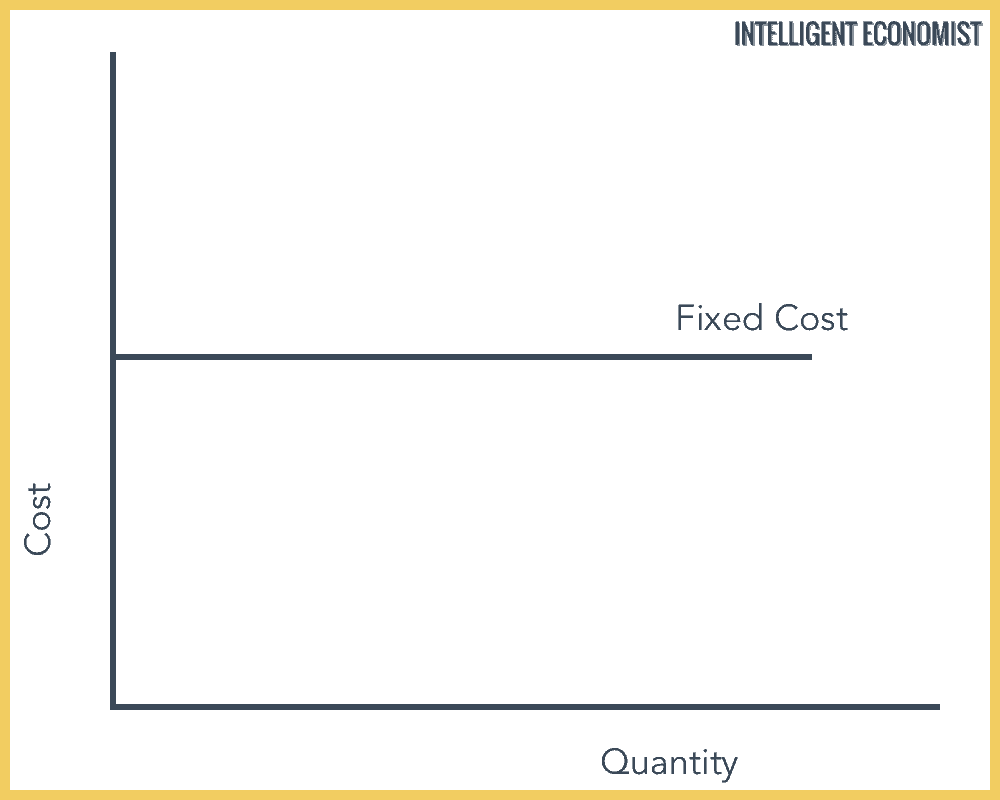

Fixed Cost Is The Cost . A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and depreciation. Some examples of fixed costs may include insurance, rent,. Graphs of mc, avc and atc. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Marginal cost, average variable cost, and average total cost. They remain constant, within capacity limits of a. A fixed cost is a business expense that does not vary even if the level of production or sales changes. They can be be used when calculating key business. Marginal revenue and marginal cost.

from www.intelligenteconomist.com

Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Marginal cost, average variable cost, and average total cost. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Some examples of fixed costs may include insurance, rent,. They remain constant, within capacity limits of a. A fixed cost is a business expense that does not vary even if the level of production or sales changes. They can be be used when calculating key business. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and depreciation. Graphs of mc, avc and atc. Marginal revenue and marginal cost.

Theory Of Production Cost Theory Intelligent Economist

Fixed Cost Is The Cost Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and depreciation. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and depreciation. Marginal revenue and marginal cost. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Some examples of fixed costs may include insurance, rent,. A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. Graphs of mc, avc and atc. Marginal cost, average variable cost, and average total cost. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. They can be be used when calculating key business. They remain constant, within capacity limits of a. A fixed cost is a business expense that does not vary even if the level of production or sales changes.

From www.educba.com

Fixed Cost Vs Variable Cost Top 12 Key Differences & Examples Fixed Cost Is The Cost They can be be used when calculating key business. Marginal cost, average variable cost, and average total cost. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Some examples of fixed costs may include insurance, rent,. Marginal revenue and marginal cost. A fixed cost is a business expense that remains. Fixed Cost Is The Cost.

From boycewire.com

Fixed Costs Definition Fixed Cost Is The Cost Marginal cost, average variable cost, and average total cost. Marginal revenue and marginal cost. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Graphs of. Fixed Cost Is The Cost.

From www.marketing91.com

Average Fixed Cost Definition, Formula and Examples Marketing91 Fixed Cost Is The Cost They remain constant, within capacity limits of a. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. A fixed cost is a business expense that does not vary even if the level of production or sales changes. Fixed costs are expenses that remain the. Fixed Cost Is The Cost.

