How To Find Equilibrium Price And Quantity In Monopoly . By the end of this section, you will be able to: Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. It may be regarded as the marginal cost curve for the industry. The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. Profit maximisation occurs where mr=mc. Explain the perceived demand curve for a perfect competitor and a monopoly. Analyze a demand curve for a monopoly and. A typical firm with marginal cost curve mc is a. In a monopoly, the price is set above marginal cost and the firm earns a positive.

from www.tutor2u.net

Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. In a monopoly, the price is set above marginal cost and the firm earns a positive. It may be regarded as the marginal cost curve for the industry. By the end of this section, you will be able to: Analyze a demand curve for a monopoly and. Explain the perceived demand curve for a perfect competitor and a monopoly. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. A typical firm with marginal cost curve mc is a. Profit maximisation occurs where mr=mc.

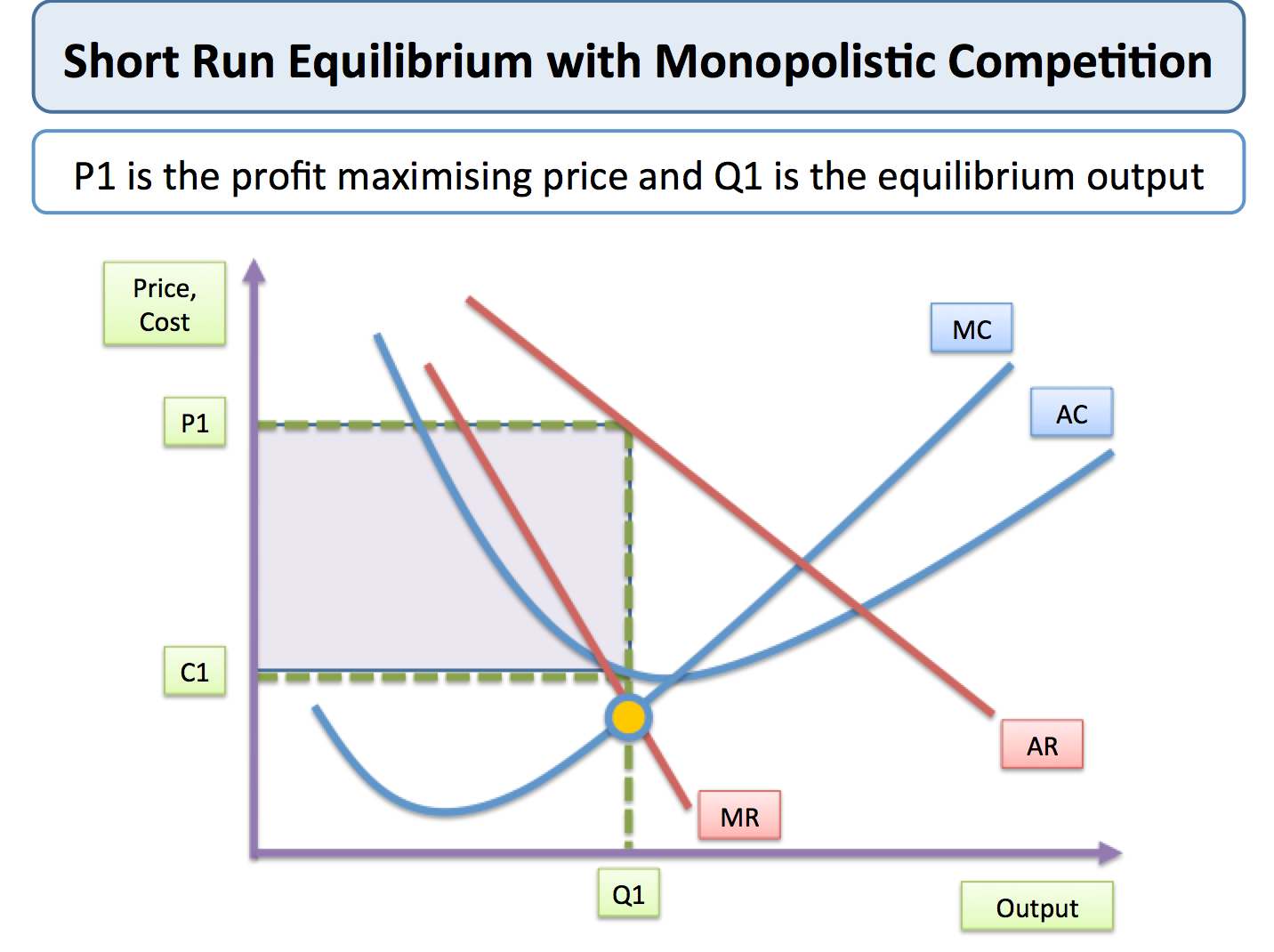

Monopolistic Competition tutor2u Economics

How To Find Equilibrium Price And Quantity In Monopoly Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. In a monopoly, the price is set above marginal cost and the firm earns a positive. It may be regarded as the marginal cost curve for the industry. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. By the end of this section, you will be able to: A typical firm with marginal cost curve mc is a. Analyze a demand curve for a monopoly and. Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. Explain the perceived demand curve for a perfect competitor and a monopoly. Profit maximisation occurs where mr=mc.

