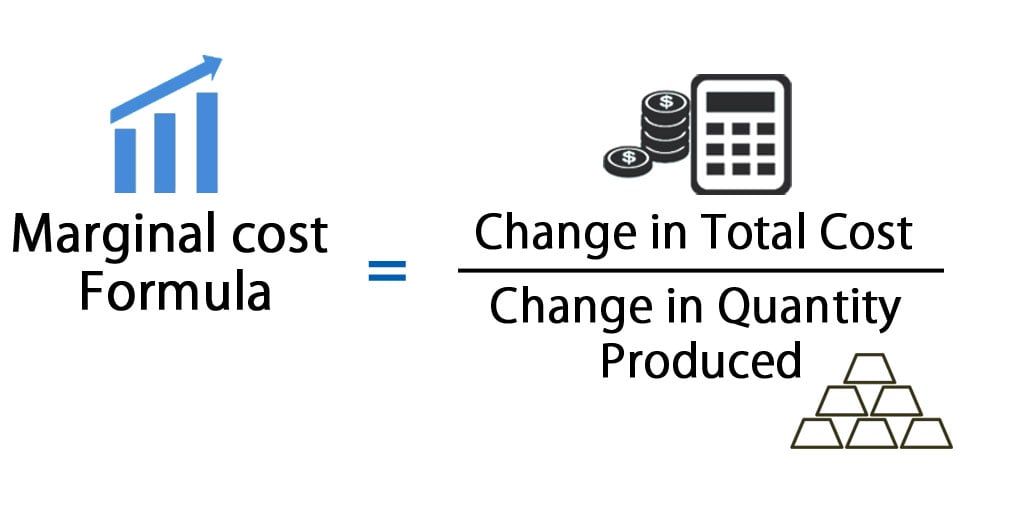

Marginal Cost Is A Change In . Change in total production cost (before and after the production increase) and. Marginal cost is an economics term that refers to the incremental cost of producing one additional unit of a product or service. The marginal cost of production is an economic concept that describes the increase in total production cost when producing one more unit of a good. The formula is the change in total cost divided by. In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. It equals the slope of the total cost curve/function or the total. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. To calculate marginal cost, a business must first calculate the formula’s two variables: Marginal cost is the change in: It is highly useful to. Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output.

from www.educba.com

It is highly useful to. It equals the slope of the total cost curve/function or the total. Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. Marginal cost is the change in: Marginal cost is an economics term that refers to the incremental cost of producing one additional unit of a product or service. Change in total production cost (before and after the production increase) and. The marginal cost of production is an economic concept that describes the increase in total production cost when producing one more unit of a good. To calculate marginal cost, a business must first calculate the formula’s two variables: The formula is the change in total cost divided by. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service.

Marginal Cost Formula Calculator (Excel template)

Marginal Cost Is A Change In Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. It equals the slope of the total cost curve/function or the total. Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. The formula is the change in total cost divided by. Marginal cost is an economics term that refers to the incremental cost of producing one additional unit of a product or service. Change in total production cost (before and after the production increase) and. It is highly useful to. Marginal cost is the change in: The marginal cost of production is an economic concept that describes the increase in total production cost when producing one more unit of a good. To calculate marginal cost, a business must first calculate the formula’s two variables: Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service.

From synder.com

How to Calculate Marginal Cost Marginal Cost Formula Marginal Cost Is A Change In It equals the slope of the total cost curve/function or the total. The marginal cost of production is an economic concept that describes the increase in total production cost when producing one more unit of a good. In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. The formula. Marginal Cost Is A Change In.

From www.slideserve.com

PPT Cost PowerPoint Presentation, free download ID1514088 Marginal Cost Is A Change In In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. It equals the slope of the total cost curve/function or the total. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. Marginal cost is an economics term that refers to. Marginal Cost Is A Change In.

From www.alamy.com

3D illustration of a graph of cost as a function of quantity, with the Marginal Cost Is A Change In Marginal cost is an economics term that refers to the incremental cost of producing one additional unit of a product or service. To calculate marginal cost, a business must first calculate the formula’s two variables: It equals the slope of the total cost curve/function or the total. Marginal cost refers to the extra expense incurred for producing an additional unit. Marginal Cost Is A Change In.

From analystprep.com

Marginal Cost of Capital Schedule CFA Level 1 AnalystPrep Marginal Cost Is A Change In To calculate marginal cost, a business must first calculate the formula’s two variables: The marginal cost of production is an economic concept that describes the increase in total production cost when producing one more unit of a good. Marginal cost is an economics term that refers to the incremental cost of producing one additional unit of a product or service.. Marginal Cost Is A Change In.