From www.founderjar.com

Variable Cost vs. Fixed Cost What's the One Key Difference? FounderJar Fixed Cost Is The Cost A fixed cost is a business expense that does not vary even if the level of production or sales changes. They remain constant, within capacity limits of a. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. A fixed cost is a business expense that remains unchanged, no matter how. Fixed Cost Is The Cost.

From www.intelligenteconomist.com

Theory Of Production Cost Theory Intelligent Economist Fixed Cost Is The Cost A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. Graphs of mc, avc and atc. They can be be used when calculating key business. They remain constant, within capacity limits of a. Fixed costs are expenses that remain the same no matter how much a company produces, such. Fixed Cost Is The Cost.

From www.educba.com

What is Fixed Cost? Formula & Examples Advantages & Disadvantages Fixed Cost Is The Cost Some examples of fixed costs may include insurance, rent,. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and depreciation. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Graphs of mc, avc and atc. Fixed costs are. Fixed Cost Is The Cost.

From seoimnews.com

Fixed Cost What It Is & How to Calculate It Seoim News Fixed Cost Is The Cost Some examples of fixed costs may include insurance, rent,. Marginal cost, average variable cost, and average total cost. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and depreciation.. Fixed Cost Is The Cost.

From efinancemanagement.com

Fixed Cost What It Is And What's Its Importance? Fixed Cost Is The Cost Some examples of fixed costs may include insurance, rent,. Marginal cost, average variable cost, and average total cost. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Graphs of mc, avc and atc. Fixed costs are expenses that do not change with increases or. Fixed Cost Is The Cost.

From www.educba.com

Top 3 Fixed Cost Examples with Explanation [Solution] Fixed Cost Is The Cost Marginal cost, average variable cost, and average total cost. A fixed cost is a business expense that does not vary even if the level of production or sales changes. Some examples of fixed costs may include insurance, rent,. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. They remain constant,. Fixed Cost Is The Cost.

From www.1099cafe.com

What is a Fixed Cost Variable vs Fixed Expenses — 1099 Cafe Fixed Cost Is The Cost Some examples of fixed costs may include insurance, rent,. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Graphs of mc, avc and atc. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. A. Fixed Cost Is The Cost.

From www.investopedia.com

Fixed Cost What It Is and How It’s Used in Business Fixed Cost Is The Cost A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. Marginal revenue and marginal cost. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Fixed costs are expenses that remain the same no matter how much a company produces,. Fixed Cost Is The Cost.

From www.educba.com

Average Fixed Cost Formula Step by Step Solutions (Calculator) Fixed Cost Is The Cost They remain constant, within capacity limits of a. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Graphs of mc, avc and atc. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. A fixed. Fixed Cost Is The Cost.

From www.educba.com

Fixed Cost Vs Variable Cost Top 12 Key Differences & Examples Fixed Cost Is The Cost Marginal revenue and marginal cost. Marginal cost, average variable cost, and average total cost. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. They can be be used when calculating key business. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent,. Fixed Cost Is The Cost.

From efinancemanagement.com

Variable Costs and Fixed Costs Fixed Cost Is The Cost They can be be used when calculating key business. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Graphs of mc, avc and atc. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax,. Fixed Cost Is The Cost.

From avada.io

How to Calculate Fixed Cost? Formula, Guide and Examples Fixed Cost Is The Cost They can be be used when calculating key business. A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. Some examples of fixed costs may include insurance, rent,. They remain constant, within capacity limits of a. Fixed costs are expenses that do not change with increases or decreases in. Fixed Cost Is The Cost.

From napkinfinance.com

What is Fixed Cost vs. Variable Cost? Napkin Finance Fixed Cost Is The Cost A fixed cost is a business expense that does not vary even if the level of production or sales changes. Marginal cost, average variable cost, and average total cost. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. A fixed cost is a business expense that remains unchanged, no matter. Fixed Cost Is The Cost.

From blog.hubspot.com

Fixed Cost What It Is & How to Calculate It Fixed Cost Is The Cost A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume. Fixed Cost Is The Cost.

From agiled.app

Differences Between Fixed Cost and Variable Cost Fixed Cost Is The Cost Marginal cost, average variable cost, and average total cost. Marginal revenue and marginal cost. Graphs of mc, avc and atc. Some examples of fixed costs may include insurance, rent,. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs are expenses that remain. Fixed Cost Is The Cost.

From tutorstips.com

Difference between Fixed Cost and Variable Cost Tutor's Tips Fixed Cost Is The Cost They can be be used when calculating key business. Graphs of mc, avc and atc. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. Fixed costs are a type. Fixed Cost Is The Cost.

From www.akounto.com

Fixed Cost Definition, Calculation & Examples Akounto Fixed Cost Is The Cost Some examples of fixed costs may include insurance, rent,. They remain constant, within capacity limits of a. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and depreciation. A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or. Fixed Cost Is The Cost.