From courses.lumenlearning.com

Equilibrium, Price, and Quantity Introduction to Business How To Find Equilibrium Price And Quantity In Monopoly In a monopoly, the price is set above marginal cost and the firm earns a positive. Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. Panel (a) shows. How To Find Equilibrium Price And Quantity In Monopoly.

From www.youtube.com

Supply And Demand Finding Equilibrium Quantity And Price YouTube How To Find Equilibrium Price And Quantity In Monopoly Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. Analyze a demand curve for a monopoly and. Profit maximisation occurs where mr=mc. Explain the perceived demand curve for a perfect competitor and a monopoly. A typical firm. How To Find Equilibrium Price And Quantity In Monopoly.

From econs20.classes.andrewheiss.com

Monopolies Microeconomics How To Find Equilibrium Price And Quantity In Monopoly A typical firm with marginal cost curve mc is a. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. It may be regarded as the marginal cost curve for the industry. Explain the perceived demand curve for a perfect competitor and a monopoly. By the end of this section, you will be. How To Find Equilibrium Price And Quantity In Monopoly.

From www.youtube.com

Finding equilibrium price and quantity YouTube How To Find Equilibrium Price And Quantity In Monopoly Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. A typical firm with marginal cost curve mc is a. Explain the perceived demand curve for a perfect competitor and a monopoly. By the end of this section, you will be able to: Profit maximisation occurs where mr=mc. The diagram for. How To Find Equilibrium Price And Quantity In Monopoly.

From www.youtube.com

find equilibrium price and quantity from a given demand and cost How To Find Equilibrium Price And Quantity In Monopoly By the end of this section, you will be able to: Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. Explain the perceived demand curve for a perfect competitor and a monopoly. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. A. How To Find Equilibrium Price And Quantity In Monopoly.

From www.youtube.com

Finding equilibrium price and quantity using linear demand and supply How To Find Equilibrium Price And Quantity In Monopoly It may be regarded as the marginal cost curve for the industry. Analyze a demand curve for a monopoly and. By the end of this section, you will be able to: A typical firm with marginal cost curve mc is a. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. Use this equilibrium quantity. How To Find Equilibrium Price And Quantity In Monopoly.

From thismatter.com

Pure Monopoly Demand, Revenue and Costs, Price Determination, Profit How To Find Equilibrium Price And Quantity In Monopoly Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. In a monopoly, the price is set above marginal cost and the firm earns a positive. By the end of this section, you will be able to: Explain the perceived demand curve for a perfect competitor and a monopoly. Use this equilibrium quantity with the. How To Find Equilibrium Price And Quantity In Monopoly.

From procfa.com

Market Equilibrium ProCFA How To Find Equilibrium Price And Quantity In Monopoly It may be regarded as the marginal cost curve for the industry. By the end of this section, you will be able to: Explain the perceived demand curve for a perfect competitor and a monopoly. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. Analyze a demand curve for a monopoly and. A typical. How To Find Equilibrium Price And Quantity In Monopoly.

From quiznutritions.z13.web.core.windows.net

How To Calculate Monopoly Price And Quantity How To Find Equilibrium Price And Quantity In Monopoly Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. By the end of this section, you will be able to: A typical firm with marginal cost curve mc is a. The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. Explain the. How To Find Equilibrium Price And Quantity In Monopoly.

From courses.lumenlearning.com

Equilibrium, Price, and Quantity Introduction to Business How To Find Equilibrium Price And Quantity In Monopoly The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. Analyze a demand curve for a. How To Find Equilibrium Price And Quantity In Monopoly.

From rowwhole3.gitlab.io

How To Fix Equilibrium Rowwhole3 How To Find Equilibrium Price And Quantity In Monopoly Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. It may be regarded as the marginal cost curve for the industry. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. Profit maximisation occurs where mr=mc. Panel (a) shows the determination of equilibrium. How To Find Equilibrium Price And Quantity In Monopoly.

