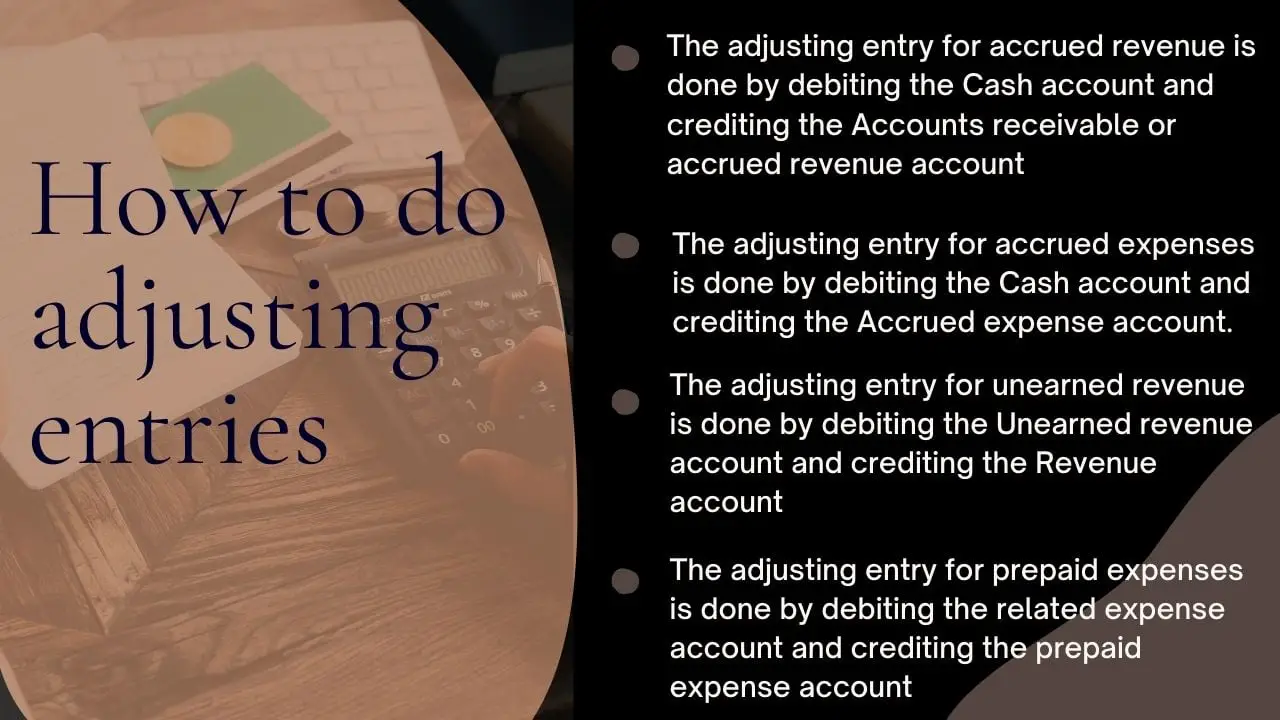

An adjusting entry is completed when accounting adjustments are recorded to reflect the true financial position of a period. These entries correct imbalances in accounts such as accrued revenues, accrued expenses, depreciation, prepaid items, and allowances, ensuring that revenue and expenses are recognized in the correct accounting period.

This process follows the matching principle and adheres to Generally Accepted Accounting Principles (GAAP), guaranteeing that financial statements present an accurate and fair view of a company’s performance. When an adjusting entry is completed, it updates relevant ledger accounts, aligns trial balances, and supports reliable month-end and year-end closing activities.

Key moments when an adjusting entry is completed include the close of an accounting period, after reviewing monthly transactions, and prior to financial statement preparation. Completing these entries promptly enhances audit readiness, improves internal controls, and strengthens stakeholder confidence in reported results.

In summary, an adjusting entry completed ensures financial data is precise, compliant, and reflective of actual business activity—essential for sound decision-making and regulatory adherence.

Mastering the completion of adjusting entries is fundamental to reliable accounting and effective financial management. By ensuring entries are accurate and timely, businesses uphold integrity in reporting, strengthen internal controls, and build trust with investors and regulators—key drivers for long-term success.

