Direct Materials Spending Variance . there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. direct materials spending variance. the direct material variance is the difference between the standard cost of materials resulting from production. Variance from budgeted costs may arise. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. direct materials refer to basic materials that form an integral part of a finished product. The spending variance for direct materials is known as the purchase price.

from psu.pb.unizin.org

direct materials spending variance. Variance from budgeted costs may arise. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. the direct material variance is the difference between the standard cost of materials resulting from production. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. direct materials refer to basic materials that form an integral part of a finished product. there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. The spending variance for direct materials is known as the purchase price.

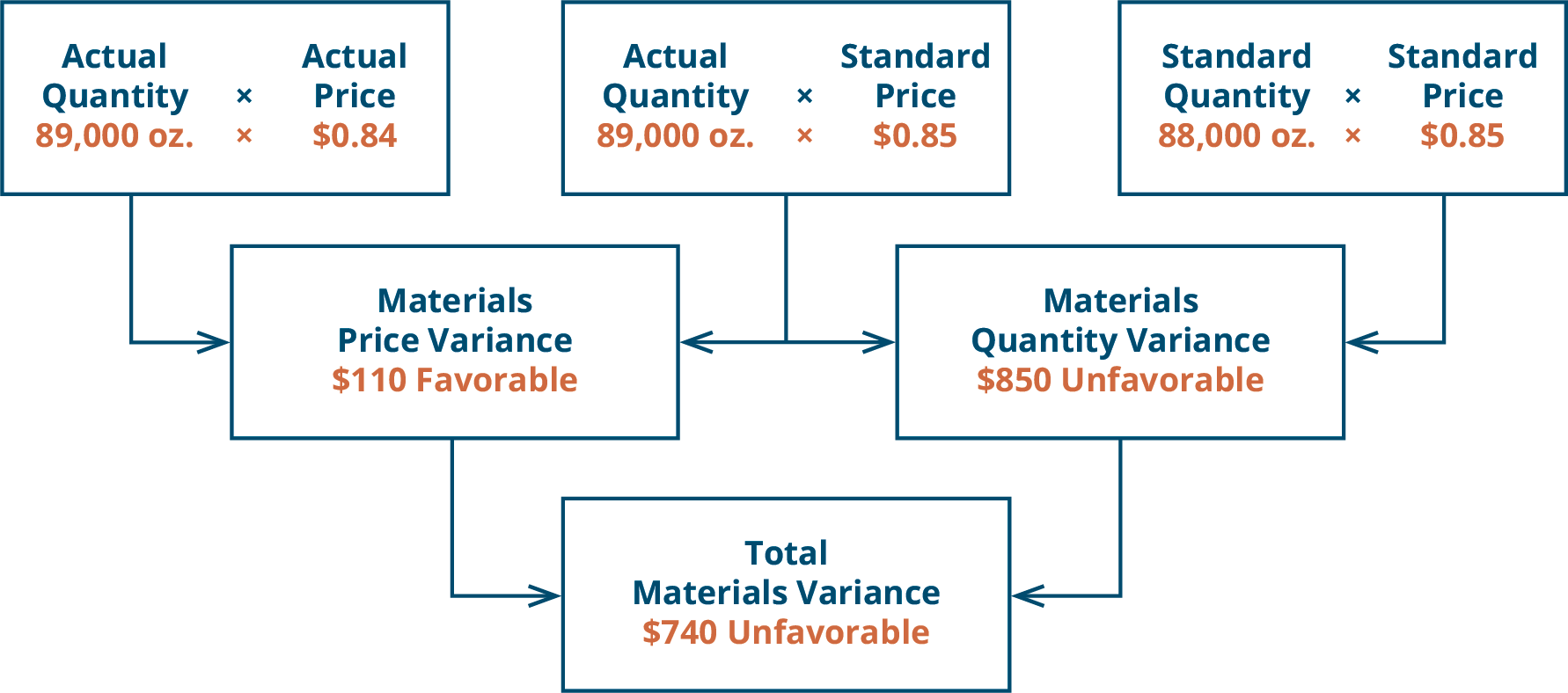

10.6 Direct Materials Variances Financial and Managerial Accounting

Direct Materials Spending Variance the direct material variance is the difference between the standard cost of materials resulting from production. there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. direct materials refer to basic materials that form an integral part of a finished product. the direct material variance is the difference between the standard cost of materials resulting from production. direct materials spending variance. Variance from budgeted costs may arise. The spending variance for direct materials is known as the purchase price. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have.

From accountingo.org

Direct Material Price Variance Accountingo Direct Materials Spending Variance the direct material variance is the difference between the standard cost of materials resulting from production. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. direct. Direct Materials Spending Variance.

From www.chegg.com

Solved c. Compute the direct materials spending Direct Materials Spending Variance the direct material variance is the difference between the standard cost of materials resulting from production. direct materials refer to basic materials that form an integral part of a finished product. Variance from budgeted costs may arise. The spending variance for direct materials is known as the purchase price. learn how to calculate, analyze, and apply direct. Direct Materials Spending Variance.

