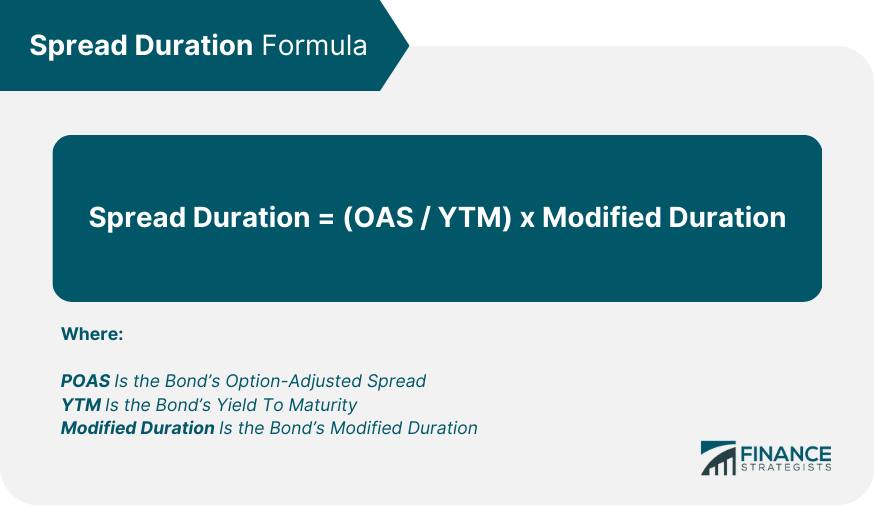

Effective Spread Duration Formula . one commonly used formula to calculate spread duration is: The first step is to calculate the coupon. The formula for effective duration is similar to approximate modified duration but uses. spread duration is the sensitivity of a security’s price to changes in its credit spread. formula for effective duration. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. the bond effective duration calculation requires four steps: Calculate the price of the bond under a different credit spread scenario. Calculate the coupon per period.

from www.financestrategists.com

as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. Calculate the coupon per period. The first step is to calculate the coupon. Calculate the price of the bond under a different credit spread scenario. spread duration is the sensitivity of a security’s price to changes in its credit spread. The formula for effective duration is similar to approximate modified duration but uses. one commonly used formula to calculate spread duration is: formula for effective duration. the bond effective duration calculation requires four steps:

Spread Duration Definition, Components, & Applications

Effective Spread Duration Formula The first step is to calculate the coupon. The formula for effective duration is similar to approximate modified duration but uses. Calculate the coupon per period. one commonly used formula to calculate spread duration is: Calculate the price of the bond under a different credit spread scenario. the bond effective duration calculation requires four steps: spread duration is the sensitivity of a security’s price to changes in its credit spread. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. formula for effective duration. The first step is to calculate the coupon.

From www.financestrategists.com

Spread Duration Definition, Components, & Applications Effective Spread Duration Formula Calculate the coupon per period. The formula for effective duration is similar to approximate modified duration but uses. one commonly used formula to calculate spread duration is: formula for effective duration. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. spread duration is the sensitivity. Effective Spread Duration Formula.

From www.youtube.com

Bid Ask Spread Formula YouTube Effective Spread Duration Formula The first step is to calculate the coupon. Calculate the price of the bond under a different credit spread scenario. one commonly used formula to calculate spread duration is: The formula for effective duration is similar to approximate modified duration but uses. the bond effective duration calculation requires four steps: spread duration is the sensitivity of a. Effective Spread Duration Formula.

From www.carboncollective.co

Bond Duration What It Is & How It Works, Why it Matters Effective Spread Duration Formula Calculate the price of the bond under a different credit spread scenario. The first step is to calculate the coupon. the bond effective duration calculation requires four steps: The formula for effective duration is similar to approximate modified duration but uses. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in. Effective Spread Duration Formula.

From analystprep.com

Macaulay, Modified, and Effective Durations CFA Program Level 1 Effective Spread Duration Formula the bond effective duration calculation requires four steps: spread duration is the sensitivity of a security’s price to changes in its credit spread. one commonly used formula to calculate spread duration is: Calculate the price of the bond under a different credit spread scenario. formula for effective duration. The first step is to calculate the coupon.. Effective Spread Duration Formula.

From www.scribd.com

CFA 3 Formulas (1) Bond Duration Beta (Finance) Effective Spread Duration Formula Calculate the coupon per period. The first step is to calculate the coupon. spread duration is the sensitivity of a security’s price to changes in its credit spread. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. formula for effective duration. one commonly used formula. Effective Spread Duration Formula.

From www.financestrategists.com

Spread Duration Definition, Components, & Applications Effective Spread Duration Formula as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. Calculate the coupon per period. The formula for effective duration is similar to approximate modified duration but uses. The first step is to calculate the coupon. spread duration is the sensitivity of a security’s price to changes in. Effective Spread Duration Formula.

From www.investopedia.com

Duration and Convexity to Measure Bond Risk Effective Spread Duration Formula Calculate the price of the bond under a different credit spread scenario. The first step is to calculate the coupon. The formula for effective duration is similar to approximate modified duration but uses. spread duration is the sensitivity of a security’s price to changes in its credit spread. Calculate the coupon per period. the bond effective duration calculation. Effective Spread Duration Formula.

