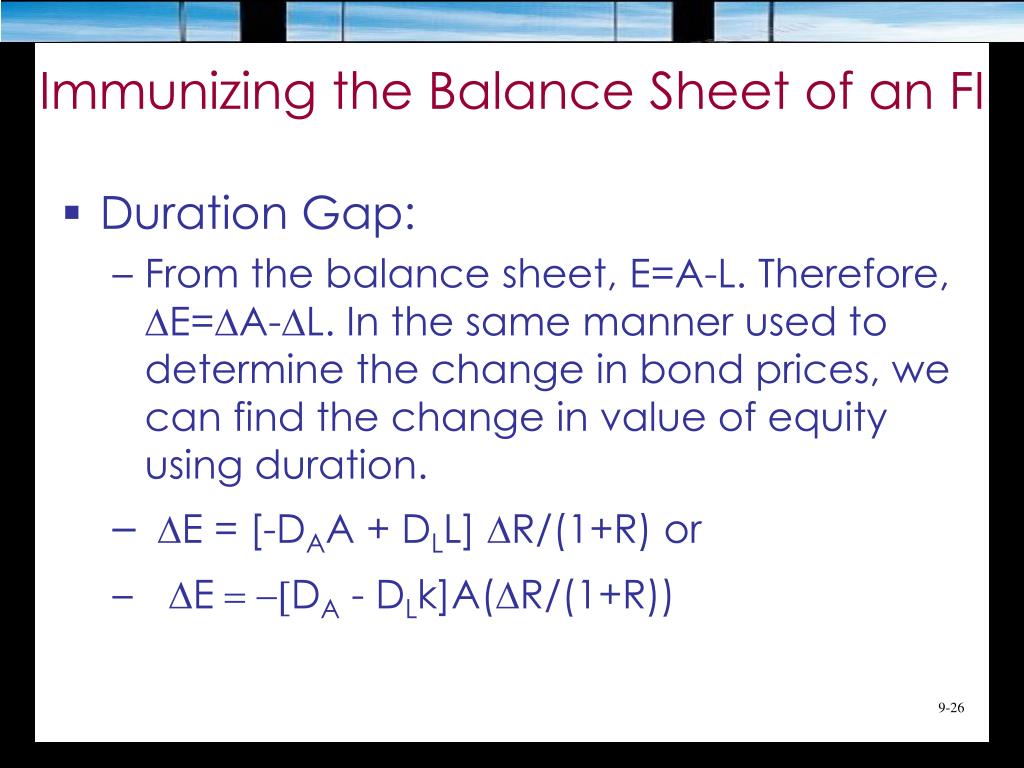

Leverage Adjusted Duration Gap Formula . D a is the duration of assets; The bank manager wants to know what happens when interest rates rise from 10% to 11%. Calculate the duration gap (p.38) important formula: Why only bank needs to use ladg? A zero duration gap tells us that the equity has zero interest rate exposure. This adjustment considers the extent to which the institution uses borrowed funds to finance. Is called duration gap, d gap. D l is the duration of liabilities; Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g.

from www.slideserve.com

This adjustment considers the extent to which the institution uses borrowed funds to finance. A zero duration gap tells us that the equity has zero interest rate exposure. Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. D l is the duration of liabilities; Is called duration gap, d gap. Calculate the duration gap (p.38) important formula: Why only bank needs to use ladg? The bank manager wants to know what happens when interest rates rise from 10% to 11%. D a is the duration of assets;

PPT Overview PowerPoint Presentation, free download ID2963080

Leverage Adjusted Duration Gap Formula Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. This adjustment considers the extent to which the institution uses borrowed funds to finance. Calculate the duration gap (p.38) important formula: The bank manager wants to know what happens when interest rates rise from 10% to 11%. A zero duration gap tells us that the equity has zero interest rate exposure. Is called duration gap, d gap. D l is the duration of liabilities; Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. D a is the duration of assets; Why only bank needs to use ladg?

From www.slideserve.com

PPT Hedging Interest Rate R isk PowerPoint Presentation, free Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: The bank manager wants to know what happens when interest rates rise from 10% to 11%. This adjustment considers the extent to which the institution uses borrowed funds to finance. D a is the duration of assets; Why only bank needs to use ladg? D l is the duration of liabilities; A zero. Leverage Adjusted Duration Gap Formula.

