel i is that it. This categorisation is applied to measure default risk, with. Basel Ii Risk Weighted Assets.

From www.slideshare.net

Basel II Risk Weighted Assets 2011 PPT Basel Ii Risk Weighted Assets The main innovation of basel ii in comparison to basel i is that it. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. This categorisation is applied to measure default risk, with. Basel Ii Risk Weighted Assets.

From www.slideshare.net

Basel II Risk Weighted Assets 2011 Basel Ii Risk Weighted Assets Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. This categorisation is applied to. Basel Ii Risk Weighted Assets.

From www.clarusft.com

Capital Ratios and Risk Weighted Assets for Tier 1 US Banks Basel Ii Risk Weighted Assets The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. This categorisation is applied to. Basel Ii Risk Weighted Assets.

From www.researchgate.net

Risk weight table for bank exposures in the Basel II framework under Basel Ii Risk Weighted Assets Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The main innovation of basel ii in comparison to basel i is that it.. Basel Ii Risk Weighted Assets.

From www.slideshare.net

Basel II Risk Weighted Assets 2011 Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. The. Basel Ii Risk Weighted Assets.

From www.investopedia.com

RiskWeighted Assets Definition and Place in Basel III Basel Ii Risk Weighted Assets The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. The main innovation of basel ii in comparison to basel i is that it. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The basel framework describes how to calculate. Basel Ii Risk Weighted Assets.

From www.researchgate.net

Credit Assessments and Corresponding Risk Weights under Basel I, II Basel Ii Risk Weighted Assets The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. The main innovation of basel ii in comparison to basel i is that it. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. This categorisation is applied to measure default risk, with assets being ranked. Basel Ii Risk Weighted Assets.

From www.slideserve.com

PPT Risk Weighted Asset calculation under BASEL PowerPoint Basel Ii Risk Weighted Assets Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according. Basel Ii Risk Weighted Assets.

From www.slideserve.com

PPT Risk Weighted Asset calculation under BASEL PowerPoint Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The main innovation of basel ii in comparison to basel i is that it. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold.. Basel Ii Risk Weighted Assets.

From en.ppt-online.org

Capital adequacy BASEL 2 and BASEL 3 online presentation Basel Ii Risk Weighted Assets The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The main innovation of basel ii in comparison to basel i is that it. Risk weighting is. Basel Ii Risk Weighted Assets.

From blog.dandkmotorsports.com

Basel 3 Risk Weighted Assets Blog Dandk Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets. Basel Ii Risk Weighted Assets.

From www.slideserve.com

PPT Risk Weighted Asset calculation under BASEL PowerPoint Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The main innovation of basel ii in comparison to basel i is that it. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. The basel risk weight functions. Basel Ii Risk Weighted Assets.

From www.slideshare.net

RiskWeighted Assets Example For Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The main innovation of basel ii in comparison to basel i is that it. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. Risk weighting is. Basel Ii Risk Weighted Assets.

From www.scribd.com

Accenture The New Importance of Risk Weighted Assets Across Europe PDF Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets. Basel Ii Risk Weighted Assets.

From www.slideserve.com

PPT Risk Weighted Asset calculation under BASEL PowerPoint Basel Ii Risk Weighted Assets Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The main innovation of basel ii in comparison to basel i is that it. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the.. Basel Ii Risk Weighted Assets.

From www.slideshare.net

Albel pres basel II quick review Basel Ii Risk Weighted Assets The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The. Basel Ii Risk Weighted Assets.

From en.ppt-online.org

Capital adequacy Basel 2. Financial institutions management kimep Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. Risk. Basel Ii Risk Weighted Assets.

From financeunlocked.com

What are Risk Weighted Assets? Finance Unlocked Basel Ii Risk Weighted Assets The basel framework describes how to calculate rwa for credit risk, market risk and operational risk. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. This categorisation is applied to. Basel Ii Risk Weighted Assets.

From www.youtube.com

Credit risk in Basel III Riskweighted assets explained (Excel) YouTube Basel Ii Risk Weighted Assets The main innovation of basel ii in comparison to basel i is that it. The basel risk weight functions used for the derivation of supervisory capital charges for unexpected losses (ul) are. This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The basel framework. Basel Ii Risk Weighted Assets.

From en.ppt-online.org

Capital adequacy BASEL 2 and BASEL 3 online presentation Basel Ii Risk Weighted Assets This categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and 100%) according to the. The main innovation of basel ii in comparison to basel i is that it. Risk weighting is intended to discourage banks from taking on excessive amounts of risk in terms of the assets they hold.. Basel Ii Risk Weighted Assets.