Spread Duration Of A Bond . Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity to. If one bond yields 7% and another one yields 4%, the. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. The yield spread is a key metric that bond investors use when gauging the level of expense for a bond or group of bonds. Spread duration is the sensitivity of a security’s price to changes in its credit spread. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Duration can also be used to measure how sensitive the.

from www.babypips.com

Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. The yield spread is a key metric that bond investors use when gauging the level of expense for a bond or group of bonds. Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity to. Duration can also be used to measure how sensitive the. If one bond yields 7% and another one yields 4%, the. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is the sensitivity of a security’s price to changes in its credit spread.

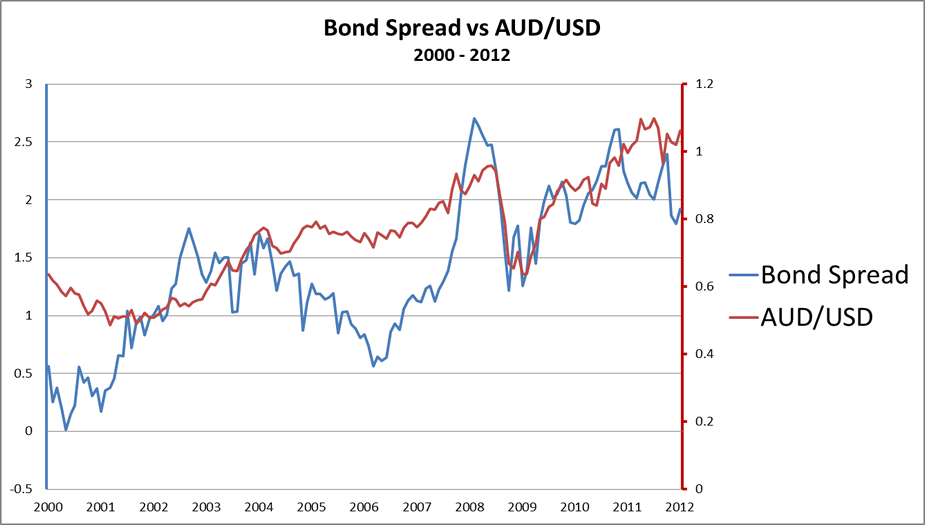

How Bond Spreads Between Two Countries Affect Their Exchange Rate

Spread Duration Of A Bond It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. The yield spread is a key metric that bond investors use when gauging the level of expense for a bond or group of bonds. Duration can also be used to measure how sensitive the. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is the sensitivity of a security’s price to changes in its credit spread. Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. If one bond yields 7% and another one yields 4%, the. Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity to. Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread.

From www.livemint.com

Credit spreads on AAA corporate bonds at historic low Mint Spread Duration Of A Bond Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. If one bond yields 7% and another one yields 4%, the. Duration can also be used to measure how sensitive the. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks. Spread Duration Of A Bond.

From ar.inspiredpencil.com

Yield To Maturity Spread Duration Of A Bond Duration can also be used to measure how sensitive the. Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Spread duration is the sensitivity of a security’s price to changes in its credit spread. The yield spread is a key metric that bond investors use when gauging the level. Spread Duration Of A Bond.

From www.youtube.com

CFA Level 1 Fixed Reading 55 Understanding Fixed Risk Spread Duration Of A Bond Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Spread duration is a measure of the percentage change in a bond’s price for a given change in. Spread Duration Of A Bond.

From www.chegg.com

6. State why you would agree or disagree with the Spread Duration Of A Bond The yield spread is a key metric that bond investors use when gauging the level of expense for a bond or group of bonds. If one bond yields 7% and another one yields 4%, the. Spread duration is the sensitivity of a security’s price to changes in its credit spread. Duration can also be used to measure how sensitive the.. Spread Duration Of A Bond.

From www.financestrategists.com

FloatingRate Bonds Definition, Types, Benefits, and Risks Spread Duration Of A Bond Spread duration is the sensitivity of a security’s price to changes in its credit spread. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. It quantifies. Spread Duration Of A Bond.