From www.slideserve.com

PPT Chapter 9 part B Portfolio Immunization Using Duration PowerPoint Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: This adjustment considers the extent to which the institution uses borrowed funds to finance. D l is the duration of liabilities; Is called duration gap, d gap. A zero duration gap tells us that the equity has zero interest rate exposure. Why only bank needs to use ladg? D a is the duration. Leverage Adjusted Duration Gap Formula.

From www.youtube.com

Duration Gap calculation in Excel YouTube Leverage Adjusted Duration Gap Formula This adjustment considers the extent to which the institution uses borrowed funds to finance. D l is the duration of liabilities; Is called duration gap, d gap. D a is the duration of assets; Calculate the duration gap (p.38) important formula: Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded. Leverage Adjusted Duration Gap Formula.

From www.numerade.com

SOLVED A bank with total assets of 271 million and equity of31 million Leverage Adjusted Duration Gap Formula D a is the duration of assets; A zero duration gap tells us that the equity has zero interest rate exposure. Calculate the duration gap (p.38) important formula: Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. D l is the duration of liabilities; This adjustment considers. Leverage Adjusted Duration Gap Formula.

From www.slideserve.com

PPT Hedging Interest Rate R isk PowerPoint Presentation, free Leverage Adjusted Duration Gap Formula Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. The bank manager wants to know what happens when interest rates rise from 10% to 11%. Why only bank needs to use ladg? Calculate the duration gap (p.38) important formula: D a is the duration of assets; Is. Leverage Adjusted Duration Gap Formula.

From www.slideshare.net

Duration model Leverage Adjusted Duration Gap Formula Is called duration gap, d gap. Why only bank needs to use ladg? A zero duration gap tells us that the equity has zero interest rate exposure. The bank manager wants to know what happens when interest rates rise from 10% to 11%. D a is the duration of assets; Calculate the duration gap (p.38) important formula: D l is. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

Solved What is State Bank’s leverage adjusted duration gap? Leverage Adjusted Duration Gap Formula Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. D a is the duration of assets; This adjustment considers the extent to which the institution uses borrowed funds to finance. The bank manager wants to know what happens when interest rates rise from 10% to 11%. D. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

Solved What is the leverageadjusted duration gap? Third Leverage Adjusted Duration Gap Formula D a is the duration of assets; Why only bank needs to use ladg? The bank manager wants to know what happens when interest rates rise from 10% to 11%. Is called duration gap, d gap. Calculate the duration gap (p.38) important formula: D l is the duration of liabilities; A zero duration gap tells us that the equity has. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

Solved 1. Calculate the leverageadjusted duration gap Leverage Adjusted Duration Gap Formula Why only bank needs to use ladg? This adjustment considers the extent to which the institution uses borrowed funds to finance. Calculate the duration gap (p.38) important formula: A zero duration gap tells us that the equity has zero interest rate exposure. Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

Solved Calculate the leveraged adjusted duration gap of this Leverage Adjusted Duration Gap Formula Why only bank needs to use ladg? D a is the duration of assets; Calculate the duration gap (p.38) important formula: Is called duration gap, d gap. This adjustment considers the extent to which the institution uses borrowed funds to finance. Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded. Leverage Adjusted Duration Gap Formula.

From www.slideserve.com

PPT Chapter 6 PowerPoint Presentation, free download ID4021126 Leverage Adjusted Duration Gap Formula Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. Calculate the duration gap (p.38) important formula: Why only bank needs to use ladg? D l is the duration of liabilities; Is called duration gap, d gap. This adjustment considers the extent to which the institution uses borrowed. Leverage Adjusted Duration Gap Formula.

From www.coursehero.com

[Solved] a. Calculate the leverageadjusted duration gap of an FI that Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: This adjustment considers the extent to which the institution uses borrowed funds to finance. D l is the duration of liabilities; Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. D a is the duration of assets; The bank manager. Leverage Adjusted Duration Gap Formula.