From www.tutor2u.net

Oligopoly Kinked Demand Curve Economics tutor2u Marginal Cost Is A Change In To calculate marginal cost, a business must first calculate the formula’s two variables: Change in total production cost (before and after the production increase) and. Marginal cost is the change in: Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. Marginal cost refers to the extra expense incurred. Marginal Cost Is A Change In.

From www.margincalculator.net

Marginal Cost Calculator Marginal Cost Is A Change In In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. The formula is the change in total cost divided by. Change in total production cost (before and after the production increase) and. Marginal cost is the change in: Marginal cost is an economics term that refers to the incremental. Marginal Cost Is A Change In.

From www.slideserve.com

PPT Cost PowerPoint Presentation, free download ID5717240 Marginal Cost Is A Change In To calculate marginal cost, a business must first calculate the formula’s two variables: It equals the slope of the total cost curve/function or the total. It is highly useful to. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. Marginal cost is an economics term that refers to the incremental cost. Marginal Cost Is A Change In.

From www.chegg.com

Solved Marginal cost is defined as the change in fixed cost Marginal Cost Is A Change In To calculate marginal cost, a business must first calculate the formula’s two variables: It is highly useful to. It equals the slope of the total cost curve/function or the total. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. The marginal cost of production is an economic concept that describes the. Marginal Cost Is A Change In.

From webapi.bu.edu

🏷️ Relationship between total cost average cost and marginal cost Marginal Cost Is A Change In Marginal cost is an economics term that refers to the incremental cost of producing one additional unit of a product or service. It equals the slope of the total cost curve/function or the total. To calculate marginal cost, a business must first calculate the formula’s two variables: Marginal cost refers to the extra expense incurred for producing an additional unit. Marginal Cost Is A Change In.

From javier-well-patel.blogspot.com

Marginal Costs and Marginal Benefits Are Used to Describe Marginal Cost Is A Change In Marginal cost is an economics term that refers to the incremental cost of producing one additional unit of a product or service. Marginal cost is the change in: The marginal cost of production is an economic concept that describes the increase in total production cost when producing one more unit of a good. It equals the slope of the total. Marginal Cost Is A Change In.

From www.educba.com

Marginal Cost Formula Calculator (Excel template) Marginal Cost Is A Change In Marginal cost is the change in: To calculate marginal cost, a business must first calculate the formula’s two variables: In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in. Marginal Cost Is A Change In.

From haipernews.com

How To Calculate Marginal Cost Haiper Marginal Cost Is A Change In The marginal cost of production is an economic concept that describes the increase in total production cost when producing one more unit of a good. Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. In economics, the marginal cost is the change in the total cost that arises. Marginal Cost Is A Change In.

From tsort.info

Marginal Cost Marginal Cost Is A Change In Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. It is highly useful to. To calculate marginal cost, a business must first calculate the formula’s two variables: Change in total production cost (before and after the production increase) and. Marginal cost refers to the extra expense incurred for. Marginal Cost Is A Change In.

From www.chegg.com

Solved Marginal cost is thechange in average variable cost Marginal Cost Is A Change In Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. Change in total production cost (before and after the production increase) and. In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. The marginal cost of production is. Marginal Cost Is A Change In.

From www.slideserve.com

PPT Management in the Built Environment Lesson 5 PRODUCTION Marginal Cost Is A Change In To calculate marginal cost, a business must first calculate the formula’s two variables: Marginal cost is an economics term that refers to the incremental cost of producing one additional unit of a product or service. Marginal cost is the change in: It is highly useful to. Marginal cost refers to the extra expense incurred for producing an additional unit of. Marginal Cost Is A Change In.

From hmhub.in

Marginal Cost Breakeven Analysis hmhub Marginal Cost Is A Change In The marginal cost of production is an economic concept that describes the increase in total production cost when producing one more unit of a good. To calculate marginal cost, a business must first calculate the formula’s two variables: Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. It equals the slope. Marginal Cost Is A Change In.

From www.studocu.com

Chapter 4 Marginal Cost Chapter 4 Marginal Cost Definition Marginal Marginal Cost Is A Change In To calculate marginal cost, a business must first calculate the formula’s two variables: Marginal cost is the change in: Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. The marginal. Marginal Cost Is A Change In.

From saylordotorg.github.io

Why Do Prices Change? Marginal Cost Is A Change In Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. Marginal cost is the change in: It equals the slope of the total cost curve/function or the total. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. To calculate marginal. Marginal Cost Is A Change In.

From www.myaccountingcourse.com

What is a Marginal Cost? Definition Meaning Example Marginal Cost Is A Change In Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. Change in total production cost (before and after the production increase) and. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. To calculate marginal cost, a business must first calculate. Marginal Cost Is A Change In.

From www.chegg.com

Solved Marginal cost is defined as the change in total Marginal Cost Is A Change In In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. Marginal cost is an economics term that refers to the incremental cost of producing one additional unit of a product or service. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or. Marginal Cost Is A Change In.