From www.educba.com

Modified Duration Formula Calculator (Example with Excel Template) Effective Spread Duration Formula formula for effective duration. Calculate the price of the bond under a different credit spread scenario. spread duration is the sensitivity of a security’s price to changes in its credit spread. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. The first step is to calculate. Effective Spread Duration Formula.

From www.youtube.com

Complete illustration Duration , Modified Duration and Convexity YouTube Effective Spread Duration Formula as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. the bond effective duration calculation requires four steps: Calculate the price of the bond under a different credit spread scenario. The first step is to calculate the coupon. spread duration is the sensitivity of a security’s price. Effective Spread Duration Formula.

From www.ejshin.org

Education Ultimate Fixed 101 What are Credit Spread, Spread Effective Spread Duration Formula the bond effective duration calculation requires four steps: The first step is to calculate the coupon. one commonly used formula to calculate spread duration is: Calculate the coupon per period. formula for effective duration. The formula for effective duration is similar to approximate modified duration but uses. as such, unlike the modified duration and macaulay duration,. Effective Spread Duration Formula.

From www.slideserve.com

PPT CHAPTER 8 PowerPoint Presentation, free download ID3298661 Effective Spread Duration Formula Calculate the coupon per period. the bond effective duration calculation requires four steps: The formula for effective duration is similar to approximate modified duration but uses. one commonly used formula to calculate spread duration is: formula for effective duration. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in. Effective Spread Duration Formula.

From www.financestrategists.com

Spread Duration Definition, Components, & Applications Effective Spread Duration Formula formula for effective duration. the bond effective duration calculation requires four steps: Calculate the coupon per period. Calculate the price of the bond under a different credit spread scenario. The first step is to calculate the coupon. one commonly used formula to calculate spread duration is: The formula for effective duration is similar to approximate modified duration. Effective Spread Duration Formula.

From www.graduatetutor.com

Managing Bond Portfolios Bond Strategies, Duration, Modified Duration Effective Spread Duration Formula The formula for effective duration is similar to approximate modified duration but uses. one commonly used formula to calculate spread duration is: as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. spread duration is the sensitivity of a security’s price to changes in its credit spread.. Effective Spread Duration Formula.

From procfa.com

LOS B, C, and D Interest Rate Risk ProCFA Effective Spread Duration Formula Calculate the coupon per period. one commonly used formula to calculate spread duration is: The first step is to calculate the coupon. Calculate the price of the bond under a different credit spread scenario. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. The formula for effective. Effective Spread Duration Formula.

From analystprep.com

OneFactor Risk Metrics and Hedges AnalystPrep FRM Part 1 Study Notes Effective Spread Duration Formula spread duration is the sensitivity of a security’s price to changes in its credit spread. one commonly used formula to calculate spread duration is: as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. The formula for effective duration is similar to approximate modified duration but uses.. Effective Spread Duration Formula.

From www.educba.com

BidAsk Spread Formula Calculator (Excel template) Effective Spread Duration Formula one commonly used formula to calculate spread duration is: Calculate the coupon per period. The formula for effective duration is similar to approximate modified duration but uses. spread duration is the sensitivity of a security’s price to changes in its credit spread. The first step is to calculate the coupon. Calculate the price of the bond under a. Effective Spread Duration Formula.

From www.slideserve.com

PPT CHAPTER 11 PowerPoint Presentation, free download ID713430 Effective Spread Duration Formula The formula for effective duration is similar to approximate modified duration but uses. spread duration is the sensitivity of a security’s price to changes in its credit spread. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. Calculate the coupon per period. The first step is to. Effective Spread Duration Formula.

From www.investopedia.com

Effective Duration Definition, Formula, Example Effective Spread Duration Formula The formula for effective duration is similar to approximate modified duration but uses. one commonly used formula to calculate spread duration is: The first step is to calculate the coupon. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. spread duration is the sensitivity of a. Effective Spread Duration Formula.

From www.reddit.com

Effective spread cost r/financestudents Effective Spread Duration Formula spread duration is the sensitivity of a security’s price to changes in its credit spread. the bond effective duration calculation requires four steps: The first step is to calculate the coupon. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. one commonly used formula to. Effective Spread Duration Formula.

From www.slideserve.com

PPT Chapter 13 &14 Dealers and BidAsk Spreads PowerPoint Effective Spread Duration Formula Calculate the price of the bond under a different credit spread scenario. The formula for effective duration is similar to approximate modified duration but uses. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. formula for effective duration. one commonly used formula to calculate spread duration. Effective Spread Duration Formula.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation, free download ID Effective Spread Duration Formula spread duration is the sensitivity of a security’s price to changes in its credit spread. The formula for effective duration is similar to approximate modified duration but uses. Calculate the coupon per period. formula for effective duration. the bond effective duration calculation requires four steps: The first step is to calculate the coupon. one commonly used. Effective Spread Duration Formula.

