Cost Run Equilibrium . By the end of this section, you will be able to: A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. The effect of an increase in demand for the industry. See how different price levels and outputs. Explain demand, quantity demanded, and the law of. If there is an increase in demand there will be an. changes in long run equilibrium. 6.7 why perfect competition is desirable. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply.

from www.chegg.com

In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. See how different price levels and outputs. If there is an increase in demand there will be an. A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. 6.7 why perfect competition is desirable. The effect of an increase in demand for the industry. By the end of this section, you will be able to: changes in long run equilibrium. Explain demand, quantity demanded, and the law of.

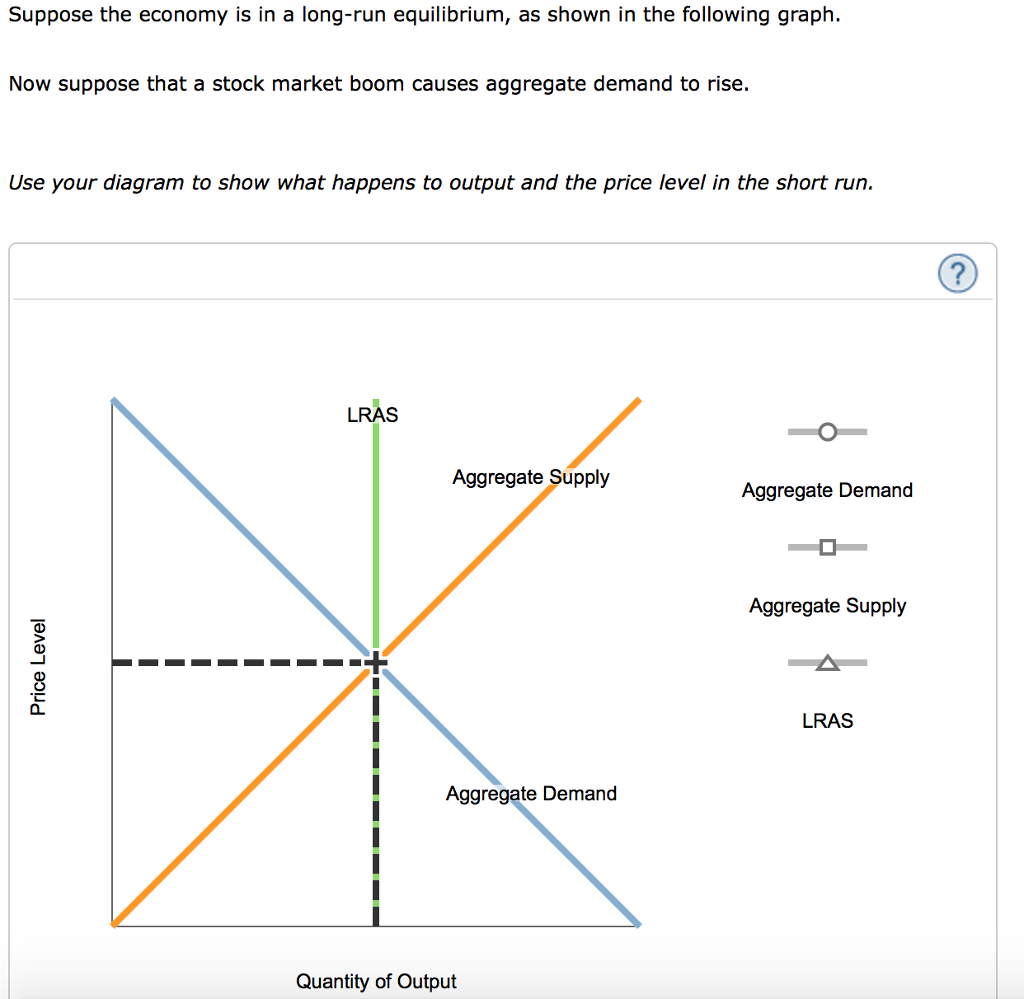

Solved Suppose the economy is in a longrun equilibrium, as

Cost Run Equilibrium In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. The effect of an increase in demand for the industry. By the end of this section, you will be able to: A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. changes in long run equilibrium. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. See how different price levels and outputs. Explain demand, quantity demanded, and the law of. If there is an increase in demand there will be an. 6.7 why perfect competition is desirable. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal.

From www.tutor2u.net

Monopolistic Competition tutor2u Economics Cost Run Equilibrium If there is an increase in demand there will be an. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. See how different price levels and outputs. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. A perfectly competitive firm is a price. Cost Run Equilibrium.

From analystprep.com

Longrun Equilibrium Under Each Market Structure AnalystPrep CFA Cost Run Equilibrium Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. Explain demand, quantity demanded, and the law of. See how different price levels and outputs. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. If there is an increase in demand there will be. Cost Run Equilibrium.

From www.chegg.com

Solved 7. Shortrun supply and longrun equilibrium Consider Cost Run Equilibrium A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. The effect of an increase in demand for the industry. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. See how different price levels and outputs. 6.7 why perfect competition. Cost Run Equilibrium.

