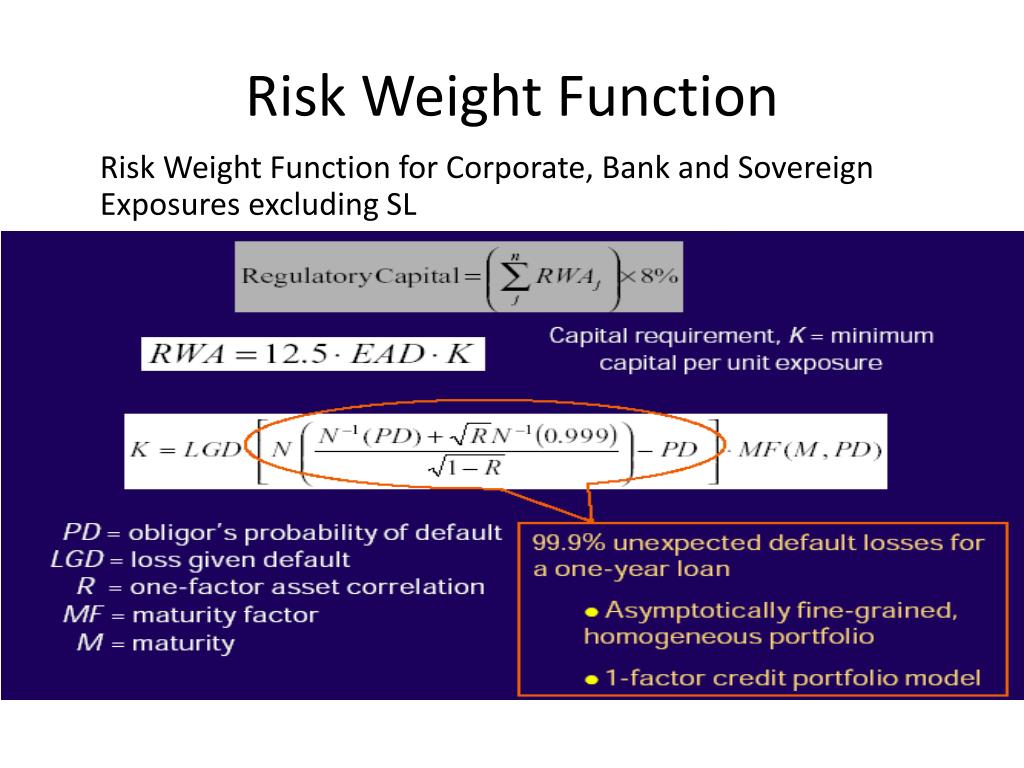

Basel Ii Irb Risk Weight Functions . For corporate exposures in irb, the risk weight function is found in paragraph 156:. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. now consider the risk weight function itself. this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and.

from www.slideserve.com

now consider the risk weight function itself. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. For corporate exposures in irb, the risk weight function is found in paragraph 156:. this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and.

PPT Credit Risk Capital Allocation IRB Approach PowerPoint Presentation ID1657103

Basel Ii Irb Risk Weight Functions we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. now consider the risk weight function itself. this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. For corporate exposures in irb, the risk weight function is found in paragraph 156:.

From www.academia.edu

(PDF) Basel Committee on Banking Supervision An Explanatory Note on the Basel II IRB Risk Weight Basel Ii Irb Risk Weight Functions this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. this note explains the economic foundations and the mathematical model of. Basel Ii Irb Risk Weight Functions.

From www.slideserve.com

PPT The Microeconomic Foundations of Basel II PowerPoint Presentation ID589532 Basel Ii Irb Risk Weight Functions now consider the risk weight function itself. this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. this categorisation is applied. Basel Ii Irb Risk Weight Functions.

From www.researchgate.net

Illustrative Sovereign Risk Weights and Capital Charges Under the Basel... Download Scientific Basel Ii Irb Risk Weight Functions — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%,. Basel Ii Irb Risk Weight Functions.

From www.slideserve.com

PPT The Microeconomic Foundations of Basel II PowerPoint Presentation ID589532 Basel Ii Irb Risk Weight Functions now consider the risk weight function itself. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: For corporate exposures in irb, the risk. Basel Ii Irb Risk Weight Functions.