From www.slideserve.com

PPT Chapter 7 Flexible Budgets, Variances, and Management Control I PowerPoint Presentation Direct Materials Spending Variance Variance from budgeted costs may arise. the direct material variance is the difference between the standard cost of materials resulting from production. there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. The spending variance for direct materials is known as the purchase price. direct materials refer to. Direct Materials Spending Variance.

From efinancemanagement.com

Price Variance Meaning, Calculation, Importance and More Direct Materials Spending Variance the direct material variance is the difference between the standard cost of materials resulting from production. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. direct materials refer to basic materials that form an integral part of a finished product. The spending variance for direct materials is known as the. Direct Materials Spending Variance.

From www.chegg.com

Solved Direct Materials Usage Variance, Direct Materials Mix Direct Materials Spending Variance Variance from budgeted costs may arise. there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. the direct material variance is the difference between the standard cost of materials resulting from production. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved.. Direct Materials Spending Variance.

From www.chegg.com

Solved Exercise 219 (Algo) Direct materials variances LO P3 Direct Materials Spending Variance The spending variance for direct materials is known as the purchase price. direct materials refer to basic materials that form an integral part of a finished product. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. there are two components to a direct materials variance, the. Direct Materials Spending Variance.

From www.slideserve.com

PPT Chapter 7 Flexible Budgets, Variances, and Management Control I PowerPoint Presentation Direct Materials Spending Variance direct materials refer to basic materials that form an integral part of a finished product. the direct material variance is the difference between the standard cost of materials resulting from production. Variance from budgeted costs may arise. The spending variance for direct materials is known as the purchase price. to compute the direct materials quantity variance, subtract. Direct Materials Spending Variance.

From efinancemanagement.com

Direct Materials Quantity Variance All You Need to Know Direct Materials Spending Variance the direct material variance is the difference between the standard cost of materials resulting from production. The spending variance for direct materials is known as the purchase price. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. direct materials spending variance. learn how to calculate, analyze, and apply. Direct Materials Spending Variance.

From www.slideserve.com

PPT Performance Evaluation Using Variances from Standard Costs PowerPoint Presentation ID Direct Materials Spending Variance direct materials spending variance. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. The spending variance for direct materials is known as the purchase price. the direct material variance is the difference between the standard cost of materials resulting from production. learn how to calculate, analyze, and apply. Direct Materials Spending Variance.

From www.coursehero.com

[Solved] E97 (Algo) Calculating Direct Material and Direct Labor Variances... Course Hero Direct Materials Spending Variance Variance from budgeted costs may arise. the direct material variance is the difference between the standard cost of materials resulting from production. direct materials refer to basic materials that form an integral part of a finished product. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. learn how. Direct Materials Spending Variance.

From www.slideserve.com

PPT Direct Input Variances, and Management Control I PowerPoint Presentation ID566171 Direct Materials Spending Variance The spending variance for direct materials is known as the purchase price. the direct material variance is the difference between the standard cost of materials resulting from production. Variance from budgeted costs may arise. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. direct materials spending variance. to compute. Direct Materials Spending Variance.

From accountingo.org

Direct Material Price Variance Accountingo Direct Materials Spending Variance the direct material variance is the difference between the standard cost of materials resulting from production. Variance from budgeted costs may arise. direct materials refer to basic materials that form an integral part of a finished product. there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. . Direct Materials Spending Variance.

From www.slideserve.com

PPT Chapter 11 Standard Costs & Variance Analysis PowerPoint Presentation ID863490 Direct Materials Spending Variance to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. The spending variance for direct materials is known as the purchase price. Variance from budgeted costs may arise. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. direct materials spending variance. the. Direct Materials Spending Variance.

From www.chegg.com

Solved Calculate the Direct Materials Spending Variance Direct Materials Spending Variance variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. The spending variance for direct materials is known as the purchase price. the direct material variance is the difference between the standard cost of materials resulting from production. there are two components to a direct materials variance,. Direct Materials Spending Variance.

From www.coursehero.com

3. Compute the direct materials cost variance, including its price... Course Hero Direct Materials Spending Variance The spending variance for direct materials is known as the purchase price. direct materials spending variance. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. direct materials refer to basic materials that form an integral part of a finished product. Variance from budgeted costs may arise.. Direct Materials Spending Variance.

From exowjdtwi.blob.core.windows.net

Direct Materials How To Calculate at William Brinn blog Direct Materials Spending Variance direct materials refer to basic materials that form an integral part of a finished product. direct materials spending variance. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. Variance from budgeted costs may arise. to compute the direct materials quantity variance, subtract the actual quantity. Direct Materials Spending Variance.

From www.slideteam.net

Direct Materials Spending Variance Ppt Powerpoint Presentation Template Cpb PowerPoint Direct Materials Spending Variance direct materials spending variance. there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price.. Direct Materials Spending Variance.

From www.principlesofaccounting.com

Variance Analysis Direct Materials Spending Variance to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. Variance from budgeted costs may arise. direct materials spending variance. the direct material variance is the difference between the standard cost of materials resulting from production. variable overhead spending variance is the difference between what the variable production overheads. Direct Materials Spending Variance.