From snipe.fm

😍 Long run equilibrium in a perfectly competitive market. The Long Cost Run Equilibrium See how different price levels and outputs. changes in long run equilibrium. A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. Explain demand, quantity demanded, and the law of. By the end of this section, you will be able to: In a simple market under perfect competition,. Cost Run Equilibrium.

From penpoin.com

LongRun Macroeconomic Equilibrium and Its Explanation Cost Run Equilibrium The effect of an increase in demand for the industry. 6.7 why perfect competition is desirable. Explain demand, quantity demanded, and the law of. By the end of this section, you will be able to: If there is an increase in demand there will be an. In a simple market under perfect competition, equilibrium occurs at a quantity and. Cost Run Equilibrium.

From www.chegg.com

Solved The graphs below illustrate an initial equilibrium Cost Run Equilibrium By the end of this section, you will be able to: See how different price levels and outputs. The effect of an increase in demand for the industry. Explain demand, quantity demanded, and the law of. If there is an increase in demand there will be an. A perfectly competitive firm is a price taker, which means that it must. Cost Run Equilibrium.

From www.chegg.com

Solved 7. Shortrun supply and longrun equilibrium Consider Cost Run Equilibrium changes in long run equilibrium. See how different price levels and outputs. Explain demand, quantity demanded, and the law of. If there is an increase in demand there will be an. By the end of this section, you will be able to: In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal.. Cost Run Equilibrium.

From intelligenteconomist.com

Monopolistic Competition Market Structure Intelligent Economist Cost Run Equilibrium changes in long run equilibrium. By the end of this section, you will be able to: See how different price levels and outputs. A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. Explain demand, quantity demanded, and the law of. In a simple market under perfect competition,. Cost Run Equilibrium.

From www.coursehero.com

[Solved] solve the problem Product A is sold in a perfectly competitive Cost Run Equilibrium Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. See how different price levels and outputs. 6.7 why perfect competition is desirable. If there is an increase in demand there will be an. Explain demand, quantity demanded, and the law of. By the end of this section, you will be. Cost Run Equilibrium.

From passnownow.com

SS1 Economics Third Term Equilibrium Price/Price Determination Cost Run Equilibrium See how different price levels and outputs. If there is an increase in demand there will be an. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. 6.7 why perfect competition is desirable. A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price. Cost Run Equilibrium.

From www.mrbanks.co.uk

Perfect Competition — Mr Banks Tuition Tuition Services. Free Cost Run Equilibrium Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. 6.7 why perfect competition is desirable. If there is an increase in demand there will be an. See how different price levels and outputs. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal.. Cost Run Equilibrium.

From www.intelligenteconomist.com

Perfect Competition Intelligent Economist Cost Run Equilibrium See how different price levels and outputs. If there is an increase in demand there will be an. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. By the end of this section, you will be able to: Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate. Cost Run Equilibrium.

From api-stg.3m.com

😱 Long run equilibrium in a perfectly competitive market. Long. 20221102 Cost Run Equilibrium changes in long run equilibrium. Explain demand, quantity demanded, and the law of. 6.7 why perfect competition is desirable. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. The effect of an increase in demand for the industry. A perfectly competitive firm is a price taker, which means that it. Cost Run Equilibrium.

From www.chegg.com

Solved Suppose the economy is in a longrun equilibrium, as Cost Run Equilibrium The effect of an increase in demand for the industry. 6.7 why perfect competition is desirable. A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. By the end of this section, you will be able to: Explain demand, quantity demanded, and the law of. See how different. Cost Run Equilibrium.

From www.answersarena.com

[Solved] 7. Shortrun supply and longrun equilibrium Cons Cost Run Equilibrium In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. 6.7 why perfect competition is desirable. See how different price levels and outputs. changes in long run equilibrium. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. If there is an increase. Cost Run Equilibrium.

From www.chegg.com

Solved 7. Shortrun supply and longrun equilibrium Consider Cost Run Equilibrium A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. By the end of this section, you will be able to: changes in long run equilibrium. If there is an increase. Cost Run Equilibrium.

From www.chegg.com

Solved Figure ShortRun Equilibrium Aggregate price level Cost Run Equilibrium If there is an increase in demand there will be an. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. 6.7 why perfect competition is desirable. Explain demand, quantity. Cost Run Equilibrium.

From 2012books.lardbucket.org

Recessionary and Inflationary Gaps and LongRun Macroeconomic Equilibrium Cost Run Equilibrium If there is an increase in demand there will be an. By the end of this section, you will be able to: In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. 6.7 why. Cost Run Equilibrium.

From webapi.bu.edu

🎉 Short run macroeconomic equilibrium. Macroeconomic Equilibrium Cost Run Equilibrium 6.7 why perfect competition is desirable. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. Explain demand, quantity demanded, and the law of. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. By the end of this section, you will be able. Cost Run Equilibrium.

