Linear Interpolation Zero Rates . It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. Specifically, the interest rates for cash flows are determined. Suppose that you interpolate your zero curve, i.e. Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. The smoothness of a rate curve is to be measured on the smoothness of its. As you can see from the. A (poor) common choice is to interpolate (linearly) on zero rates. We use the following linear interpolation formula for this purpose: Because ac is linear, that is, a. To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the passed.

from www.chegg.com

Specifically, the interest rates for cash flows are determined. Because ac is linear, that is, a. The smoothness of a rate curve is to be measured on the smoothness of its. It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. A (poor) common choice is to interpolate (linearly) on zero rates. As you can see from the. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the passed. We use the following linear interpolation formula for this purpose: To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. Suppose that you interpolate your zero curve, i.e.

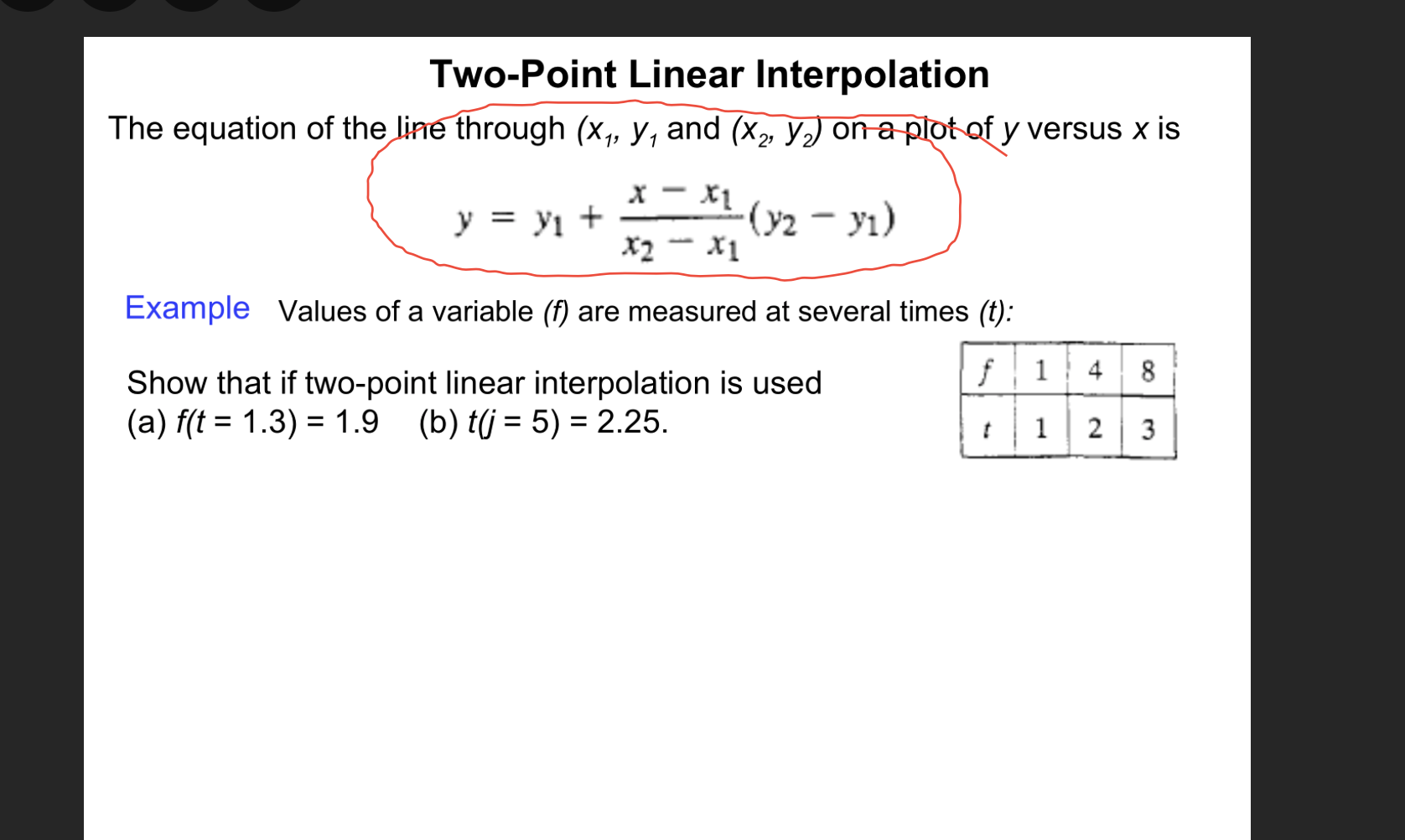

Solved TwoPoint Linear Interpolation The equation of the

Linear Interpolation Zero Rates To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. Specifically, the interest rates for cash flows are determined. Because ac is linear, that is, a. The smoothness of a rate curve is to be measured on the smoothness of its. A (poor) common choice is to interpolate (linearly) on zero rates. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the passed. Suppose that you interpolate your zero curve, i.e. Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. As you can see from the. We use the following linear interpolation formula for this purpose: To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates;

From www.researchgate.net

Samples at zero crossing linear interpolation. Download Scientific Linear Interpolation Zero Rates It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; As you can see from the. The smoothness of a rate curve is to be measured on the smoothness of its. To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. A (poor) common choice is to interpolate (linearly) on. Linear Interpolation Zero Rates.

From www.slideserve.com

PPT Image Interpolation PowerPoint Presentation, free download ID Linear Interpolation Zero Rates The smoothness of a rate curve is to be measured on the smoothness of its. A (poor) common choice is to interpolate (linearly) on zero rates. To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates.. Linear Interpolation Zero Rates.

From www.slideserve.com

