Turning a new Florida home or renovation project into a permanent loan is a critical step for homeowners and investors seeking long-term financial stability and property value retention.

Understanding Florida Construction Financing to Permanent Loans

After completing construction in Florida, securing a permanent loan—often a fixed-rate mortgage—depends on final inspections, occupancy certificates, and proof of insurance. Unlike temporary construction loans, permanent loans require full project completion and lender underwriting, ensuring the property meets both building codes and financing standards. This shift offers lower long-term risk and consistent payment terms, ideal for stable equity buildup.

Key Requirements for Conversion to Permanent Loans

To transition from construction to permanent financing, borrowers must submit final project documents including inspection reports, title verification, and proof of compliance with Florida’s stringent building regulations. Lenders also evaluate the property’s market value, borrower’s creditworthiness, and debt-to-income ratio. Proactive coordination with lenders and contractors accelerates approval and minimizes delays.

Strategies for a Smooth Transition to Permanent Loans

Proactive planning is essential: maintain detailed records, engage experienced lenders familiar with Florida’s market, and anticipate closing costs and maintenance reserves. Exploring government-backed loan programs like FHA or VA options can further improve terms. Staying informed about local regulations and financing incentives helps optimize long-term ownership costs and ensures compliance with Florida’s evolving real estate landscape.

Conclusion and Next Steps

Successfully transitioning Florida construction to permanent loans unlocks lasting equity and financial security. By meeting lender criteria and leveraging expert guidance, homeowners and investors can confidently finalize financing and enjoy peaceful, long-term ownership. Begin your journey today by consulting a Florida-savvy mortgage professional.

From project completion to permanent loan approval, understanding Florida’s unique financing path empowers you to build or buy with confidence—secure your future with a well-planned permanent mortgage.

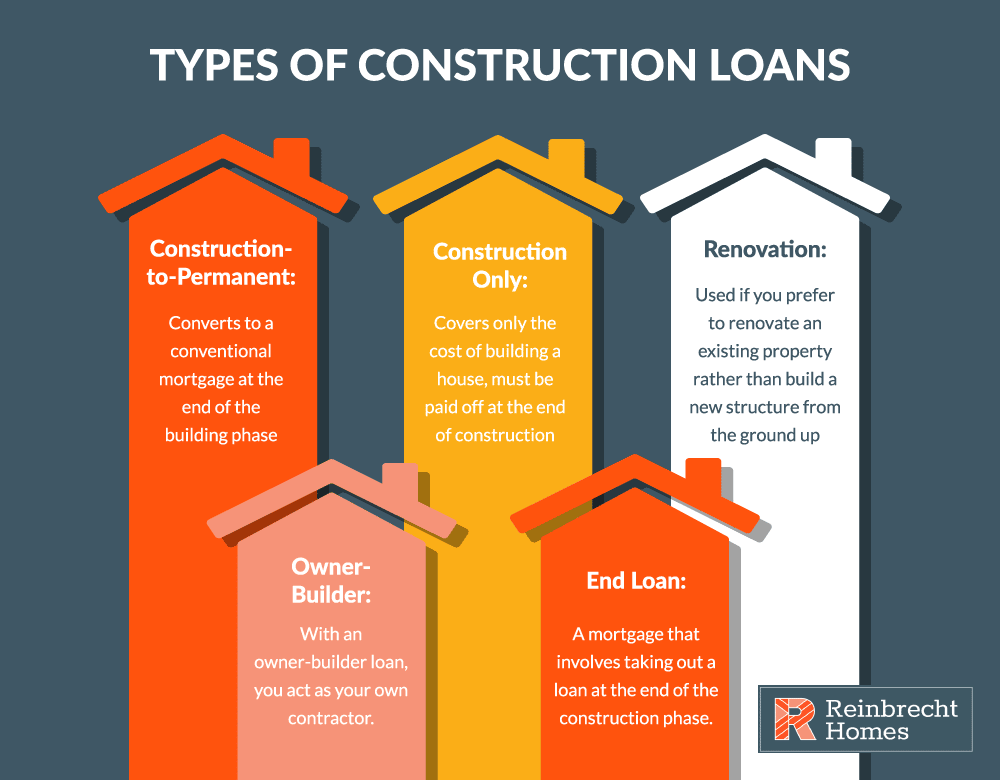

Construction-to-permanent financing are one-time loans that fund construction and then convert into a permanent mortgage. Fixed rate and variable rate mortgage loan options One-time closing, saving you in closing cost Up to 100% financing on primary residences Permanent rate is locked before construction starts Loan is an interest. Build your dream home with MIDFLORIDA Credit Union's construction-to-permanent loans-one loan, one closing, easy financing across Florida.

Construction loans in Florida are available in a wide array of options depending on the lender you choose and your personal financial situation. Through this process, you'll end up with your general contractor of choice and the documentation that you'll need to actually apply for your construction loan. Comparing Construction Loan Lenders First, check if a lender offers construction loans to a homebuyer.

If so, find out if the loans are construction to permanent. (Yes to both at SCCU! Explore your construction-to-permanent mortgages options and speak with a lender today to apply in Florida.

Contact us today to get started! One-Time Close Construction Loan (Single-Close Construction-to-Permanent)Build your new home from the ground up. Build your dream home with a Citizens construction.

Building a home? This piece describes construction to permanent loans, draw schedules, required down payments, and how Florida building codes influence financing. If you're looking to build a brand-new home on a lot you own, a bridge-to-permanent loan from Titan Funding of Boca Raton, Florida, could be the perfect loan for you. Bridge-to-perm loans, also known as construction-to-permanent loans or single-close loans, provide all the funding for construction costs and the permanent mortgage.

The main benefit is that there's only one closing. You don. One-Time Close construction loans are popular for those looking to build a new home on their own lot in Florida.

These government-backed loans are available through FHA, VA and USDA. They combine construction and permanent financing into a single loan, reducing paperwork, closing costs, and the risk of interest rate fluctuations.