Everything you want to know about adjusting entries. Definition, explanation, examples, and purpose of preparing adjusting entries. This explanation teaches the essential process of preparing adjusting entries to convert accounting records from cash basis to accrual basis before issuing financial statements.

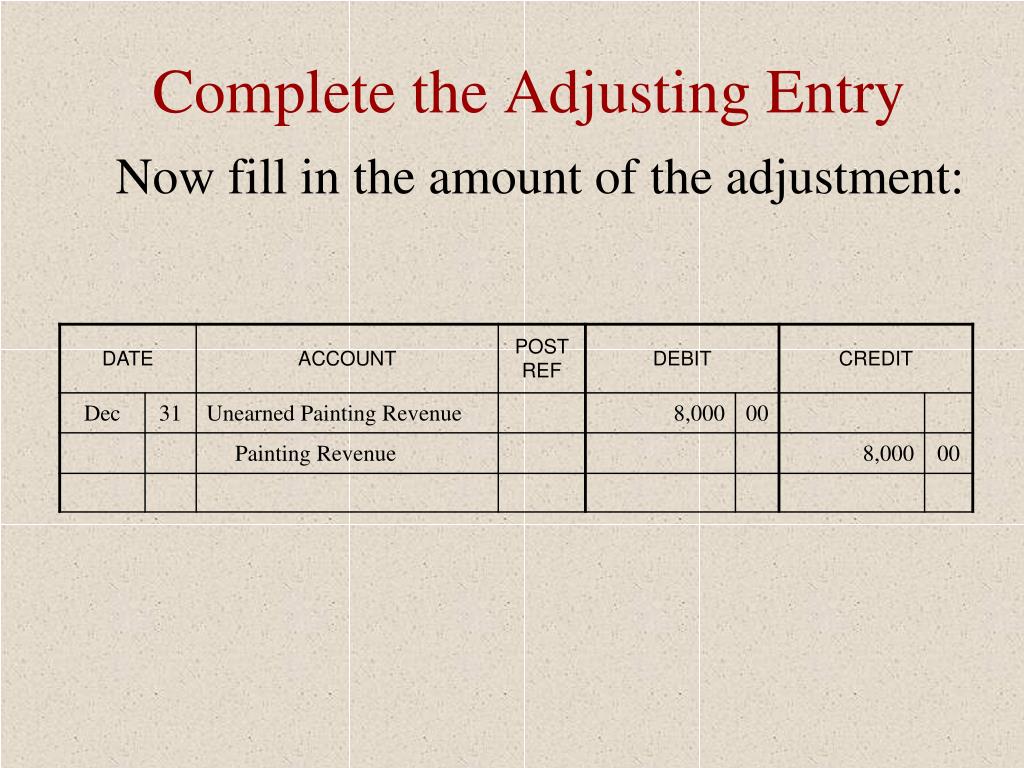

Using a detailed, step-by-step approach with T-accounts and visual aids, the content demonstrates how to review preliminary account balances and determine necessary adjustments. The explanation covers both major. Learn how to master adjusting entries for precise accounting.

Enhance your financial accuracy and streamline your reporting-read the essential guide now! At a later time, adjusting entries are made to record the associated revenue and expense recognition, or cash payment. A set of accrual or deferral journal entries with the corresponding adjusting entry provides a complete picture of the transaction and its cash settlement.