From www.slideserve.com

PPT Theory of Cost PowerPoint Presentation, free download ID4217040 Marginal Cost Is A Change In Change in total production cost (before and after the production increase) and. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. It equals the slope of the total cost curve/function. Marginal Cost Is A Change In.

From quickbooks.intuit.com

Marginal cost and revenue Formulas, definitions, and howto guide Marginal Cost Is A Change In It equals the slope of the total cost curve/function or the total. It is highly useful to. In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. To calculate marginal cost, a business must first calculate the formula’s two variables: Change in total production cost (before and after the. Marginal Cost Is A Change In.

From quickbooks.intuit.com

Marginal cost and revenue Formulas, definitions, and howto guide Marginal Cost Is A Change In In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. Change in total production cost (before and after the production increase) and. To calculate marginal cost, a business. Marginal Cost Is A Change In.

From www.investopedia.com

Marginal Cost Meaning, Formula, and Examples Marginal Cost Is A Change In Change in total production cost (before and after the production increase) and. It equals the slope of the total cost curve/function or the total. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. The formula is the change in total cost divided by. In economics, the marginal cost is the change. Marginal Cost Is A Change In.

From saylordotorg.github.io

Why Do Prices Change? Marginal Cost Is A Change In Change in total production cost (before and after the production increase) and. To calculate marginal cost, a business must first calculate the formula’s two variables: It equals the slope of the total cost curve/function or the total. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. It is highly useful to.. Marginal Cost Is A Change In.

From caambition.com

Marginal cost CA Ambition Marginal Cost Is A Change In Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. Marginal cost is the change in: Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. Change in total production cost (before and after the production increase) and. In economics, the. Marginal Cost Is A Change In.

From analystprep.com

Price, Marginal Cost, Marginal Revenue, Economic Profit, and the Marginal Cost Is A Change In Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. It is highly useful to. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. The marginal cost of production is an economic concept that describes the increase in total production. Marginal Cost Is A Change In.

From www.scribd.com

Assignment1 Marginal Cost Is The Difference (Or Change) in Cost of A Marginal Cost Is A Change In It equals the slope of the total cost curve/function or the total. Marginal cost is the change in: In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. Marginal cost is. Marginal Cost Is A Change In.

From corporatefinanceinstitute.com

Marginal Cost Formula Definition, Examples, Calculate Marginal Cost Marginal Cost Is A Change In In economics, the marginal cost is the change in the total cost that arises when the quantity produced is increased, i.e. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. It equals the slope of the total cost curve/function or the total. Change in total production cost (before and after the. Marginal Cost Is A Change In.

From www.researchgate.net

Effect of a change in average marginal costs on the number of firms Marginal Cost Is A Change In Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. Change in total production cost (before and after the production increase) and. Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. It equals the slope of the total cost curve/function. Marginal Cost Is A Change In.

From www.wikihow.com

How to Find Marginal Cost 11 Steps (with Pictures) wikiHow Marginal Cost Is A Change In Change in total production cost (before and after the production increase) and. Marginal cost is the change in: The formula is the change in total cost divided by. To calculate marginal cost, a business must first calculate the formula’s two variables: It equals the slope of the total cost curve/function or the total. Marginal cost is an economics term that. Marginal Cost Is A Change In.

From www.allassignmenthelp.co.uk

Marginal Cost Meaning with Example and Feature Marginal Cost Is A Change In Marginal cost is the change in: Marginal cost is an economics term that refers to the incremental cost of producing one additional unit of a product or service. Change in total production cost (before and after the production increase) and. Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in. Marginal Cost Is A Change In.

From www.wikihow.com

How to Calculate Marginal Cost 9 Steps (with Pictures) wikiHow Marginal Cost Is A Change In It is highly useful to. To calculate marginal cost, a business must first calculate the formula’s two variables: Change in total production cost (before and after the production increase) and. The marginal cost of production is an economic concept that describes the increase in total production cost when producing one more unit of a good. The formula is the change. Marginal Cost Is A Change In.

From medium.com

Understanding Marginal Costs. A Hopefully Not Too Economic… by Tony Marginal Cost Is A Change In The formula is the change in total cost divided by. Marginal cost refers to the extra expense incurred for producing an additional unit of a product or service. Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. The marginal cost of production is an economic concept that describes. Marginal Cost Is A Change In.

From www.careerprinciples.com

Marginal Cost Definition, Formula, and Examples Marginal Cost Is A Change In Marginal cost is the change in total cost (or total variable cost) in response to a one unit change in output. It equals the slope of the total cost curve/function or the total. The formula is the change in total cost divided by. Marginal cost is the change in: It is highly useful to. Marginal cost is an economics term. Marginal Cost Is A Change In.