In a world where resources grow increasingly limited, understanding the true cost of scarcity is essential for sustainable growth and competitiveness.

Understanding Additional Costs from Scarce Resources

When resources such as raw materials, skilled labor, or energy become scarce, their cost often rises sharply due to market dynamics, supply chain disruptions, and heightened demand. This escalation isn't just a price tag—it reflects deeper economic pressures that can disrupt budgets, delay projects, and threaten operational stability. Businesses must recognize these hidden costs to maintain financial resilience and strategic agility.

Factors Driving Up Costs in Scarce Environments

Several key factors amplify the cost of scarce resources: limited supply from geopolitical constraints, increased competition among buyers, rising transportation expenses, and regulatory hurdles. Additionally, technological bottlenecks and labor shortages further drive up premiums. These elements combine to create a volatile landscape where traditional budgeting falls short, demanding proactive and data-driven planning.

Strategies to Mitigate Additional Expenses

To manage additional costs effectively, organizations should adopt diversified sourcing, invest in resource efficiency technologies, and build strategic reserves. Forecasting models that incorporate scarcity indicators enable smarter procurement decisions. Long-term partnerships with suppliers and innovation in substitution or recycling can also reduce dependency and stabilize costs over time.

Conclusion: Building Resilience Through Cost Awareness

Acknowledging and quantifying the additional cost of scarce resources is no longer optional—it's a strategic imperative. By integrating scarcity insights into financial and operational planning, businesses can safeguard margins, enhance agility, and turn resource constraints into competitive advantages. Proactive management ensures sustainability and long-term success in an evolving marketplace.

Embracing a forward-looking approach to resource scarcity transforms challenges into opportunities. Prioritize visibility, flexibility, and innovation to navigate higher costs with confidence and maintain momentum in a constrained world.

