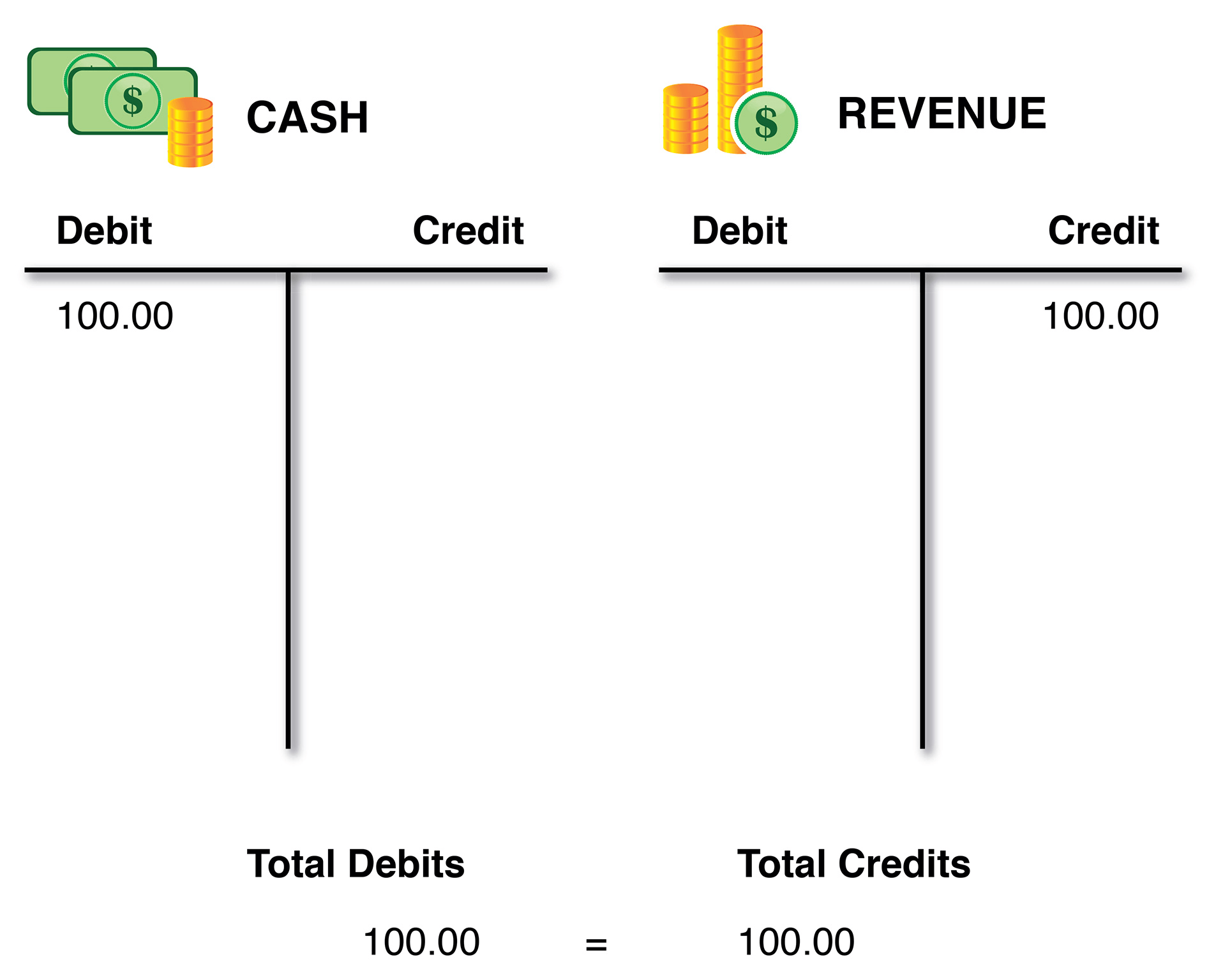

Understanding a T chart accounting format is essential for anyone looking to grasp the fundamentals of double-entry bookkeeping. This simple visual tool provides a clear framework for analyzing how every financial transaction impacts a business, ensuring that the fundamental equation of assets equaling liabilities plus equity always remains balanced. By separating debits and credits into two distinct columns, it serves as the foundational building block for transitioning from manual records to complex accounting software.