From analystprep.com

IRB Model CFA, FRM, and Actuarial Exams Study Notes Basel Ii Irb Risk Weight Functions this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. — this paper introduces basel ii, the construction of risk weight functions and their limits in. Basel Ii Irb Risk Weight Functions.

From www.researchgate.net

Credit Assessments and Corresponding Risk Weights under Basel I, II & III Download Table Basel Ii Irb Risk Weight Functions we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. For corporate exposures in irb, the risk weight function is found in paragraph 156:. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: . Basel Ii Irb Risk Weight Functions.

From www.researchgate.net

Basel II risk weights and credit assessments Download Scientific Diagram Basel Ii Irb Risk Weight Functions this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. now consider the risk weight function itself. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. — this paper introduces basel ii, the construction. Basel Ii Irb Risk Weight Functions.

From www.researchgate.net

Risk weight table for bank exposures in the Basel II framework under... Download Scientific Basel Ii Irb Risk Weight Functions now consider the risk weight function itself. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. For corporate exposures in irb, the risk weight function. Basel Ii Irb Risk Weight Functions.

From www.scribd.com

The Basel II IRB Approach For Credit Portfolios PDF Basel Ii Risk Basel Ii Irb Risk Weight Functions this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: now consider the risk weight function itself. we show how the basel ii one factor model which. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Basel 2 Basel Ii Irb Risk Weight Functions For corporate exposures in irb, the risk weight function is found in paragraph 156:. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: we show how the. Basel Ii Irb Risk Weight Functions.

From www.researchgate.net

Capital charges under the Basel II IRB Approach (RBA) Long Term Weights Download Table Basel Ii Irb Risk Weight Functions this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. — this paper introduces basel ii, the construction of risk weight functions. Basel Ii Irb Risk Weight Functions.

From www.youtube.com

Capital Requirement IRB approach A part of Basel 2 YouTube Basel Ii Irb Risk Weight Functions this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. now consider the risk weight function itself. For corporate exposures in irb, the risk weight function. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Basel II IRB Risk Weight Functions Basel Ii Irb Risk Weight Functions now consider the risk weight function itself. For corporate exposures in irb, the risk weight function is found in paragraph 156:. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. this note explains the economic foundations and the mathematical model of. Basel Ii Irb Risk Weight Functions.

From www.federalreserve.gov

Basel II Capital Accord Notice of proposed rulemaking (NPR) Preamble Calculation of Risk Basel Ii Irb Risk Weight Functions — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: now consider the risk weight function itself. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. For corporate exposures in irb, the risk weight function is found. Basel Ii Irb Risk Weight Functions.

From www.semanticscholar.org

Basel Committee on Banking Supervision an Explanatory Note on the Basel Ii Irb Risk Weight Basel Ii Irb Risk Weight Functions now consider the risk weight function itself. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: For corporate exposures in irb, the risk weight function is found. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Developments around basel 2 Basel Ii Irb Risk Weight Functions we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. For corporate exposures in irb, the risk weight function is found in paragraph 156:. now consider the risk weight function itself. — this paper introduces basel ii, the construction of risk weight. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Basel II IRB Risk Weight Functions Basel Ii Irb Risk Weight Functions — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: now consider the risk weight function itself. For corporate exposures in irb, the risk weight function is found in paragraph 156:. we show how the basel ii one factor model which is used to calibrate risk weights can be. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Basel II IRB Risk Weight Functions Basel Ii Irb Risk Weight Functions now consider the risk weight function itself. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. For corporate exposures in irb,. Basel Ii Irb Risk Weight Functions.

From www.slideserve.com

PPT Basel II, Securitization, and Credit Risk PowerPoint Presentation ID496882 Basel Ii Irb Risk Weight Functions this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: For corporate exposures in irb, the risk weight function is found in paragraph 156:. we show how the basel. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Basel II Risk Weighted Assets 2011 Basel Ii Irb Risk Weight Functions now consider the risk weight function itself. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. For corporate exposures in irb, the risk weight function is found in paragraph 156:. this note explains the economic foundations and the mathematical model of. Basel Ii Irb Risk Weight Functions.