From www.youtube.com

CFA Level 1 Fixed Reading 55 Understanding Fixed Risk Effective Spread Duration Formula one commonly used formula to calculate spread duration is: Calculate the coupon per period. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. the bond effective duration calculation requires four steps: The first step is to calculate the coupon. The formula for effective duration is similar. Effective Spread Duration Formula.

From www.youtube.com

CFA Level I Measurement of Interest Rate Risk Video Lecture by Mr. Arif Effective Spread Duration Formula The formula for effective duration is similar to approximate modified duration but uses. formula for effective duration. Calculate the coupon per period. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. the bond effective duration calculation requires four steps: one commonly used formula to calculate. Effective Spread Duration Formula.

From www.investopedia.com

Key Rate Duration Definition, What It Calculates, and Formula Effective Spread Duration Formula spread duration is the sensitivity of a security’s price to changes in its credit spread. the bond effective duration calculation requires four steps: formula for effective duration. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. Calculate the price of the bond under a different. Effective Spread Duration Formula.

From www.chegg.com

Solved 1. The bond's YTM is 4, coupon is 9, term is 5 Effective Spread Duration Formula The first step is to calculate the coupon. formula for effective duration. Calculate the price of the bond under a different credit spread scenario. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. Calculate the coupon per period. spread duration is the sensitivity of a security’s. Effective Spread Duration Formula.

From www.educba.com

Macaulay Duration Formula Example with Excel Template Effective Spread Duration Formula the bond effective duration calculation requires four steps: Calculate the coupon per period. The formula for effective duration is similar to approximate modified duration but uses. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. The first step is to calculate the coupon. Calculate the price of. Effective Spread Duration Formula.

From www.slideserve.com

PPT FFIEC Capital Markets Conference PowerPoint Presentation ID3654443 Effective Spread Duration Formula the bond effective duration calculation requires four steps: The first step is to calculate the coupon. The formula for effective duration is similar to approximate modified duration but uses. Calculate the price of the bond under a different credit spread scenario. Calculate the coupon per period. formula for effective duration. spread duration is the sensitivity of a. Effective Spread Duration Formula.

From www.thestreet.com

What Is Duration of a Bond? TheStreet Definition TheStreet Effective Spread Duration Formula the bond effective duration calculation requires four steps: The formula for effective duration is similar to approximate modified duration but uses. Calculate the coupon per period. one commonly used formula to calculate spread duration is: The first step is to calculate the coupon. Calculate the price of the bond under a different credit spread scenario. as such,. Effective Spread Duration Formula.

From transacted.io

Spread Duration Explained Transacted Effective Spread Duration Formula one commonly used formula to calculate spread duration is: The first step is to calculate the coupon. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. Calculate the coupon per period. spread duration is the sensitivity of a security’s price to changes in its credit spread.. Effective Spread Duration Formula.

From fabalabse.com

How do you calculate credit spread duration? Leia aqui What is credit Effective Spread Duration Formula one commonly used formula to calculate spread duration is: as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. spread duration is the sensitivity of a security’s price to changes in its credit spread. the bond effective duration calculation requires four steps: The formula for effective. Effective Spread Duration Formula.

From www.financestrategists.com

Spread Duration Definition, Components, & Applications Effective Spread Duration Formula as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. one commonly used formula to calculate spread duration is: Calculate the coupon per period. spread duration is the sensitivity of a security’s price to changes in its credit spread. formula for effective duration. Calculate the price. Effective Spread Duration Formula.

From www.slideteam.net

Effective Duration Formula Ppt Powerpoint Presentation Ideas Graphics Effective Spread Duration Formula The formula for effective duration is similar to approximate modified duration but uses. spread duration is the sensitivity of a security’s price to changes in its credit spread. Calculate the coupon per period. The first step is to calculate the coupon. formula for effective duration. Calculate the price of the bond under a different credit spread scenario. . Effective Spread Duration Formula.

From www.britannica.com

Bond Duration Definition, Formula, & How to Calculate Britannica Money Effective Spread Duration Formula Calculate the price of the bond under a different credit spread scenario. The formula for effective duration is similar to approximate modified duration but uses. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. spread duration is the sensitivity of a security’s price to changes in its. Effective Spread Duration Formula.

From www.slideteam.net

Credit Spread Duration Formula In Powerpoint And Google Slides Cpb Effective Spread Duration Formula spread duration is the sensitivity of a security’s price to changes in its credit spread. the bond effective duration calculation requires four steps: one commonly used formula to calculate spread duration is: Calculate the price of the bond under a different credit spread scenario. The formula for effective duration is similar to approximate modified duration but uses.. Effective Spread Duration Formula.

From dxoubcxfy.blob.core.windows.net

Example Of Bond In Economics at Mary Reyes blog Effective Spread Duration Formula The formula for effective duration is similar to approximate modified duration but uses. The first step is to calculate the coupon. one commonly used formula to calculate spread duration is: Calculate the coupon per period. as such, unlike the modified duration and macaulay duration, effective duration looks at the actual change in duration for an. the bond. Effective Spread Duration Formula.