Core Mechanics of the T Account Structure

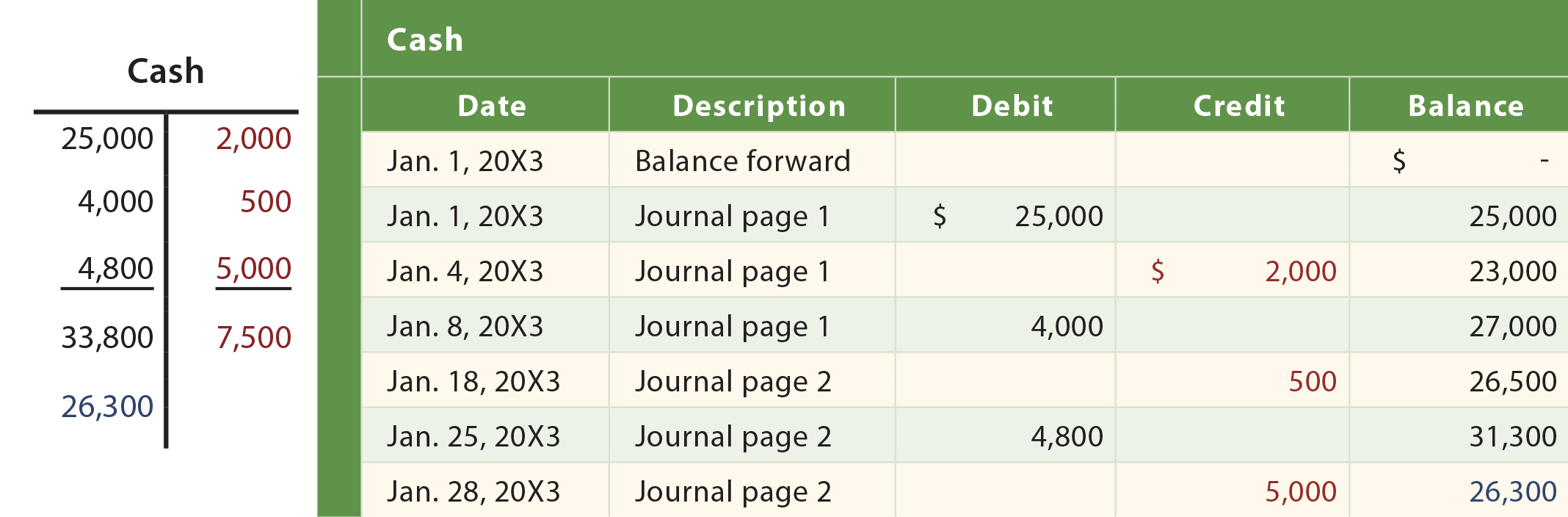

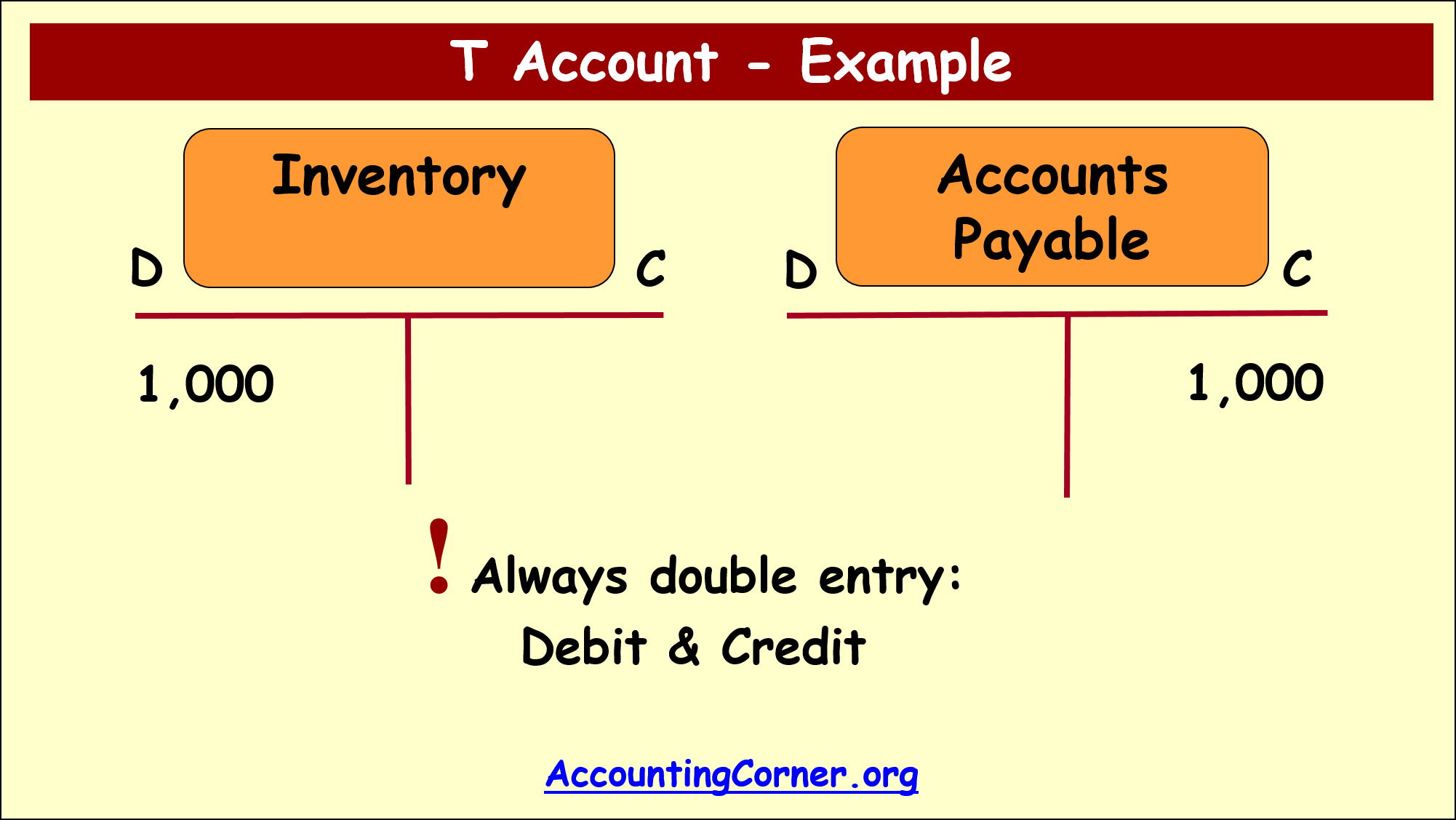

The structure is named for its resemblance to the letter "T," with the account title placed at the top of a vertical line and the horizontal top of the "T." The left side represents the debit column, while the right side represents the credit column. Unlike single-entry systems that track cash flow only, this method records both the source and the destination of every financial movement. This inherent design forces the bookkeeper to think in terms of dual effects, which drastically reduces the risk of errors going unnoticed.