From www.tutor2u.net

Changes in Market Equilibrium Price tutor2u Economics How To Find Equilibrium Price And Quantity In Monopoly In a monopoly, the price is set above marginal cost and the firm earns a positive. Profit maximisation occurs where mr=mc. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. A typical firm with marginal cost curve. How To Find Equilibrium Price And Quantity In Monopoly.

From sites.google.com

What is a Monopoly YKK Zipper How To Find Equilibrium Price And Quantity In Monopoly Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. Profit maximisation occurs where mr=mc. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. In a monopoly, the. How To Find Equilibrium Price And Quantity In Monopoly.

From corporatefinanceinstitute.com

Equilibrium Quantity Overview, Supply and Demand How To Find Equilibrium Price And Quantity In Monopoly Explain the perceived demand curve for a perfect competitor and a monopoly. Analyze a demand curve for a monopoly and. Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. A typical firm with marginal cost curve mc is a. The diagram for a monopoly is generally considered to be the. How To Find Equilibrium Price And Quantity In Monopoly.

From www.chegg.com

Solved 1. The equilibrium price and quantity before the How To Find Equilibrium Price And Quantity In Monopoly It may be regarded as the marginal cost curve for the industry. In a monopoly, the price is set above marginal cost and the firm earns a positive. Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. By the end of this section, you will be able to: Explain the. How To Find Equilibrium Price And Quantity In Monopoly.

From www.economicshelp.org

Oligopoly Diagram Economics Help How To Find Equilibrium Price And Quantity In Monopoly It may be regarded as the marginal cost curve for the industry. Profit maximisation occurs where mr=mc. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. Explain the perceived demand curve for a perfect competitor. How To Find Equilibrium Price And Quantity In Monopoly.

From www.youtube.com

Simple concept to determine equilibrium price and quantity for given How To Find Equilibrium Price And Quantity In Monopoly Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. Analyze a demand curve for a monopoly and. In a monopoly, the price is set above marginal cost and the firm earns a positive. It may be regarded. How To Find Equilibrium Price And Quantity In Monopoly.

From www.opentextbooks.org.hk

Monopoly Open Textbooks for Hong Kong How To Find Equilibrium Price And Quantity In Monopoly By the end of this section, you will be able to: Analyze a demand curve for a monopoly and. It may be regarded as the marginal cost curve for the industry. Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. In a monopoly, the price is set above marginal cost. How To Find Equilibrium Price And Quantity In Monopoly.

From www.youtube.com

How to Calculate Market Equilibrium (NO GRAPHING) Think Econ YouTube How To Find Equilibrium Price And Quantity In Monopoly Analyze a demand curve for a monopoly and. Explain the perceived demand curve for a perfect competitor and a monopoly. By the end of this section, you will be able to: Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. Profit maximisation occurs where mr=mc. In a monopoly, the price is set above marginal. How To Find Equilibrium Price And Quantity In Monopoly.

From www.tutor2u.net

Monopolistic Competition tutor2u Economics How To Find Equilibrium Price And Quantity In Monopoly Profit maximisation occurs where mr=mc. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. In a monopoly, the price is set above marginal cost and the firm earns a positive. A typical firm with marginal cost curve mc is a. Explain the perceived demand curve for a perfect competitor and a monopoly.. How To Find Equilibrium Price And Quantity In Monopoly.

From www.enotes.com

Explain how the longrun equilibrium under oligopoly differs from that How To Find Equilibrium Price And Quantity In Monopoly Explain the perceived demand curve for a perfect competitor and a monopoly. In a monopoly, the price is set above marginal cost and the firm earns a positive. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. It may be regarded as the marginal cost curve for the industry. Use this equilibrium quantity with. How To Find Equilibrium Price And Quantity In Monopoly.

From articles.outlier.org

Predicting Changes in Equilibrium Price and Quantity Outlier How To Find Equilibrium Price And Quantity In Monopoly Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. In a monopoly, the price is set above marginal. How To Find Equilibrium Price And Quantity In Monopoly.

From passnownow.com

SS1 Economics Third Term Equilibrium Price/Price Determination How To Find Equilibrium Price And Quantity In Monopoly Analyze a demand curve for a monopoly and. In a perfectly competitive market, price equals marginal cost and firms earn an economic profit of zero. It may be regarded as the marginal cost curve for the industry. In a monopoly, the price is set above marginal cost and the firm earns a positive. By the end of this section, you. How To Find Equilibrium Price And Quantity In Monopoly.