PPT MA2213 Lecture 2 PowerPoint Presentation, free download ID1160606 Linear Interpolation Zero Rates We use the following linear interpolation formula for this purpose: The smoothness of a rate curve is to be measured on the smoothness of its. As you can see from the. Specifically, the interest rates for cash flows are determined. To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. A (poor) common choice. Linear Interpolation Zero Rates.

From www.researchgate.net

Linear interpolation using landmarks. Download Scientific Diagram Linear Interpolation Zero Rates A (poor) common choice is to interpolate (linearly) on zero rates. As you can see from the. Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; The smoothness of a rate curve is to be measured on. Linear Interpolation Zero Rates.

From www.exceldemy.com

How to Do Linear Interpolation in Excel (7 Handy Methods) ExcelDemy Linear Interpolation Zero Rates A (poor) common choice is to interpolate (linearly) on zero rates. Because ac is linear, that is, a. It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. Specifically, the interest rates for cash flows are determined. It uses theoretical par bond arbitrage and yield interpolation to derive all. Linear Interpolation Zero Rates.

From www.learntospark.com

Linear Interpolation with Machine Learning PySpark Linear Interpolation Zero Rates It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; Suppose that you interpolate your zero curve, i.e. A (poor) common choice is to interpolate (linearly) on zero rates. We use the following linear interpolation formula for this purpose: Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known. Linear Interpolation Zero Rates.

From www.educba.com

Interpolation Formula Example with Excel Template Linear Interpolation Zero Rates Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. A (poor) common choice is to interpolate (linearly) on zero rates. Suppose that you interpolate your zero curve, i.e. Because ac is linear, that is, a. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates. Linear Interpolation Zero Rates.

From studyflix.de

Lineare Interpolation • einfach erklärt · [mit Video] Linear Interpolation Zero Rates It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; Because ac is linear, that is, a. A (poor) common choice is to interpolate (linearly) on zero rates. Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. Suppose that you interpolate your zero curve, i.e. To get. Linear Interpolation Zero Rates.

From ubcmath.github.io

Interpolation — Applied Linear Algebra Linear Interpolation Zero Rates Suppose that you interpolate your zero curve, i.e. Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; The smoothness of a rate curve is to be measured on the smoothness of its. Because ac is linear, that. Linear Interpolation Zero Rates.