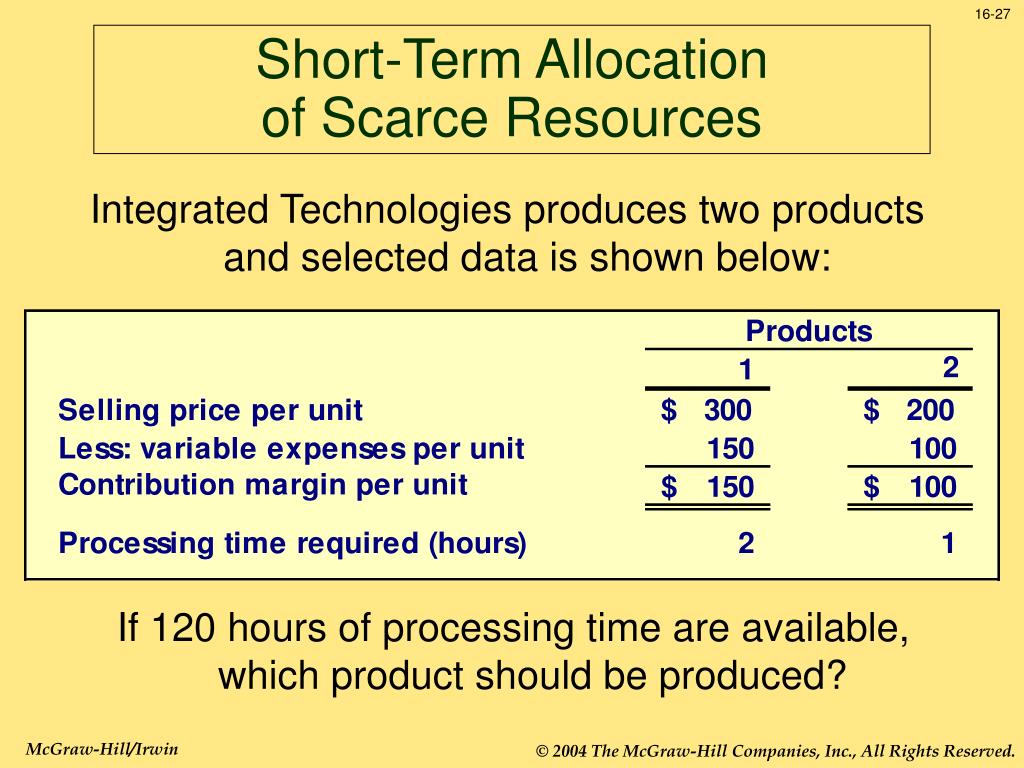

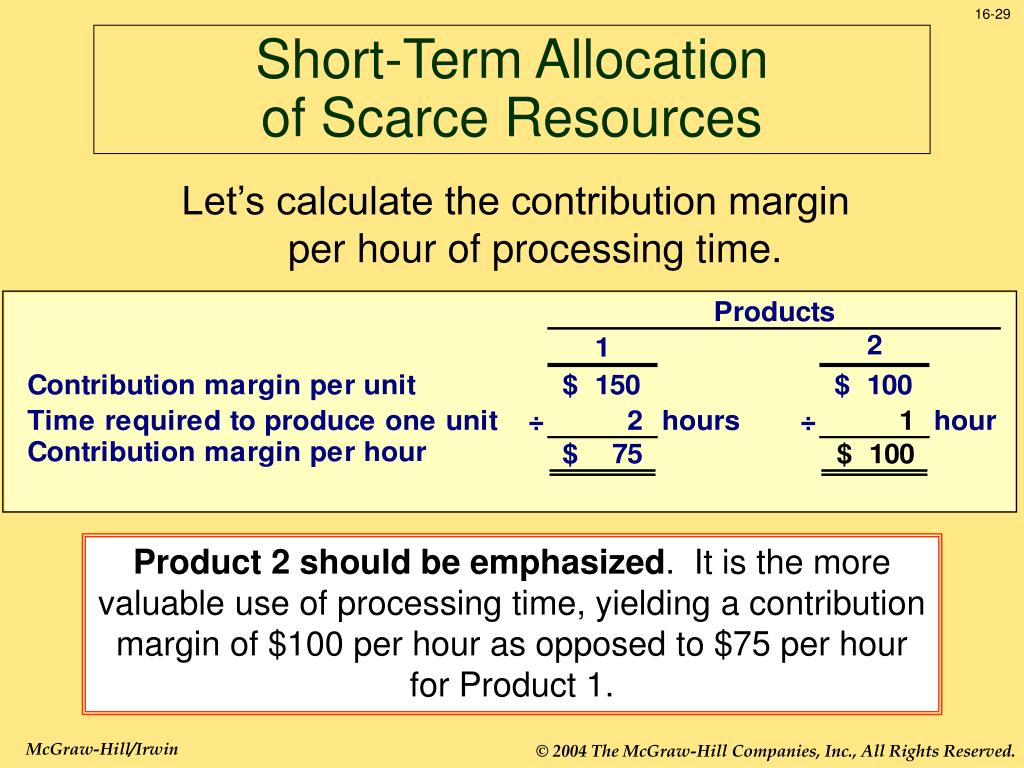

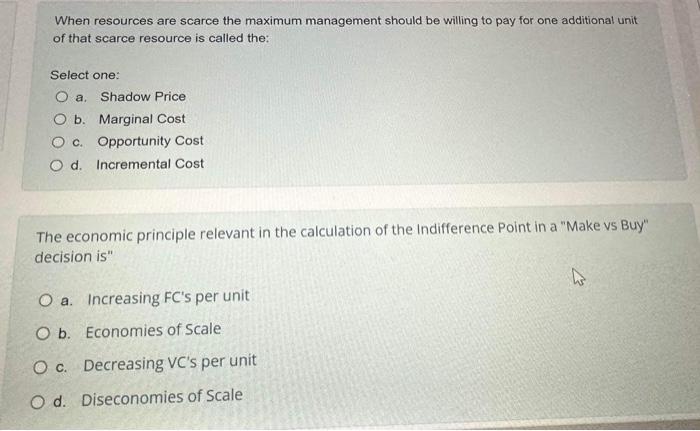

Contribution per unit = Sales price less variable cost per unit. 2. Divide the contribution per unit for each product, by the quantity of scarce resource required to make it.

Scarce resources or those with high market demand may drive up costs, making the incremental cost analysis more challenging. On the other hand, readily available and affordable resources can contribute to lower incremental costs. Learn how to effectively allocate limited resources to maximize profits in managerial accounting, focusing on relevant costs and short.

The contribution margin per unit of the scarce resource can be used to assess the value of relaxing the constraint. When there is unsatisfied demand for a single product because of a constraint, the value of additional time on the constraint is simply the contribution margin per unit of the scarce resource for that product. The contribution per unit of scarce resource and the internal opportunity cost g insights into the measurement of the opportunity cost of scarce resources.

In Chapter 15 we defined the opportunity cost of a resource as "the maximum benefit which could. Linear programming - assumptions a single quantifiable objective each product always uses the same quantity of the scarce resource per unit. the contribution (or cost) per unit is constant for each product, regardless of the level of activity.

Therefore, the objective function is a straight line. products are independent the focus is short. Scarce resource utilization (or allocation) decision is a judgment regarding the best use of scarce resources so as to maximize the total net income of a business.

Such decision is based on the contribution margin per unit of scarce resource from each product. Study with Quizlet and memorise flashcards containing terms like Contribution per unit formula, Relevant costs must have these 3 characteristics, What analysis is used when there is only one scarce resource? and others. Step 1 Identify scarce resource Calculate contribution per unit (unit selling price- Step 2 unit variable cost) Calculate contribution per unit of scarce resource Step 3 for each product Rank products: (highest contribution per unit of scarce resource first).

State decision (production plan based on ranking of products) Step 4 Optimal Plan.