Understanding how much additional super you can contribute before tax is key to maximizing your retirement savings while staying within tax compliance. With strategic planning, you can push contribution limits without triggering unintended tax consequences.

How Much Additional Super Can I Contribute Before Tax?

The amount of additional super you can contribute before hitting tax-related limitations depends on your current income, existing super balance, and applicable rules. For most contributors, increasing super contributions beyond 30% of earnings may trigger higher marginal tax rates and reduce net benefits. However, strategic timing—such as front-loading contributions during high-income years—can allow extra contributions without immediate tax penalties. Always review your tax bracket and consider the tax offset implications to ensure your additional super enhances long-term retirement value efficiently.

Key Tax Considerations for Extra Super Contributions

Super contributions above 30% of earnings may increase your taxable income, potentially reducing your net after-tax return. However, contributions made before age 55 or to a non-registered fund can avoid immediate tax impacts. Employer top-ups remain tax-free until age 55, offering a safe way to boost contributions. Understanding the tax offset and marginal rates ensures your extra super delivers maximum retirement growth without unexpected tax burdens.

Maximizing Contributions Without Crossing Tax Thresholds

To contribute beyond standard limits safely, align additional super with lower tax brackets, utilize non-taxable employer contributions, and plan ahead for tax-free investment windows. Using tools like super contribution recoupment or rolling over balances can optimize tax efficiency. Regular consultation with a tax advisor ensures your contributions remain compliant while maximizing retirement security.

Conclusion

Balancing additional super contributions with tax efficiency is essential for smart financial growth. By staying informed and planning strategically, you can enhance your retirement fund without triggering unwanted tax liabilities. Take control today—review your super statement, consult a professional, and contribute wisely to secure your financial future.

Maximizing your super contributions before tax requires awareness of income thresholds, tax rates, and strategic timing. By working within tax guidelines and leveraging available tools, you can contribute more effectively to your retirement while preserving your after-tax wealth. Start planning now to unlock your full super potential without tax surprises.

If you're 50+ and want to make catch-up contributions, here's what you need to know about how they work, contribution limits, and a new Roth requirement for high. Standard 401 (k) and IRA Catch-Up Contribution Limits Before we dive into so-called "super catch-ups," it helps to review standard catch-ups. (Catch.

IRS finalized rules on the optional higher "super catch-up" contribution limit for defined contribution plan participants ages 60. 2026 brings changes to your 401(k) cathc up contributions. Ignoring these changes could get you in trouble with the IRS or cause a suprise tax bill.

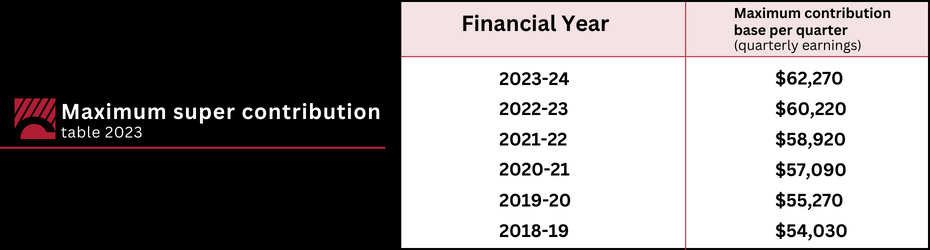

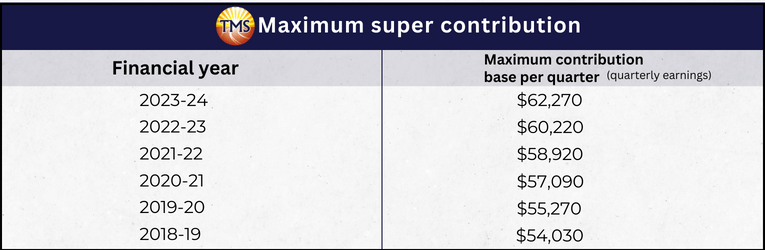

Adding to your super You can boost your retirement savings by making voluntary super contributions, such as by: setting up a salary sacrifice arrangement with your employer making personal super contributions (and a non-concessional contribution may make you eligible for the government's super co-contribution) transferring any super you have in a foreign super fund arranging for your spouse to. In addition, the amount of your compensation that can be taken into account when determining employer and employee contributions is limited to $345,000 for 2024 ($330,000 for 2023; $305,000 for 2022; $290,000 for 2021, $285,000 for 2020). Related 401 (k) plans Contribution limits if you're in more than one plan.

The IRS updates retirement contribution limits annually for inflation. Here are the 2026 limits and their impact, to help you make the most of your retirement savings. You can generally add to super in two ways: Before-tax1: including Superannuation Guarantee (SG), before-tax employee (salary sacrifice), extra employer and tax-deductible personal contributions.

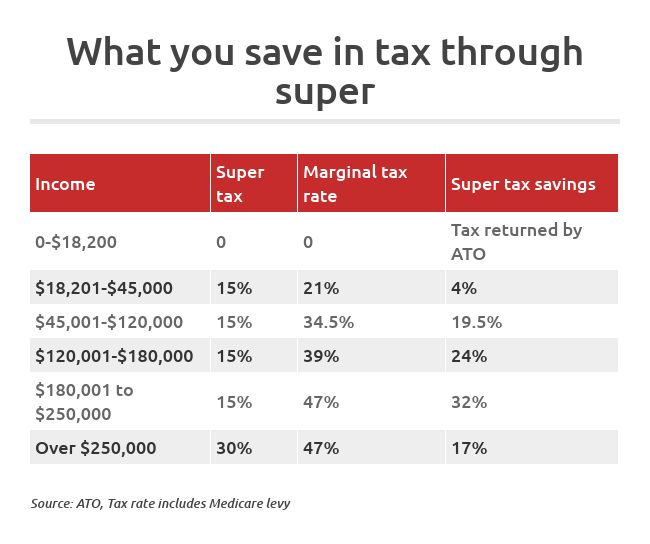

These are also called 'concessional' contributions. Concessional contributions You can make before-tax contributions, where contributions come out of your pay before income tax, such as salary sacrifice. You pay 15% tax on this money when it goes into your super (the Australian Taxation Office may apply an extra 15% if your income plus super contributions is more than $250,000 per year.) This compares to normal tax rates, which can be up to 45%.

Making extra super contributions will build your retirement nest-egg, as well as provide immediate and long-term tax benefits. So, what are extra super contributions and how much extra super contributions can you make?