From dxospbybf.blob.core.windows.net

Direct Materials Examples In Accounting at Bolton blog Direct Materials Spending Variance the direct material variance is the difference between the standard cost of materials resulting from production. direct materials refer to basic materials that form an integral part of a finished product. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. variable overhead spending variance is the difference between. Direct Materials Spending Variance.

From psu.pb.unizin.org

10.9 Management’s Use of Variance Analysis Financial and Managerial Accounting Direct Materials Spending Variance The spending variance for direct materials is known as the purchase price. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. direct materials refer to basic materials that form an integral part of a finished product. variable overhead spending variance is the difference between what the variable production overheads. Direct Materials Spending Variance.

From www.chegg.com

Solved Standard Product Cost, Direct Materials Variance Direct Materials Spending Variance the direct material variance is the difference between the standard cost of materials resulting from production. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. to. Direct Materials Spending Variance.

From www.coursehero.com

Direct Materials Variance Analysis Accounting for Managers Course Hero Direct Materials Spending Variance Variance from budgeted costs may arise. The spending variance for direct materials is known as the purchase price. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. the direct material variance is the difference between the standard cost of materials resulting from production. direct materials spending. Direct Materials Spending Variance.

From www.slideserve.com

PPT Chapter 11 Standard Costs & Variance Analysis PowerPoint Presentation ID863490 Direct Materials Spending Variance there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. the direct material variance is the difference between the standard cost of materials resulting from production. direct materials spending variance. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. . Direct Materials Spending Variance.

From www.chegg.com

Solved Knowledge Check 04 Calculate the direct materials Direct Materials Spending Variance learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. direct materials spending variance. direct materials refer to basic materials that form an integral part of a finished product. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. Variance. Direct Materials Spending Variance.

From www.scribd.com

Understanding Direct Material Costs A Detailed Explanation of Material Variances, Break Even Direct Materials Spending Variance The spending variance for direct materials is known as the purchase price. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. the direct material variance is the difference between the standard cost of materials resulting from production. direct materials spending variance. there are two components to a direct. Direct Materials Spending Variance.

From psu.pb.unizin.org

10.6 Direct Materials Variances Financial and Managerial Accounting Direct Materials Spending Variance to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. the direct material. Direct Materials Spending Variance.

From www.slideshare.net

Projecto variance Direct Materials Spending Variance Variance from budgeted costs may arise. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should have. there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. learn how to calculate, analyze, and apply direct material variance for effective. Direct Materials Spending Variance.

From www.chegg.com

Solved Exercise 815 (Algo) Direct materials and direct Direct Materials Spending Variance direct materials spending variance. direct materials refer to basic materials that form an integral part of a finished product. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. the direct material variance is the difference between the standard cost of materials resulting from production. Variance from budgeted costs. Direct Materials Spending Variance.

From www.superfastcpa.com

What is a Direct Material Variance? Direct Materials Spending Variance there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. the direct material variance is the difference between the standard cost of materials resulting from production. direct materials spending variance. The. Direct Materials Spending Variance.

From kaitlynn-has-valencia.blogspot.com

The Two Variances in Direct Materials Cost Are KaitlynnhasValencia Direct Materials Spending Variance direct materials spending variance. learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. The spending variance for direct materials is known as the purchase price. Variance from budgeted costs may arise. the direct material variance is the difference between the standard cost of materials resulting from production. to compute. Direct Materials Spending Variance.

From www.scribd.com

Analysis of Standard Costs, Variances, and Flexible Budgeting for Direct Materials, Direct Labor Direct Materials Spending Variance learn how to calculate, analyze, and apply direct material variance for effective cost control and improved. direct materials refer to basic materials that form an integral part of a finished product. direct materials spending variance. there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. to. Direct Materials Spending Variance.

From www.slideserve.com

PPT Standard Costing and Variance Analysis PowerPoint Presentation ID6406125 Direct Materials Spending Variance Variance from budgeted costs may arise. direct materials refer to basic materials that form an integral part of a finished product. there are two components to a direct materials variance, the direct materials price variance and the direct materials quantity. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price.. Direct Materials Spending Variance.

From www.thetechedvocate.org

How to calculate material price variance The Tech Edvocate Direct Materials Spending Variance Variance from budgeted costs may arise. the direct material variance is the difference between the standard cost of materials resulting from production. direct materials spending variance. direct materials refer to basic materials that form an integral part of a finished product. variable overhead spending variance is the difference between what the variable production overheads actually cost. Direct Materials Spending Variance.

From courses.lumenlearning.com

Direct Materials Variance Analysis Accounting for Managers Direct Materials Spending Variance direct materials refer to basic materials that form an integral part of a finished product. to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. Variance from budgeted costs may arise. The spending variance for direct materials is known as the purchase price. direct materials spending variance. learn how. Direct Materials Spending Variance.

From efinancemanagement.com

Material Variance Cost, Price, Usage Formula & Example eFM Direct Materials Spending Variance to compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price. the direct material variance is the difference between the standard cost of materials resulting from production. direct materials spending variance. variable overhead spending variance is the difference between what the variable production overheads actually cost and what they should. Direct Materials Spending Variance.