Reducing the principal on a loan term isn’t just a financial adjustment—it’s a strategic move that unlocks significant savings over time. Understanding how much additional principal to reduce can transform your financial trajectory and accelerate debt freedom.

How Much Additional Principal to Reduce for Maximum Savings

The optimal amount to reduce your loan principal depends on monthly cash flow, interest costs, and long-term goals. Typically, reducing the principal by 10% to 20% can cut total interest by 15% to 30% over the remaining term. For example, reducing a $300,000 loan by $30,000 (10%) over 30 years may save thousands in interest, freeing up income for investments or emergency savings. Use loan payoff calculators to model scenarios based on your rate, term, and extra payments.

The Mechanics: Interest Savings and Principal Reduction

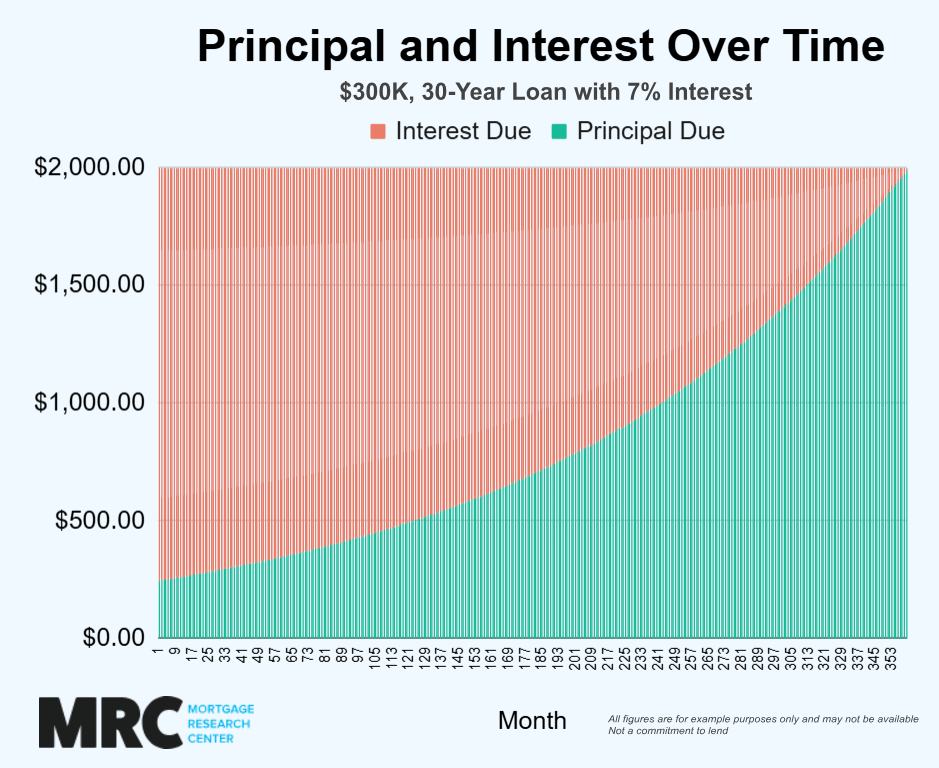

Principal reduction lowers monthly interest charges because interest is calculated on a smaller balance. This compounding effect means every dollar paid early saves more over time. Reducing principal accelerates payoff, shortens term flexibility, and improves debt-to-income ratios—beneficial for future borrowing. Even small incremental reductions compound significantly, making disciplined extra principal payments a powerful wealth-building tool.

Practical Strategies to Increase Additional Principal Payments

To maximize additional principal, consider automating larger monthly payments, applying windfalls like bonuses or tax refunds toward principal, or refinancing to a shorter term with higher principal portions. These steps compound savings, reduce total interest, and fast-track full loan ownership—improving long-term financial health and stability.

Conclusion: Take Control of Your Loan’s Future

Understanding how much additional principal to reduce is key to minimizing costs and accelerating financial freedom. By making strategic extra payments and leveraging loan tools, you transform your loan from a burden into a stepping stone toward greater savings and security. Start today—calculate your savings potential and take the first step toward smarter debt management.

Maximizing principal reduction isn’t just about cutting payments—it’s about maximizing returns. With precise calculations and intentional adjustments, you can reduce your loan term strategically, save thousands in interest, and strengthen your financial future. Begin today and unlock lasting value.