From www.chegg.com

Solved Price level The following graph shows aggregate Cost Run Equilibrium 6.7 why perfect competition is desirable. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. Explain demand, quantity demanded, and the law of. The effect of an increase in demand for the industry. changes in long run equilibrium. A perfectly competitive firm is a price taker, which means that it. Cost Run Equilibrium.

From www.chegg.com

Solved 7. Shortrun supply and longrun equilibrium Consider Cost Run Equilibrium See how different price levels and outputs. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. If there is an increase in demand there will be an. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. changes in long run equilibrium. . Cost Run Equilibrium.

From www.youtube.com

Finding Longrun Equilibrium from Cost FunctionsII YouTube Cost Run Equilibrium Explain demand, quantity demanded, and the law of. The effect of an increase in demand for the industry. If there is an increase in demand there will be an. By the end of this section, you will be able to: See how different price levels and outputs. 6.7 why perfect competition is desirable. In a simple market under perfect. Cost Run Equilibrium.

From www.intelligenteconomist.com

Perfect Competition Short Run Intelligent Economist Cost Run Equilibrium changes in long run equilibrium. The effect of an increase in demand for the industry. See how different price levels and outputs. A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the. Cost Run Equilibrium.

From www.coursehero.com

[Solved] Short run supply and longrun equilibrium Consider the Cost Run Equilibrium In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. By the end of this section, you will be able to: See how different price levels and outputs. The effect of an. Cost Run Equilibrium.

From mysominotes.wordpress.com

ECONOMICS OF EDUCATION How does cost function analysis and internal Cost Run Equilibrium changes in long run equilibrium. A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. By the end of this section, you will be able to: Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. 6.7 why perfect. Cost Run Equilibrium.

From keplarllp.com

😀 Explain equilibrium price. Supply and Demand The Market Mechanism Cost Run Equilibrium Explain demand, quantity demanded, and the law of. The effect of an increase in demand for the industry. If there is an increase in demand there will be an. changes in long run equilibrium. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. By the end of this section, you will. Cost Run Equilibrium.

From www.chegg.com

Solved 6. Shortrun perfectly competitive equilibrium Cost Run Equilibrium If there is an increase in demand there will be an. Explain demand, quantity demanded, and the law of. The effect of an increase in demand for the industry. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. 6.7 why perfect competition is desirable. In a simple market under perfect. Cost Run Equilibrium.

From analystprep.com

ShortRun Macroeconomic Equilibrium CFA Level 1 AnalystPrep Cost Run Equilibrium If there is an increase in demand there will be an. changes in long run equilibrium. Explain demand, quantity demanded, and the law of. By the end of this section, you will be able to: In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. 6.7 why perfect competition is desirable.. Cost Run Equilibrium.

From www.intelligenteconomist.com

Perfect Competition Intelligent Economist Cost Run Equilibrium Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. changes in long run equilibrium. Explain demand, quantity demanded, and the law of. 6.7 why perfect competition is desirable. By the end of this section, you will be able to: If there is an increase in demand there will be. Cost Run Equilibrium.

From saylordotorg.github.io

Perfect Competition and Supply and Demand Cost Run Equilibrium Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. 6.7 why perfect competition is desirable. By the end of this section, you will be able to: See how different price levels and outputs. Explain demand, quantity demanded, and the law of. A perfectly competitive firm is a price taker, which. Cost Run Equilibrium.

From www.chegg.com

Solved 7. Shortrun supply and longrun equilibrium Cost Run Equilibrium See how different price levels and outputs. The effect of an increase in demand for the industry. Explain demand, quantity demanded, and the law of. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at. Cost Run Equilibrium.

From analystprep.com

Factors Affecting LongRun Equilibrium Example CFA Level 1 AnalystPrep Cost Run Equilibrium changes in long run equilibrium. By the end of this section, you will be able to: See how different price levels and outputs. The effect of an increase in demand for the industry. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. Let's look at the concept of equilibrium in macroeconomics,. Cost Run Equilibrium.

From www.chegg.com

Solved Because this market is a monopolistically competitive Cost Run Equilibrium A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. Explain demand, quantity demanded, and the law of. By the end of this section, you will be able to: Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. 6.7. Cost Run Equilibrium.

From www.slideserve.com

PPT 1. In a perfectly competitive market in longrun equilibrium Cost Run Equilibrium A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells. Let's look at the concept of equilibrium in macroeconomics, using graphs to illustrate aggregate demand and aggregate supply. See how different price levels and outputs. If there is an increase in demand there will be an. Explain demand, quantity. Cost Run Equilibrium.

From economicsnotes11.blogspot.com

Equilibrium in the Long Run Economics Cost Run Equilibrium If there is an increase in demand there will be an. In a simple market under perfect competition, equilibrium occurs at a quantity and price where the marginal. By the end of this section, you will be able to: Explain demand, quantity demanded, and the law of. 6.7 why perfect competition is desirable. The effect of an increase in. Cost Run Equilibrium.