Decoding Debits and Credits

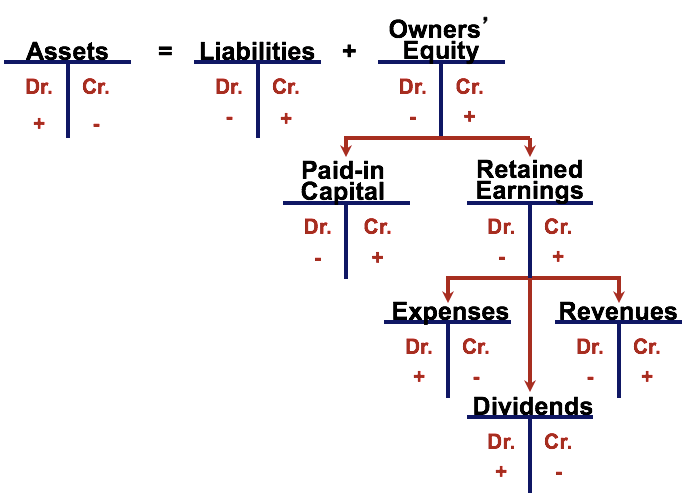

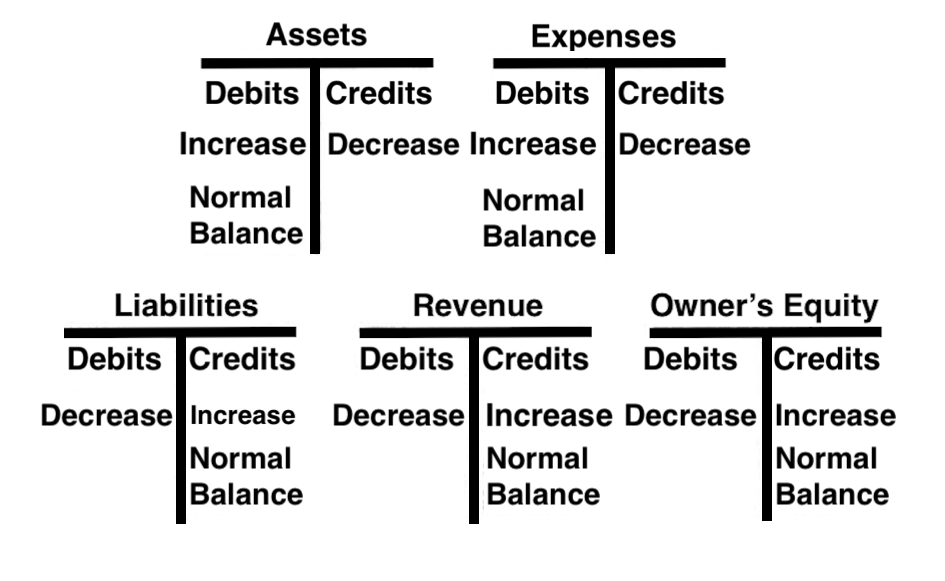

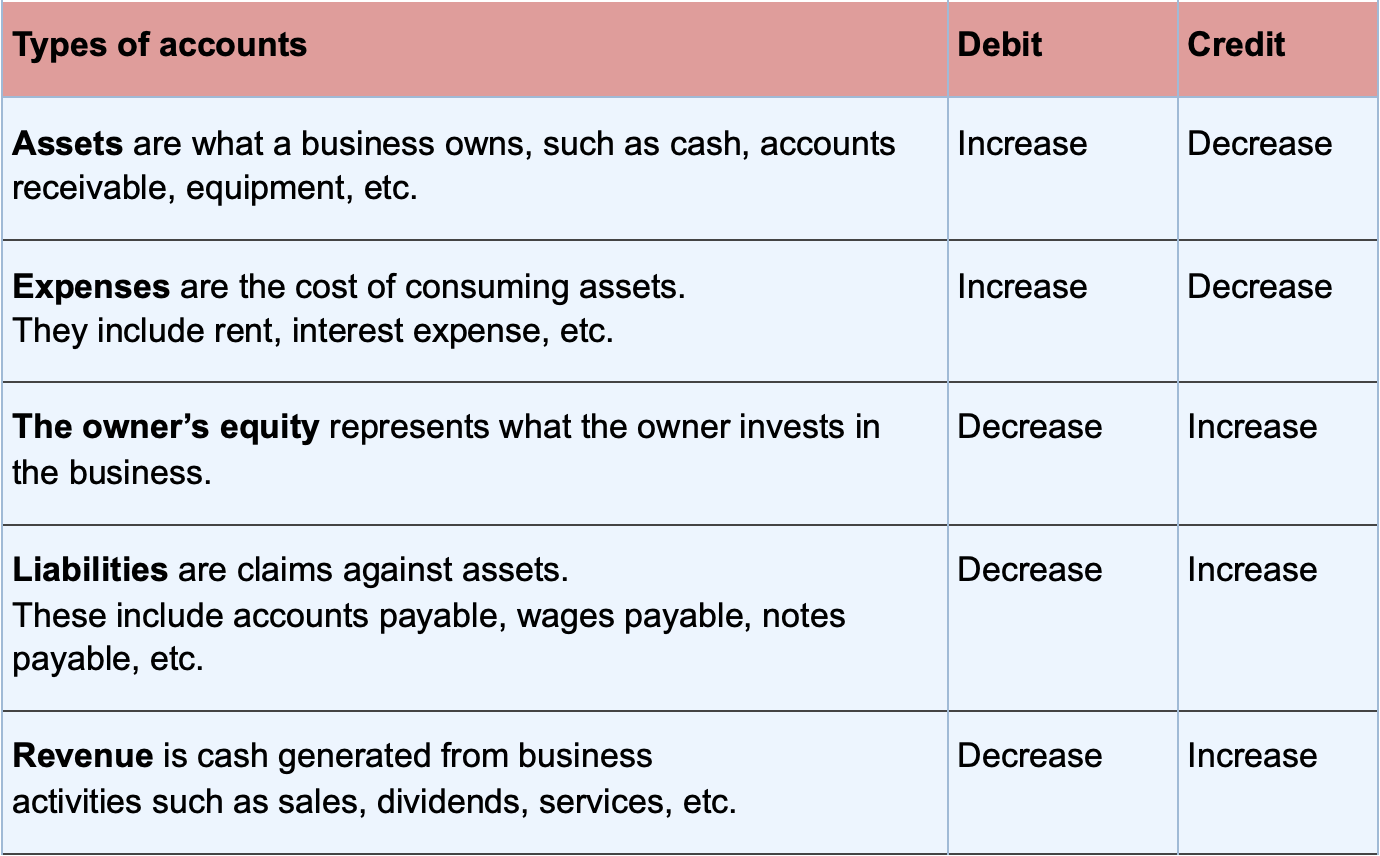

Perhaps the most confusing aspect for beginners is the concept of debits and credits, which are often mistakenly associated with positive and negative values. In reality, the effect of a debit or credit depends entirely on the type of account being referenced. For asset and expense accounts, a debit increases the balance while a credit decreases it. Conversely, for liability, equity, and revenue accounts, a credit increases the balance while a debit decreases it. Mastering this logic is the key to accurately mapping any transaction onto the T chart.

Practical Examples: Assets and Cash Flow

To illustrate this concept, consider a business that purchases a new server for $3,000 using cash. In this scenario, the asset account "Equipment" would be increased, requiring a debit entry on the left side of its T account. Simultaneously, the asset account "Cash" would be decreased, necessitating a credit entry on the right side. This demonstrates the conservation of value; the total assets remain the same, merely shifting from one category to another, which keeps the T chart in perfect balance.