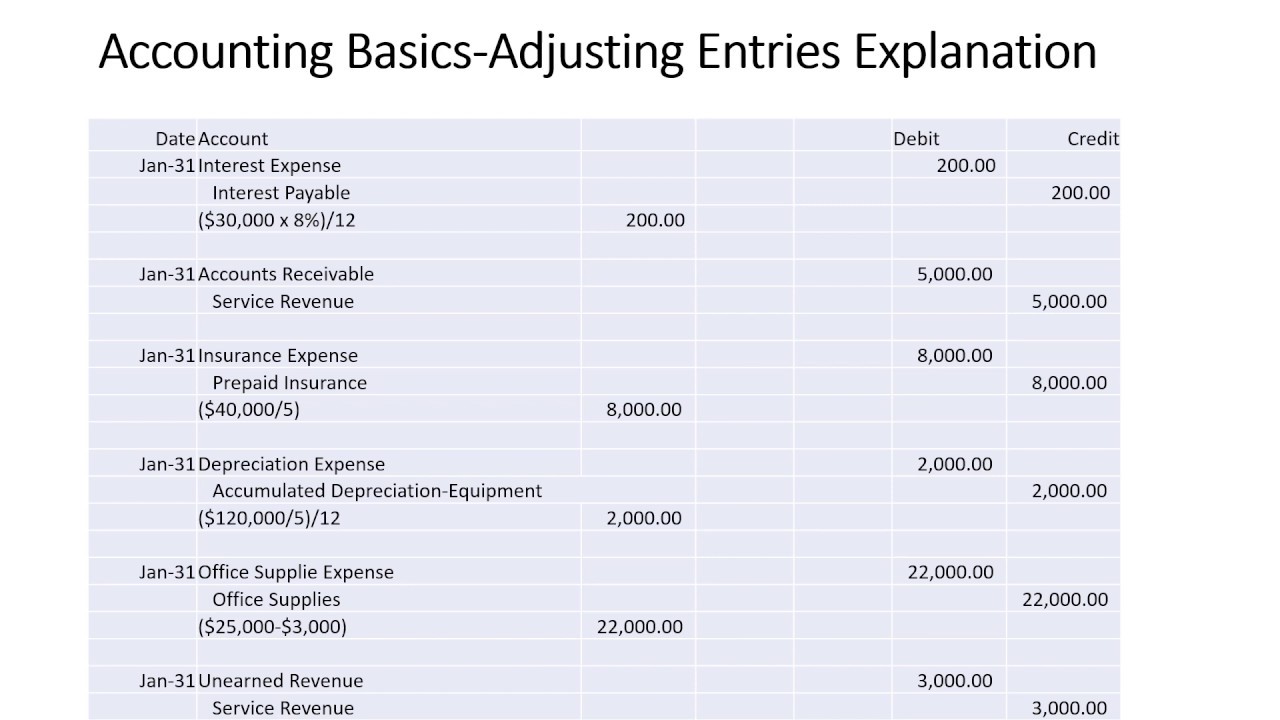

Dive deep into adjusting journal entries. We'll explore different types, provide examples, and discuss how and when to make journal entry adjustments. Adjusting entries are journal entries recorded at the end of an accounting period to alter the ending balances in various general ledger accounts.