From www.coursehero.com

[Solved] a. Calculate the leverageadjusted duration gap of an FI that Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: The bank manager wants to know what happens when interest rates rise from 10% to 11%. This adjustment considers the extent to which the institution uses borrowed funds to finance. Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. A. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

Solved vestion 24 ot yet swered Second Derivatives, a Leverage Adjusted Duration Gap Formula D l is the duration of liabilities; Calculate the duration gap (p.38) important formula: Why only bank needs to use ladg? Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. This adjustment considers the extent to which the institution uses borrowed funds to finance. D a is. Leverage Adjusted Duration Gap Formula.

From www.slideserve.com

PPT Chapter 6 PowerPoint Presentation, free download ID4021126 Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: Is called duration gap, d gap. D a is the duration of assets; A zero duration gap tells us that the equity has zero interest rate exposure. This adjustment considers the extent to which the institution uses borrowed funds to finance. Adjusted duration gap = duration gap da — gdl where dl is. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

Solved Consider the following. a. Calculate the Leverage Adjusted Duration Gap Formula D l is the duration of liabilities; Calculate the duration gap (p.38) important formula: D a is the duration of assets; Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. Is called duration gap, d gap. Why only bank needs to use ladg? A zero duration gap. Leverage Adjusted Duration Gap Formula.

From www.youtube.com

How to Calculate Leverage Ratio in Excel YouTube Leverage Adjusted Duration Gap Formula D l is the duration of liabilities; Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. D a is the duration of assets; Calculate the duration gap (p.38) important formula: The bank manager wants to know what happens when interest rates rise from 10% to 11%. A. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

Solved Question 1 Calculate the leverageadjusted duration Leverage Adjusted Duration Gap Formula Is called duration gap, d gap. Calculate the duration gap (p.38) important formula: Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. Why only bank needs to use ladg? D a is the duration of assets; D l is the duration of liabilities; This adjustment considers the. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

1. Calculate the leverageadjusted duration gap Leverage Adjusted Duration Gap Formula D a is the duration of assets; The bank manager wants to know what happens when interest rates rise from 10% to 11%. Why only bank needs to use ladg? Calculate the duration gap (p.38) important formula: Is called duration gap, d gap. This adjustment considers the extent to which the institution uses borrowed funds to finance. D l is. Leverage Adjusted Duration Gap Formula.

From slideplayer.com

Interest Rate Risk II Chapter 9 © 2006 The McGrawHill Companies, Inc Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: D l is the duration of liabilities; A zero duration gap tells us that the equity has zero interest rate exposure. Why only bank needs to use ladg? The bank manager wants to know what happens when interest rates rise from 10% to 11%. This adjustment considers the extent to which the institution. Leverage Adjusted Duration Gap Formula.

From www.slideserve.com

PPT Interest Rate Risk II Chapter 9 PowerPoint Presentation, free Leverage Adjusted Duration Gap Formula Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. Is called duration gap, d gap. Why only bank needs to use ladg? Calculate the duration gap (p.38) important formula: This adjustment considers the extent to which the institution uses borrowed funds to finance. D a is the. Leverage Adjusted Duration Gap Formula.

From www.slideserve.com

PPT The duration gap model and clumping PowerPoint Presentation, free Leverage Adjusted Duration Gap Formula D a is the duration of assets; The bank manager wants to know what happens when interest rates rise from 10% to 11%. Is called duration gap, d gap. This adjustment considers the extent to which the institution uses borrowed funds to finance. Why only bank needs to use ladg? A zero duration gap tells us that the equity has. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

1What is the leverageadjusted duration gap of your Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: The bank manager wants to know what happens when interest rates rise from 10% to 11%. D a is the duration of assets; Is called duration gap, d gap. This adjustment considers the extent to which the institution uses borrowed funds to finance. Adjusted duration gap = duration gap da — gdl where. Leverage Adjusted Duration Gap Formula.

From www.youtube.com

Managing Interest Rate Risk Duration Gap Analysis YouTube Leverage Adjusted Duration Gap Formula Why only bank needs to use ladg? D a is the duration of assets; Calculate the duration gap (p.38) important formula: A zero duration gap tells us that the equity has zero interest rate exposure. The bank manager wants to know what happens when interest rates rise from 10% to 11%. Adjusted duration gap = duration gap da — gdl. Leverage Adjusted Duration Gap Formula.