| Account | Debit | Credit |

|---|---|---|

| Equipment | $3,000 | |

| Cash | $3,000 |

Liabilities, Equity, and Revenue Dynamics

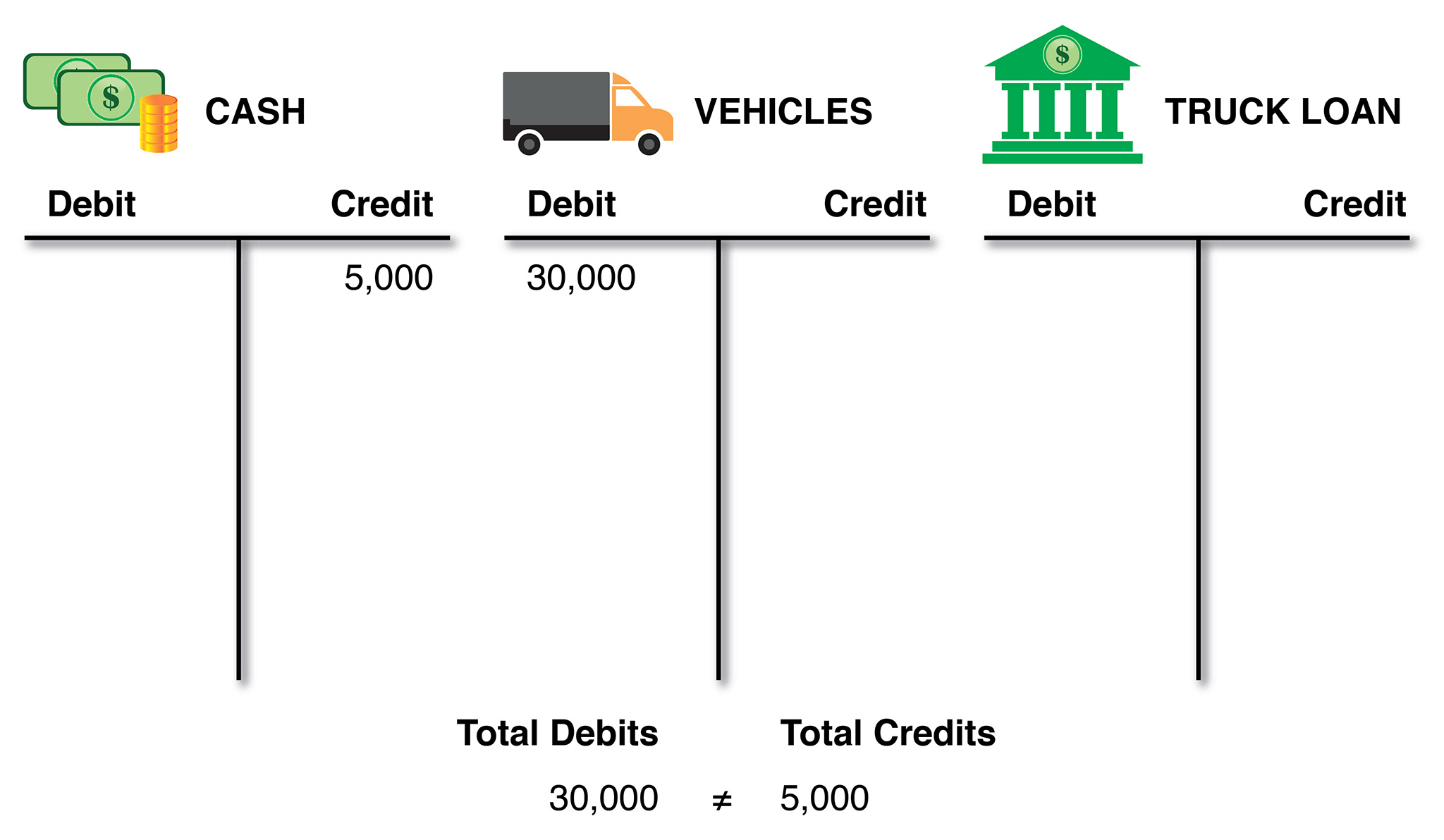

Another common scenario involves a business taking out a loan from a bank for $5,000. Here, the T chart analysis becomes crucial for understanding capital structure. The business receives cash, so the asset account "Cash" is debited on the left. However, because the business now owes money, the liability account "Loan Payable" is credited on the right. This transaction highlights how the chart separates the impact on the asset side from the impact on the financing side, providing a clear picture of obligations.

| Account | Debit | Credit |

|---|---|---|

| Cash | $5,000 | |

| Loan Payable | $5,000 |

Revenue Recognition and Expense Tracking

When the business renders a service and invoices a client for $1,200, the revenue logic comes into play. Revenue accounts increase with a credit, so the "Services Revenue" account is credited on the right side. Simultaneously, the asset account "Accounts Receivable" is debited on the left because the business has earned an asset in the form of a future cash claim. On the expense side, if the company pays $400 for advertising, the "Advertising Expense" account is debited to reflect the cost, and the "Cash" account is credited to show the outflow of resources.

| Account | Debit | Credit |

|---|---|---|

| Accounts Receivable | $1,200 | |

| Services Revenue | $1,200 | ]lt;/tr>

While digital tools automate much of the heavy lifting, the T chart remains the most effective educational instrument in the accounting arsenal. It builds intuition for financial relationships and ensures that every entry is logically sound before it is posted to the general ledger. By consistently applying these principles, professionals can maintain clean records and provide accurate financial reporting with confidence.

Accounting T Charts – emmamcintyrephotography.com

T Chart Accounting Examples

T Chart Accounting Examples

T-accounts - Basics of Accounting & Information Processing

T Accounting Examples - T Accounts for Beginners

What is a T-Account? Accounting Student Guide – Accounting How To

T-Account in Accounting | Definition | Example | Template

What Are T Accounts and Why Do You Need Them? - Baremetrics

T-Accounts Explained (With Examples) | Brixx

T Account Examples | Step by Step Guide to T-Accounts with Examples

T Accounts Template

T-Accounts Explained (With Examples) | Brixx

39+ T Chart Templates - DOC, PDF

3.5: Use Journal Entries to Record Transactions and Post to T-Accounts ...

T Account in Accounting | Definition | Example | Template

/T-Account_2-cf96e42686cc4a028f0e586995b45431.png)

T Account Template

T-Accounts - principlesofaccounting.com

T Accounts | Accounting Corner

T Account Examples | Step by Step Guide to T-Accounts with Examples

Accounting Basics: T Accounts