From childhealthpolicy.vumc.org

🐈 Determine the equilibrium price and quantity. How to Find Equilibrium How To Find Equilibrium Price And Quantity In Monopoly By the end of this section, you will be able to: The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. Analyze a demand curve for a monopoly and. A typical firm with. How To Find Equilibrium Price And Quantity In Monopoly.

From www.chegg.com

Solved Solve for the equilibrium price and quantity. Show How To Find Equilibrium Price And Quantity In Monopoly Explain the perceived demand curve for a perfect competitor and a monopoly. A typical firm with marginal cost curve mc is a. Profit maximisation occurs where mr=mc. By the end of this section, you will be able to: Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. Analyze a demand. How To Find Equilibrium Price And Quantity In Monopoly.

From www.youtube.com

How to Calculate Equilibrium Price and Quantity (Demand and Supply How To Find Equilibrium Price And Quantity In Monopoly Profit maximisation occurs where mr=mc. The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. It may be regarded as the marginal cost curve for the industry. In a monopoly, the price is. How To Find Equilibrium Price And Quantity In Monopoly.

From articles.outlier.org

Predicting Changes in Equilibrium Price and Quantity Outlier How To Find Equilibrium Price And Quantity In Monopoly The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. Analyze a demand curve for a monopoly and. Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. Panel (a) shows the determination of equilibrium price and output in. How To Find Equilibrium Price And Quantity In Monopoly.

From www.geeksforgeeks.org

LongRun Equilibrium under Perfect, Monopolistic, and Monopoly Market How To Find Equilibrium Price And Quantity In Monopoly By the end of this section, you will be able to: In a monopoly, the price is set above marginal cost and the firm earns a positive. A typical firm with marginal cost curve mc is a. Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. Explain the perceived demand. How To Find Equilibrium Price And Quantity In Monopoly.

From www.youtube.com

How to find equilibrium price and quantity for a monopoly YouTube How To Find Equilibrium Price And Quantity In Monopoly A typical firm with marginal cost curve mc is a. Explain the perceived demand curve for a perfect competitor and a monopoly. In a monopoly, the price is set above marginal cost and the firm earns a positive. Profit maximisation occurs where mr=mc. By the end of this section, you will be able to: Analyze a demand curve for a. How To Find Equilibrium Price And Quantity In Monopoly.

From quiznutritions.z13.web.core.windows.net

How To Calculate Monopoly Price And Quantity How To Find Equilibrium Price And Quantity In Monopoly By the end of this section, you will be able to: The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. Explain the perceived demand curve for a perfect competitor and a monopoly.. How To Find Equilibrium Price And Quantity In Monopoly.

From www.youtube.com

IB Economics How To Calculate The Equilibrium Quantity And Price How To Find Equilibrium Price And Quantity In Monopoly In a monopoly, the price is set above marginal cost and the firm earns a positive. A typical firm with marginal cost curve mc is a. It may be regarded as the marginal cost curve for the industry. Explain the perceived demand curve for a perfect competitor and a monopoly. In a perfectly competitive market, price equals marginal cost and. How To Find Equilibrium Price And Quantity In Monopoly.

From analystprep.com

Longrun Equilibrium Under Each Market Structure AnalystPrep CFA How To Find Equilibrium Price And Quantity In Monopoly In a monopoly, the price is set above marginal cost and the firm earns a positive. A typical firm with marginal cost curve mc is a. Explain the perceived demand curve for a perfect competitor and a monopoly. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. Use this equilibrium quantity with the demand. How To Find Equilibrium Price And Quantity In Monopoly.

From 2012books.lardbucket.org

The Foundations of Business How To Find Equilibrium Price And Quantity In Monopoly Use this equilibrium quantity with the demand function to figure out what the price paid by the consumer is. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. In a perfectly competitive. How To Find Equilibrium Price And Quantity In Monopoly.

From www.slideserve.com

PPT Monopoly PowerPoint Presentation, free download ID5172804 How To Find Equilibrium Price And Quantity In Monopoly The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. A typical firm with marginal cost curve mc is a. By the end of this section, you will be able to: Profit maximisation occurs where mr=mc. In a monopoly, the price is set above marginal cost and the. How To Find Equilibrium Price And Quantity In Monopoly.

From www.intelligenteconomist.com

Monopoly Market Structure Intelligent Economist How To Find Equilibrium Price And Quantity In Monopoly The diagram for a monopoly is generally considered to be the same in the short run as well as the long run. It may be regarded as the marginal cost curve for the industry. Analyze a demand curve for a monopoly and. Panel (a) shows the determination of equilibrium price and output in a perfectly competitive market. In a perfectly. How To Find Equilibrium Price And Quantity In Monopoly.