From www.researchgate.net

Schematic diagram of linear interpolation. Download Scientific Diagram Linear Interpolation Zero Rates Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. Because ac is linear, that is, a. A (poor) common choice is to interpolate (linearly) on zero rates. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the. Linear Interpolation Zero Rates.

From www.researchgate.net

InterpolationZero momentum Correlation function calculated on samples Linear Interpolation Zero Rates It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the passed. To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. We use the following linear. Linear Interpolation Zero Rates.

From github.com

Linear Interpolation zero values on stacked area · Issue 20818 Linear Interpolation Zero Rates It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. Specifically, the interest rates for cash flows are determined. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the passed. We use the following linear. Linear Interpolation Zero Rates.

From www.youtube.com

Linear and Quadratic Interpolation 002 YouTube Linear Interpolation Zero Rates Suppose that you interpolate your zero curve, i.e. Specifically, the interest rates for cash flows are determined. The smoothness of a rate curve is to be measured on the smoothness of its. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the passed. Because ac is. Linear Interpolation Zero Rates.

From www.chegg.com

Solved TwoPoint Linear Interpolation The equation of the Linear Interpolation Zero Rates The smoothness of a rate curve is to be measured on the smoothness of its. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the passed. Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. Specifically, the. Linear Interpolation Zero Rates.

From github.com

Linear Interpolation zero values on stacked area · Issue 20818 Linear Interpolation Zero Rates The smoothness of a rate curve is to be measured on the smoothness of its. It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. Linear interpolation assumes that the unknown rate (rn) lies on. Linear Interpolation Zero Rates.

From do.mykinsdy.de

💡 lineare interpolation berechnung lineare interpolation tabelle Linear Interpolation Zero Rates Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. As you can see from the. To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. We use the following linear interpolation formula for this purpose: Specifically, the interest rates for cash flows are determined. A. Linear Interpolation Zero Rates.

From general.chemistrysteps.com

Integrated Rate Law Chemistry Steps Linear Interpolation Zero Rates Because ac is linear, that is, a. Suppose that you interpolate your zero curve, i.e. It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the. Linear Interpolation Zero Rates.

From vru.vibrationresearch.com

Interpolation in the Frequency Domain VRU Linear Interpolation Zero Rates A (poor) common choice is to interpolate (linearly) on zero rates. It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should. Linear Interpolation Zero Rates.

From blog.timaios.org

Lineare Interpolation Linear Interpolation Zero Rates It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. Specifically, the interest rates for cash flows are determined. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the passed. Because ac is linear, that. Linear Interpolation Zero Rates.

From www.youtube.com

Linear Interpolation YouTube Linear Interpolation Zero Rates Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. The smoothness of a rate curve is to be measured on the smoothness of its. Specifically, the interest rates for cash flows are determined. Because ac is linear, that is, a. To get a zero rate between pillar dates (benchmark instrument dates). Linear Interpolation Zero Rates.

From studyflix.de

Lineare Interpolation • einfach erklärt · [mit Video] Linear Interpolation Zero Rates It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; We use the following linear interpolation formula for this purpose: It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero. Linear Interpolation Zero Rates.

From ncalculators.com

Linear Interpolation Calculator Linear Interpolation Zero Rates To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; Suppose that you interpolate your zero curve, i.e. Because ac is linear, that is, a. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero. Linear Interpolation Zero Rates.

From www.slideserve.com

PPT Interpolation PowerPoint Presentation, free download ID2735192 Linear Interpolation Zero Rates As you can see from the. Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. Suppose that you interpolate your zero curve, i.e. It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. A (poor) common choice is to interpolate. Linear Interpolation Zero Rates.

From www.youtube.com

Linear Interpolation in Excel YouTube Linear Interpolation Zero Rates Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the passed. Because ac is linear, that is, a. It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; The smoothness of a rate curve is to be measured on the smoothness of. Linear Interpolation Zero Rates.