From bondevalue.com

Bond Duration Understanding Interest Rate Risk Spread Duration Of A Bond Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity to. If one bond yields 7% and another one yields 4%, the. Duration can also be used to measure how sensitive the. Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features.. Spread Duration Of A Bond.

From seekingalpha.com

Bond Portfolio Duration And The Flaw Of Averages Seeking Alpha Spread Duration Of A Bond Duration can also be used to measure how sensitive the. Spread duration is the sensitivity of a security’s price to changes in its credit spread. Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Duration measures how long it takes, in years, for an investor to be repaid a. Spread Duration Of A Bond.

From www.axa-im.com.sg

Spread the word Managing drawdown risks in corporate bond portfolios Spread Duration Of A Bond Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. Spread duration is the sensitivity of a security’s price to changes in its credit spread. The yield spread is a key metric that bond investors use when gauging the level of expense for a bond or group of bonds.. Spread Duration Of A Bond.

From www.babypips.com

How Bond Spreads Between Two Countries Affect Their Exchange Rate Spread Duration Of A Bond It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. The yield spread is a key metric that bond investors use when gauging the level of expense for a bond or group of bonds. Duration can also be used to measure how sensitive the.. Spread Duration Of A Bond.

From moneymusingz.in

Duration of a Bond Money Musingz Personal Finance Blog Spread Duration Of A Bond If one bond yields 7% and another one yields 4%, the. Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. The yield spread is a key metric that bond investors use when gauging the level of expense for a bond or group of bonds. It quantifies the. Spread Duration Of A Bond.

From efinancemanagement.com

Duration of a Bond Portfolio Duration Macaulay & Modified Duration Spread Duration Of A Bond Spread duration is the sensitivity of a security’s price to changes in its credit spread. The yield spread is a key metric that bond investors use when gauging the level of expense for a bond or group of bonds. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards. Spread Duration Of A Bond.

From www.slideserve.com

PPT Bond Duration PowerPoint Presentation, free download ID5585530 Spread Duration Of A Bond Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. Spread duration is the sensitivity of a security’s price to changes in its credit spread. The yield spread is a key metric that bond investors use when gauging the level of expense for a bond or group of bonds.. Spread Duration Of A Bond.

From www.morningstar.co.uk

The US Treasury Yield Curve Recession Indicator is... Morningstar Spread Duration Of A Bond Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is a measure of the percentage change in a bond’s price for. Spread Duration Of A Bond.

From www.slideserve.com

PPT Bond Price Volatility PowerPoint Presentation, free download ID Spread Duration Of A Bond The yield spread is a key metric that bond investors use when gauging the level of expense for a bond or group of bonds. Spread duration is the sensitivity of a security’s price to changes in its credit spread. Duration can also be used to measure how sensitive the. Duration is a measurement of a bond’s interest rate risk that. Spread Duration Of A Bond.

From pinterest.com

Callable bonds. In a callable security, a call option could mean Spread Duration Of A Bond Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity to. Duration can also be used to measure how sensitive the. Spread duration is the sensitivity of a security’s price to changes in its credit spread. If one bond yields 7% and another one yields 4%, the. It quantifies the sensitivity of. Spread Duration Of A Bond.

From www.britannica.com

Bond Duration Definition, Formula, & How to Calculate Britannica Money Spread Duration Of A Bond Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. If one bond yields 7% and another one yields 4%, the. Spread duration focuses on a bond's. Spread Duration Of A Bond.

From twitter.com

Martin Pelletier on Twitter "Equity duration vs Bond duration. Look at Spread Duration Of A Bond Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity to. The yield spread is a key metric that bond investors use when gauging the level of expense for a bond or group of bonds. Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon. Spread Duration Of A Bond.

From www.ecb.europa.eu

Exploring the factors behind the 2018 widening in euro area corporate Spread Duration Of A Bond It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. The yield spread is a key metric that bond investors use when gauging. Spread Duration Of A Bond.

From www.financehomie.com

Spread Duration Explained Spread Duration Of A Bond Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is the sensitivity of a security’s price to changes in. Spread Duration Of A Bond.