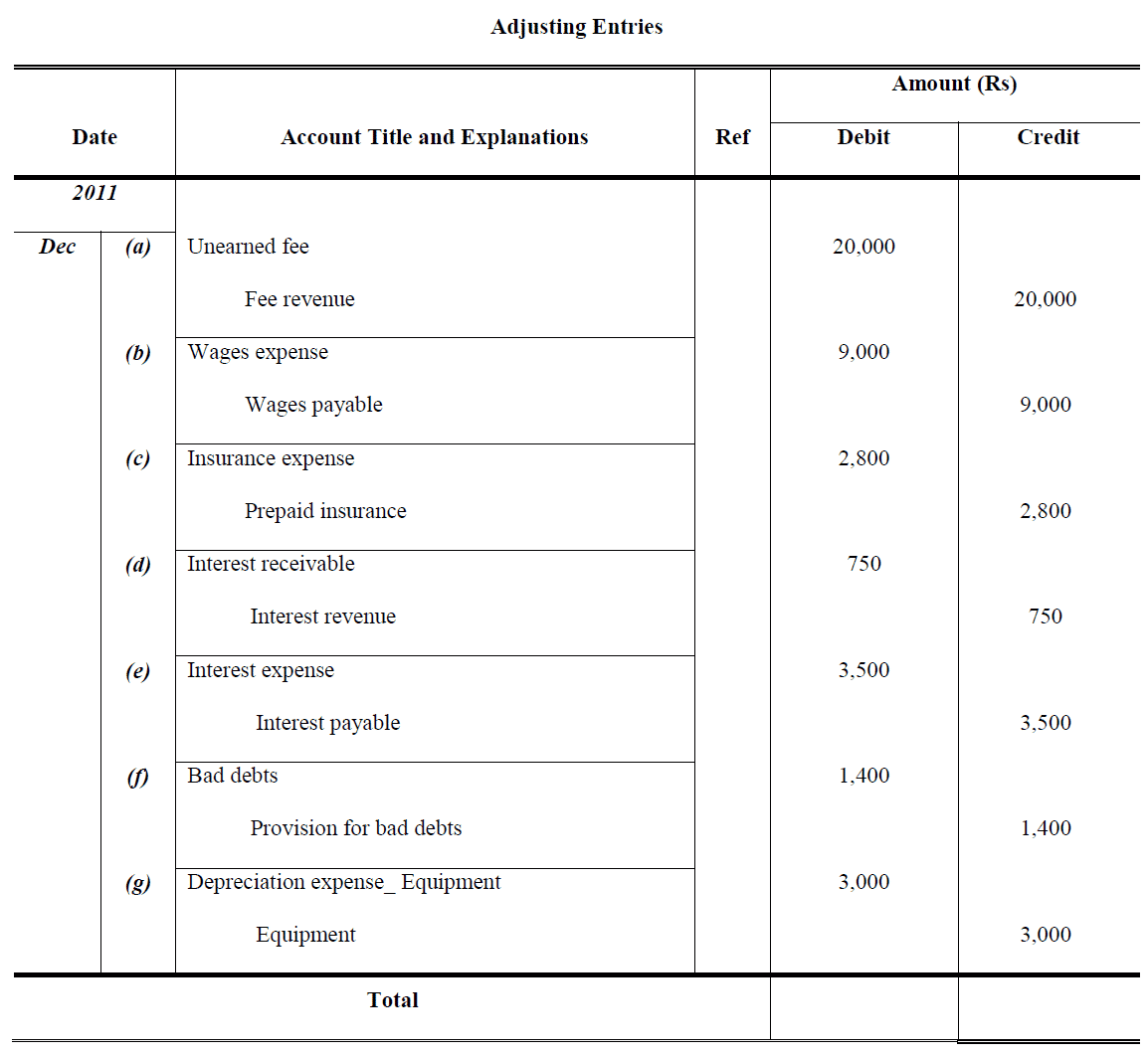

The adjusting process compares the current balance in an account to what the balance should be. An adjusting journal entry is completed to adjust the balance. Adjusting Entries are completed after all regular transactions are completed and before financial statements are created.