From www.youtube.com

Internal Rate of Return IRR and Linear Interpolation Engineering Linear Interpolation Zero Rates Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates between nodes given by the maturities of the passed. Because ac is linear, that is, a. Specifically, the interest rates for cash flows are determined. It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; It returns the corresponding discount. Linear Interpolation Zero Rates.

From www.researchgate.net

(a) Schematic illustration of linear interpolation evaluating xα. (b Linear Interpolation Zero Rates To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. Specifically, the interest rates for cash flows are determined. The smoothness of a rate curve is to be measured on the smoothness of its. We use the following linear interpolation formula for this purpose: As you can see from the. Linear interpolation assumes that. Linear Interpolation Zero Rates.

From do.mykinsdy.de

🔥 lineare interpolation online rechner lineare interpolation Linear Interpolation Zero Rates Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. We use the following linear interpolation formula for this purpose: Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the. Linear Interpolation Zero Rates.

From www.bradleysawler.com

Linear Interpolation Using Microsoft Excel Tables Bradley Sawler Linear Interpolation Zero Rates Because ac is linear, that is, a. To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. Crv = ql.piecewiselinearzero(2, ql.target(), deposits + futures + swaps, ql.actual365fixed()) the curve linearly interpolates zero rates. Linear Interpolation Zero Rates.

From studyflix.de

Lineare Interpolation • einfach erklärt · [mit Video] Linear Interpolation Zero Rates We use the following linear interpolation formula for this purpose: To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. Suppose that you interpolate your zero curve, i.e. Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. It uses theoretical par bond arbitrage and yield. Linear Interpolation Zero Rates.

From dobrian.github.io

Introduction to Linear Interpolation and Linear Mapping Linear Interpolation Zero Rates Specifically, the interest rates for cash flows are determined. To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. Because ac is linear, that is, a. We use the following linear interpolation formula for this purpose: The smoothness of a rate curve is to be measured on the smoothness of its. As you can. Linear Interpolation Zero Rates.

From www.cuemath.com

Linear Interpolation Formula Derivation, Formulas, Examples Linear Interpolation Zero Rates Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. As you can see from the. It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. Specifically, the interest rates for cash flows are determined. Crv = ql.piecewiselinearzero(2, ql.target(), deposits +. Linear Interpolation Zero Rates.

From www.geeksforgeeks.org

Linear Interpolation in MATLAB Linear Interpolation Zero Rates Specifically, the interest rates for cash flows are determined. The smoothness of a rate curve is to be measured on the smoothness of its. It uses theoretical par bond arbitrage and yield interpolation to derive all zero rates; Suppose that you interpolate your zero curve, i.e. As you can see from the. We use the following linear interpolation formula for. Linear Interpolation Zero Rates.

From ubcmath.github.io

Interpolation — Applied Linear Algebra Linear Interpolation Zero Rates As you can see from the. A (poor) common choice is to interpolate (linearly) on zero rates. The smoothness of a rate curve is to be measured on the smoothness of its. We use the following linear interpolation formula for this purpose: Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates.. Linear Interpolation Zero Rates.

From studyflix.de

Lineare Interpolation Excel • Anleitung und Beispiel · [mit Video] Linear Interpolation Zero Rates Because ac is linear, that is, a. Specifically, the interest rates for cash flows are determined. The smoothness of a rate curve is to be measured on the smoothness of its. It returns the corresponding discount factors, zero rates, and forward rates for a vector of times that is specified as input. To get a zero rate between pillar dates. Linear Interpolation Zero Rates.

From www.youtube.com

Linear Interpolation Explained What is a linear interpolation? YouTube Linear Interpolation Zero Rates A (poor) common choice is to interpolate (linearly) on zero rates. Linear interpolation assumes that the unknown rate (rn) lies on the line (ac) between the two known rates. To get a zero rate between pillar dates (benchmark instrument dates) linear interpolation should be used. We use the following linear interpolation formula for this purpose: Crv = ql.piecewiselinearzero(2, ql.target(), deposits. Linear Interpolation Zero Rates.