Understanding the Basics: A Beginner's Guide to Accounting

Introduction

Welcome to "Understanding the Basics: A Beginner's Guide to Accounting." In this comprehensive guide, we will delve into the fundamental concepts and principles of accounting. Whether you are an aspiring accountant or a business owner looking to gain a better understanding of financial management, this article will equip you with the knowledge needed to navigate the world of accounting confidently. So let's dive in!

Understanding the Basics: A Beginner's Guide to Accounting

Accounting is often referred to as the language of business. It is a system that allows individuals and organizations to record, analyze, and interpret financial transactions. By providing valuable insights into financial health, accounting plays a crucial role in decision-making processes.

What is Accounting?

Accounting can be defined as the process of identifying, measuring, and communicating economic information to various stakeholders. It involves recording and summarizing financial transactions, preparing financial statements, and interpreting the results.

Why is Accounting Important?

Accounting provides a clear picture of an organization's financial position and performance. It helps in evaluating profitability, good accountant assessing solvency, and making informed decisions based on accurate data. Additionally, accounting ensures compliance with legal requirements and enables effective management of resources.

Key Principles of Accounting

Types of Accounting

Accounting can be broadly categorized into four main types:

1. Financial Accounting

Financial accounting focuses on recording and reporting financial transactions for external stakeholders such as investors, creditors, and regulatory authorities. It involves preparing financial statements, including the balance sheet, income statement, and cash flow statement.

2. Managerial Accounting

Managerial accounting is concerned with providing internal stakeholders, such as managers and executives, with relevant financial information for decision-making purposes. It involves analyzing costs, budgets, and performance metrics to support strategic planning and control within an organization.

3. Tax Accounting

Tax accounting deals with the preparation and filing of tax returns in compliance with applicable tax laws and regulations. Its primary focus is on calculating taxable income, determining tax liabilities or refunds, and ensuring adherence to tax deadlines.

4. Auditing

Auditing involves examining an organization's financial records to ensure accuracy, integrity, and compliance with accounting standards. External auditors provide independent assessments of financial statements to enhance investor confidence and detect any potential fraud or misrepresentation.

Understanding Basic Accounting Concepts

To develop a strong foundation in accounting, it is essential to understand some basic concepts that underpin the discipline. Let's explore a few key concepts:

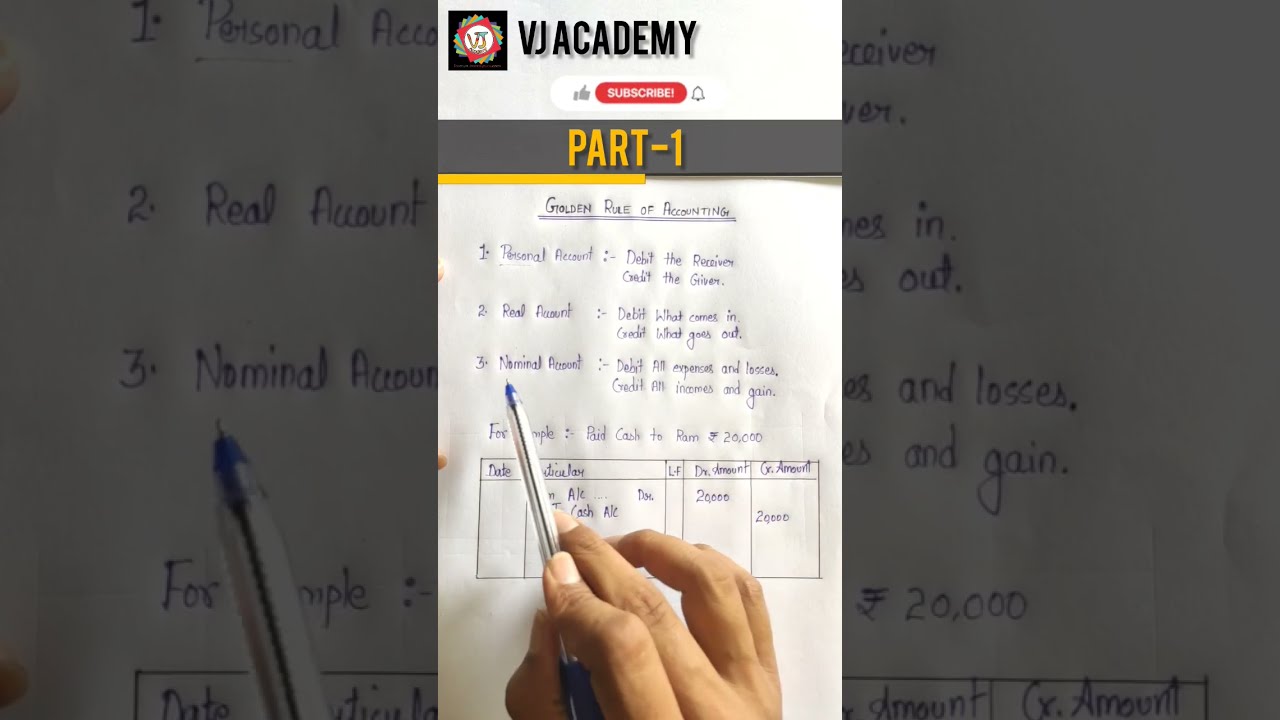

1. Double-Entry Bookkeeping

Double-entry bookkeeping is a fundamental concept in accounting that follows the principle of duality. It states that every transaction affects at least two accounts—a debit entry and a corresponding credit entry—ensuring that the equation Assets = Liabilities + Equity remains in balance.

2. Debits and Credits

Debits and credits are used to record transactions in the general ledger using T-accounts. Debits increase asset accounts and decrease liability and equity accounts, while credits decrease asset accounts and increase liability and equity accounts.

3. Chart of Accounts

A chart of accounts is a categorized listing of all the accounts used by an organization to record financial transactions. It provides a systematic framework for organizing and classifying various types of transactions.

4. Financial Statements

Financial statements are formal reports that summarize an organization's financial activities, performance, and position. The three primary financial statements are the balance sheet, income statement, and cash flow statement.

Frequently Asked Questions (FAQs)

What qualifications are required to become an accountant? To become an accountant, one typically needs a bachelor's degree in accounting or a related field. Professional certifications such as Certified Public Accountant (CPA) or Chartered Accountant (CA) can also enhance career prospects.

What software is commonly used in accounting? Popular accounting software includes QuickBooks, Xero, Sage Intacct, and FreshBooks. These platforms offer features such as invoicing, expense tracking, financial reporting, and integration with other business tools.

What is the role of technology in modern accounting? Technology has revolutionized the accounting profession by automating repetitive tasks, improving accuracy, enabling real-time data analysis, and enhancing collaboration between accountants and clients.

How does accounting contribute to business decision-making? Accounting provides vital information on revenue generation, cost management, profitability analysis, and cash flow forecasting. This data aids in making informed decisions regarding investments, expansions, pricing strategies, and resource allocation.

Can individuals benefit from understanding basic accounting principles? Absolutely! Basic accounting knowledge can help individuals manage personal finances effectively, make better investment decisions, understand tax implications, and evaluate financial opportunities.

Are there ethical considerations in the field of accounting? Yes, ethics play a crucial role in accounting. Accountants are expected to adhere to professional codes of conduct, maintain client confidentiality, exercise objectivity, and avoid conflicts of interest.

Conclusion

In conclusion, "Understanding the Basics: A Beginner's Guide to Accounting" has provided a comprehensive overview of essential accounting concepts and principles. Whether you aspire to become an accountant or simply want to gain a better understanding of financial management, this guide has equipped you with the necessary knowledge to navigate the world of accounting confidently. Remember, accounting is not just about numbers; it is a powerful tool that enables informed decision-making and drives business success. So embrace the language of business and unlock your financial potential!