From www.slideserve.com

PPT Chapter 6 PowerPoint Presentation, free download ID4021126 Leverage Adjusted Duration Gap Formula Why only bank needs to use ladg? D a is the duration of assets; Is called duration gap, d gap. This adjustment considers the extent to which the institution uses borrowed funds to finance. Calculate the duration gap (p.38) important formula: Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded. Leverage Adjusted Duration Gap Formula.

From www.slideserve.com

PPT Interest Rate Risk and ALM PowerPoint Presentation, free download Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. This adjustment considers the extent to which the institution uses borrowed funds to finance. D l is the duration of liabilities; Is called duration gap, d gap. A zero duration gap. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

Solved Consider the following.a. Calculate the Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: D l is the duration of liabilities; This adjustment considers the extent to which the institution uses borrowed funds to finance. A zero duration gap tells us that the equity has zero interest rate exposure. The bank manager wants to know what happens when interest rates rise from 10% to 11%. D a. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

Solved Question 1 Calculate the leverageadjusted duration Leverage Adjusted Duration Gap Formula D l is the duration of liabilities; Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. D a is the duration of assets; Calculate the duration gap (p.38) important formula: Is called duration gap, d gap. The bank manager wants to know what happens when interest rates. Leverage Adjusted Duration Gap Formula.

From www.numerade.com

SOLVED Consider the following a. Calculate the leverageadjusted Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: This adjustment considers the extent to which the institution uses borrowed funds to finance. D a is the duration of assets; Is called duration gap, d gap. Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. Why only bank needs. Leverage Adjusted Duration Gap Formula.

From www.chegg.com

Solved SHOW THE WORK a) Find leverageadjusted duration Leverage Adjusted Duration Gap Formula Why only bank needs to use ladg? The bank manager wants to know what happens when interest rates rise from 10% to 11%. Is called duration gap, d gap. Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. D l is the duration of liabilities; D a. Leverage Adjusted Duration Gap Formula.

From slideplayer.com

Tutorial. Measuring Interest Rate Risk ppt download Leverage Adjusted Duration Gap Formula Why only bank needs to use ladg? D a is the duration of assets; Is called duration gap, d gap. Calculate the duration gap (p.38) important formula: Adjusted duration gap = duration gap da — gdl where dl is adjusted for the proportion of assets funded by liabilities (e.g. A zero duration gap tells us that the equity has zero. Leverage Adjusted Duration Gap Formula.

From www.slideserve.com

PPT Overview PowerPoint Presentation, free download ID2963080 Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: Why only bank needs to use ladg? D l is the duration of liabilities; Is called duration gap, d gap. D a is the duration of assets; A zero duration gap tells us that the equity has zero interest rate exposure. This adjustment considers the extent to which the institution uses borrowed funds. Leverage Adjusted Duration Gap Formula.

From www.slideserve.com

PPT Fin 603 Week 5 PowerPoint Presentation, free download ID3028928 Leverage Adjusted Duration Gap Formula D l is the duration of liabilities; Calculate the duration gap (p.38) important formula: D a is the duration of assets; The bank manager wants to know what happens when interest rates rise from 10% to 11%. This adjustment considers the extent to which the institution uses borrowed funds to finance. A zero duration gap tells us that the equity. Leverage Adjusted Duration Gap Formula.

From www.slideserve.com

PPT Interest Rate Risk PowerPoint Presentation, free download ID794991 Leverage Adjusted Duration Gap Formula D l is the duration of liabilities; Calculate the duration gap (p.38) important formula: A zero duration gap tells us that the equity has zero interest rate exposure. Why only bank needs to use ladg? This adjustment considers the extent to which the institution uses borrowed funds to finance. D a is the duration of assets; Adjusted duration gap =. Leverage Adjusted Duration Gap Formula.

From www.poems.com.sg

Leverage ratio POEMS Leverage Adjusted Duration Gap Formula Calculate the duration gap (p.38) important formula: A zero duration gap tells us that the equity has zero interest rate exposure. D a is the duration of assets; The bank manager wants to know what happens when interest rates rise from 10% to 11%. Why only bank needs to use ladg? This adjustment considers the extent to which the institution. Leverage Adjusted Duration Gap Formula.