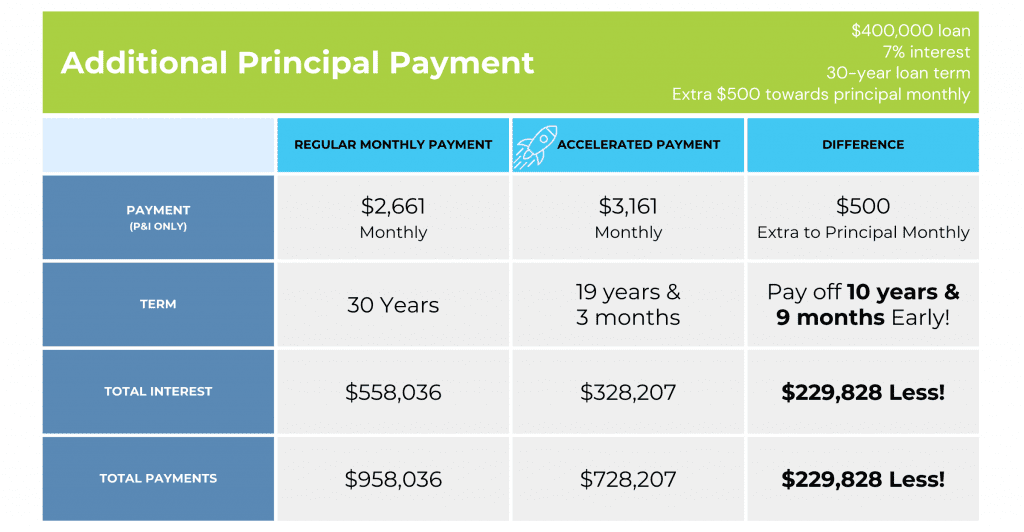

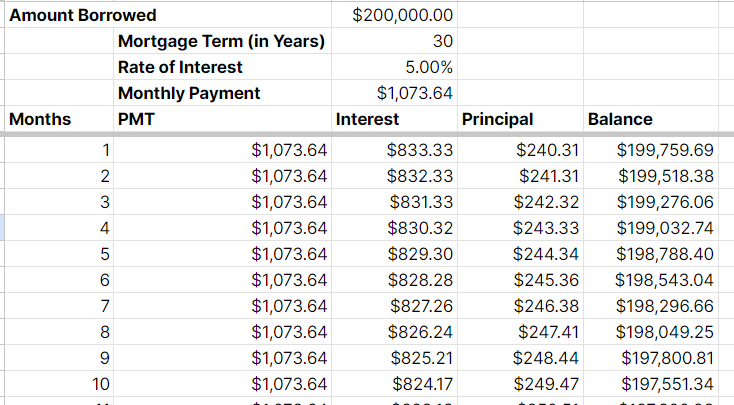

Extra payments toward the principal reduce the balance more quickly, but they generally shorten the loan term rather than lower the required monthly payment, unless you refinance or the lender recalculates the payment schedule. A financial advisor can help you evaluate whether making extra mortgage payments fits your budget and long. Mortgage Payoff Calculator This mortgage payoff calculator helps evaluate how adding extra payments or bi.

Paying extra toward your mortgage principal-whether monthly, bi‑weekly, or in lump sums. When a borrower makes additional principal payments to reduce the balance, he is essentially reducing interest payments on his loan. Depending on the size of the loan and the extra payments, and the number of additional payments the borrower makes, he could pay off his loan much earlier than the original term.

Benefits of paying extra on a. Put extra money-like a tax refund, work bonus, or inheritance-directly toward your loan's principal. Even a single lump.

Practicing this discipline on a monthly basis would reduce the standard 30-year loan to 15 years. However, as the loan progresses, the ratio of interest and principal inverts so that eventually the principal represents the majority of the payment. A borrower continues to match the principal amount with an additional payment.

Use a mortgage payoff calculator with extra principal payments to see how steady monthly extras, yearly lump sums, and one. Principal curtailment is a powerful tool for reducing the overall cost of a loan. By making additional payments towards the principal, borrowers can reduce the interest paid over the life of the loan and shorten the loan term.

Additional Principal Payment Extra payments applied to the mortgage above the monthly requirement. These payments are typically used to settle existing late charges or fees before being applied to the principal. Have you considered the benefits of paying your mortgage off sooner?

Use our Extra Principal Mortgage Calculator to see how monthly extra payments reduce interest and shorten your loan term fast.