From www.researchgate.net

Capital charges under the Basel II IRB Approach (RBA) Long Term Weights Download Table Basel Ii Irb Risk Weight Functions now consider the risk weight function itself. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: this categorisation is applied to measure. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Basel II Risk Weighted Assets 2011 Basel Ii Irb Risk Weight Functions now consider the risk weight function itself. For corporate exposures in irb, the risk weight function is found in paragraph 156:. this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. we show how the basel ii one factor model which is used to calibrate risk weights. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Basel II IRB Risk Weight Functions Basel Ii Irb Risk Weight Functions this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. For corporate exposures in irb, the risk weight function is found in paragraph 156:. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. — this. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Basel II IRB Risk Weight Functions Basel Ii Irb Risk Weight Functions we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. — this paper introduces basel ii, the construction of risk weight. Basel Ii Irb Risk Weight Functions.

From www.slideserve.com

PPT Dealing with double default under Basel II PowerPoint Presentation ID678785 Basel Ii Irb Risk Weight Functions — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. we show how the basel ii one factor model which is used to calibrate risk weights can be extended. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Basel II Risk Weighted Assets 2011 PPT Basel Ii Irb Risk Weight Functions this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. For corporate exposures in irb, the risk weight function is found in paragraph 156:. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: this note explains the. Basel Ii Irb Risk Weight Functions.

From www.semanticscholar.org

Basel Committee on Banking Supervision an Explanatory Note on the Basel Ii Irb Risk Weight Basel Ii Irb Risk Weight Functions this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. For corporate exposures in irb, the risk weight function is found in paragraph 156:. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. now consider. Basel Ii Irb Risk Weight Functions.

From www.slideserve.com

PPT The New Basel Capital Accord Potential Effects on lending rates in New Zealand PowerPoint Basel Ii Irb Risk Weight Functions this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. now consider the risk weight function itself. — this paper introduces basel ii, the construction of risk weight functions and their limits in two sections: For corporate exposures in irb, the risk weight function is found. Basel Ii Irb Risk Weight Functions.

From www.slideserve.com

PPT Credit Risk Capital Allocation IRB Approach PowerPoint Presentation ID1657103 Basel Ii Irb Risk Weight Functions For corporate exposures in irb, the risk weight function is found in paragraph 156:. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Basel II IRB Risk Weight Functions Basel Ii Irb Risk Weight Functions For corporate exposures in irb, the risk weight function is found in paragraph 156:. this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. — this. Basel Ii Irb Risk Weight Functions.

From www.slideserve.com

PPT Credit & Operational Risks Are We Ready For Basel II? PowerPoint Presentation ID4681547 Basel Ii Irb Risk Weight Functions For corporate exposures in irb, the risk weight function is found in paragraph 156:. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. now consider the risk weight function itself. we show how the basel ii one factor model which is used to calibrate risk. Basel Ii Irb Risk Weight Functions.

From www.slideserve.com

PPT Credit & Operational Risks Are We Ready For Basel II? PowerPoint Presentation ID4681547 Basel Ii Irb Risk Weight Functions now consider the risk weight function itself. For corporate exposures in irb, the risk weight function is found in paragraph 156:. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. — this paper introduces basel ii, the construction of risk weight. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Albel pres basel II quick review Basel Ii Irb Risk Weight Functions this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. we show how the basel ii one factor model which is used to calibrate risk weights can be extended to a model for estimating pds. For corporate exposures in irb, the risk weight function is found in. Basel Ii Irb Risk Weight Functions.

From www.semanticscholar.org

Basel Committee on Banking Supervision an Explanatory Note on the Basel Ii Irb Risk Weight Basel Ii Irb Risk Weight Functions this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. For corporate exposures in irb, the risk weight function is found in paragraph 156:. — this. Basel Ii Irb Risk Weight Functions.

From www.slideshare.net

Basel II IRB Risk Weight Functions Basel Ii Irb Risk Weight Functions this note explains the economic foundations and the mathematical model of the basel ii risk weight formulas for credit risk. now consider the risk weight function itself. this categorisation is applied to measure default risk, with assets being ranked in four risk weight buckets (0%, 20%, 50% and. — this paper introduces basel ii, the construction. Basel Ii Irb Risk Weight Functions.