From www.slideserve.com

PPT Bond Price Volatility PowerPoint Presentation, free download ID Spread Duration Of A Bond If one bond yields 7% and another one yields 4%, the. Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Spread duration is the sensitivity of a security’s price to changes in its credit spread. Duration can also be used to measure how sensitive the. The yield. Spread Duration Of A Bond.

From www.columbiathreadneedleus.com

Chart Two types of steepening yield curves Columbia Threadneedle Blog Spread Duration Of A Bond Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Duration is a measurement of a bond’s interest rate risk that considers a. Spread Duration Of A Bond.

From www.investopedia.com

Duration and Convexity to Measure Bond Risk Spread Duration Of A Bond Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. If one bond yields 7% and another one yields 4%, the. Spread duration focuses on a bond's price. Spread Duration Of A Bond.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation ID3950949 Spread Duration Of A Bond Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Spread duration is the sensitivity of a security’s price to changes in its credit spread. Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity to. The yield spread is. Spread Duration Of A Bond.

From www.investopedia.com

Understanding Treasury Yield and Interest Rates Spread Duration Of A Bond Duration can also be used to measure how sensitive the. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity to. Duration measures how long it takes, in years, for an. Spread Duration Of A Bond.

From www.youtube.com

Understanding credit spread duration and its impact on bond prices Spread Duration Of A Bond If one bond yields 7% and another one yields 4%, the. Duration can also be used to measure how sensitive the. Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity to. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit. Spread Duration Of A Bond.

From www.carboncollective.co

Bond Duration What It Is & How It Works, Why it Matters Spread Duration Of A Bond Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. If one bond yields 7% and another one yields 4%, the. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. The yield spread is a key metric that. Spread Duration Of A Bond.

From www.educba.com

Macaulay Duration Formula Example with Excel Template Spread Duration Of A Bond Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Duration can also be used to measure how sensitive the. Spread duration is a measure of the percentage. Spread Duration Of A Bond.

From telegra.ph

Spread Bond Telegraph Spread Duration Of A Bond If one bond yields 7% and another one yields 4%, the. Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Duration. Spread Duration Of A Bond.

From www.slideserve.com

PPT Bond Price Volatility PowerPoint Presentation, free download ID Spread Duration Of A Bond Duration can also be used to measure how sensitive the. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity to. Duration is a measurement of. Spread Duration Of A Bond.

From analystprep.com

Valuing Embedded Options CFA, FRM, and Actuarial Exams Study Notes Spread Duration Of A Bond Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity. Spread Duration Of A Bond.

From analystprep.com

Optionadjusted Spreads CFA, FRM, and Actuarial Exams Study Notes Spread Duration Of A Bond Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is a measure of the percentage change in a bond’s price for. Spread Duration Of A Bond.

From www.investopedia.com

The Predictive Powers of the Bond Yield Curve Spread Duration Of A Bond Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Spread duration is a measure of the percentage change in a bond’s price for a given change in. Spread Duration Of A Bond.

From www.investopedia.com

Understanding Treasury Yields and Interest Rates Spread Duration Of A Bond Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its total cash flows. Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the. Spread Duration Of A Bond.

From www.ejshin.org

Education Ultimate Fixed 101 What are Credit Spread, Spread Spread Duration Of A Bond Spread duration is a measure of the percentage change in a bond’s price for a given change in its credit spread. Duration is a measurement of a bond’s interest rate risk that considers a bond’s maturity, yield, coupon and call features. Duration measures how long it takes, in years, for an investor to be repaid a bond’s price through its. Spread Duration Of A Bond.

From econbrowser.com

Yield curve inversion Econbrowser Spread Duration Of A Bond It quantifies the sensitivity of a bond’s price to credit spread movements, allowing investors to evaluate the potential risks and rewards associated with credit spread changes. Spread duration is the sensitivity of a security’s price to changes in its credit spread. Spread duration is a measure of the percentage change in a bond’s price for a given change in its. Spread Duration Of A Bond.