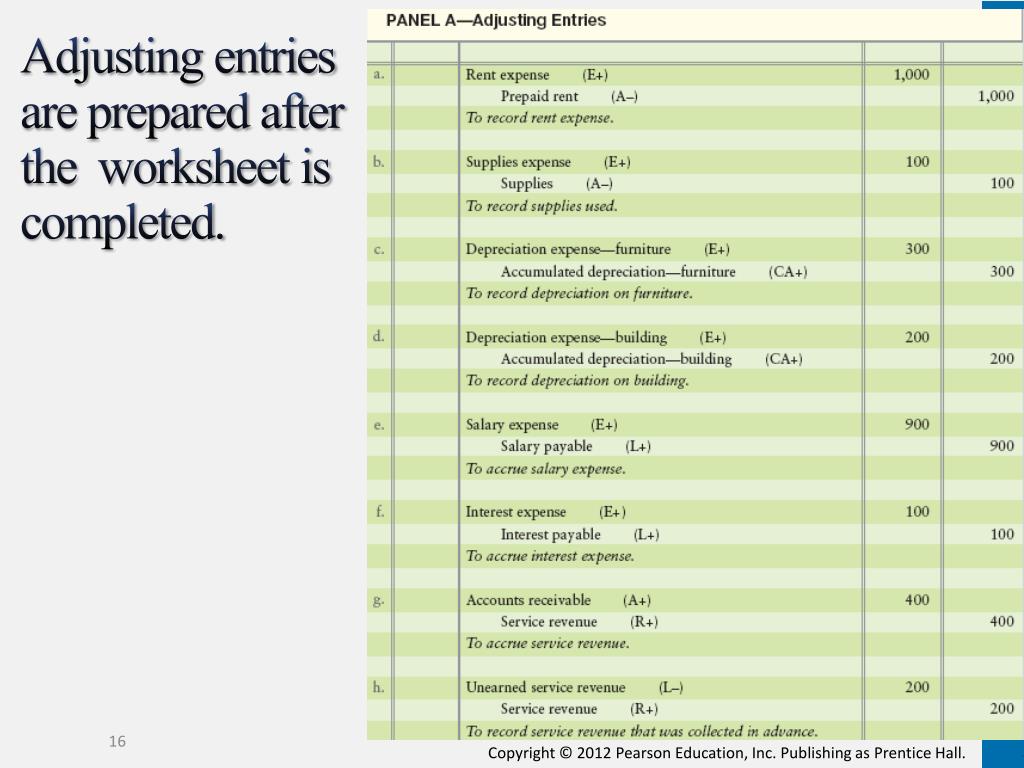

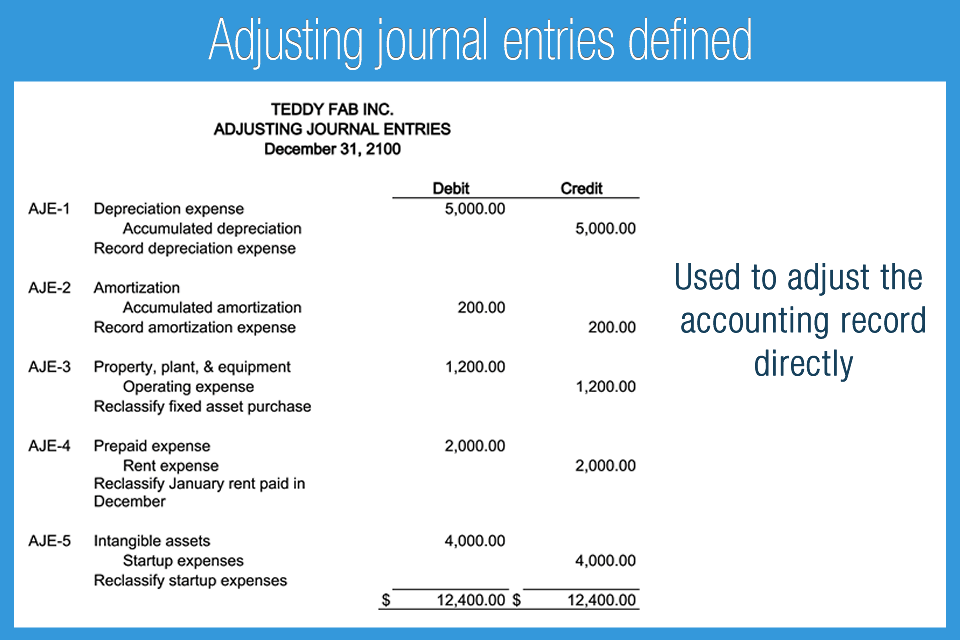

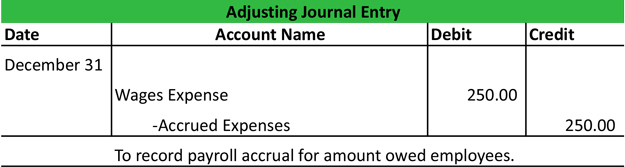

The adjusting entries for a given accounting period are entered in the general journal and posted to the appropriate ledger accounts (note: these are the same ledger accounts used to post your other journal entries). Three Adjusting Entry Rules Adjusting entries will almost never include cash. Adjusting entries in accounting: A beginner's guide 2025/01/22 Adjusting entries are journal entries made at the end of an accounting period to update various accounts before creating financial statements.

Adjusting entries, or adjusting journal entries, are journal entries made at the end of a period to correct accounts before the financial statements are prepared.