From www.educba.com

What is Fixed Cost? Formula & Examples Advantages & Disadvantages Fixed Cost Is The Cost Marginal cost, average variable cost, and average total cost. They remain constant, within capacity limits of a. Marginal revenue and marginal cost. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and depreciation. Some examples of fixed costs may include insurance, rent,. A fixed cost is a business. Fixed Cost Is The Cost.

From www.intelligenteconomist.com

Theory Of Production Cost Theory Intelligent Economist Fixed Cost Is The Cost Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and depreciation. Marginal cost, average variable cost, and average total cost. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Some examples of fixed costs may include insurance, rent,.. Fixed Cost Is The Cost.

From oer.pressbooks.pub

Understanding the cost equation Accounting and Accountability Fixed Cost Is The Cost A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. Graphs of mc, avc and atc. They remain constant, within capacity limits of a. Marginal cost, average variable cost, and average total cost. They can be be used when calculating key business. Fixed costs are expenses that do not. Fixed Cost Is The Cost.

From penpoin.com

Total Variable Cost Examples, Curve, Importance Fixed Cost Is The Cost Graphs of mc, avc and atc. Marginal revenue and marginal cost. A fixed cost is a business expense that does not vary even if the level of production or sales changes. They remain constant, within capacity limits of a. Marginal cost, average variable cost, and average total cost. Some examples of fixed costs may include insurance, rent,. A fixed cost. Fixed Cost Is The Cost.

From cfoperspective.com

Choose the Right Type of Costs to Make the Best Decision Fixed Cost Is The Cost Marginal revenue and marginal cost. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and depreciation. A fixed cost is a business expense that remains unchanged, no matter how. Fixed Cost Is The Cost.

From www.youtube.com

Fixed Cost Vs Variable Cost Difference Between them with Example Fixed Cost Is The Cost A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. Marginal revenue and marginal cost. They can be be used when calculating key business. Graphs of mc, avc and atc. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property. Fixed Cost Is The Cost.

From riable.com

Fixed Costs Riable Fixed Cost Is The Cost They can be be used when calculating key business. A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs are expenses that. Fixed Cost Is The Cost.

From www.marketing91.com

Average Fixed Cost Definition, Formula and Examples Marketing91 Fixed Cost Is The Cost Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Some examples of fixed costs may include insurance, rent,. Fixed costs are expenses that remain the. Fixed Cost Is The Cost.

From sendpulse.ng

What is an Average Fixed Cost Basics Definition SendPulse Fixed Cost Is The Cost They can be be used when calculating key business. Some examples of fixed costs may include insurance, rent,. Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. A fixed cost is a business expense that does not vary even if the level of production. Fixed Cost Is The Cost.

From learnbusinessconcepts.com

Fixed Cost Explanation, Formula, Calculation, and Examples Fixed Cost Is The Cost Graphs of mc, avc and atc. Marginal cost, average variable cost, and average total cost. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. Fixed costs are expenses that. Fixed Cost Is The Cost.

From www.sagesoftware.co.in

Fixed Costs What It Is and How It's Used in Business Fixed Cost Is The Cost A fixed cost is a business expense that remains unchanged, no matter how much a company grows its revenue or produces. They can be be used when calculating key business. Graphs of mc, avc and atc. Fixed costs are expenses that remain the same no matter how much a company produces, such as rent, property tax, insurance, and depreciation. Some. Fixed Cost Is The Cost.

From joiytmunv.blob.core.windows.net

Fixed Cost Microeconomics at Fred Bremner blog Fixed Cost Is The Cost Fixed costs are a type of expense or cost that remains unchanged with an increase or decrease in the volume of goods or services sold. A fixed cost is a business expense that does not vary even if the level of production or sales changes. Fixed costs are expenses that do not change with increases or decreases in a company’s. Fixed Cost Is The Cost.

From www.1099cafe.com

What is a Fixed Cost Variable vs Fixed Expenses — 1099 Cafe Fixed Cost Is The Cost A fixed cost is a business expense that does not vary even if the level of production or sales changes. They can be be used when calculating key business. Graphs of mc, avc and atc. Marginal cost, average variable cost, and average total cost. Marginal revenue and marginal cost. A fixed cost is a business expense that remains unchanged, no. Fixed Cost Is The Cost.

From www.educba.com

Fixed Cost Formula Calculator (Examples with Excel Template) Fixed Cost Is The Cost They can be be used when calculating key business. They remain constant, within capacity limits of a. A fixed cost is a business expense that does not vary even if the level of production or sales changes. Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Fixed costs are expenses. Fixed Cost Is The Cost.

From cruseburke.co.uk

Fixed Cost and Variable Cost What's the Difference? CruseBurke Fixed Cost Is The Cost Fixed costs are expenses that do not change with increases or decreases in a company’s production or sales volumes. Marginal cost, average variable cost, and average total cost. They remain constant, within capacity limits of a. Some examples of fixed costs may include insurance, rent,. Fixed costs are expenses that remain the same no matter how much a company produces,. Fixed Cost Is The Cost.