Buying a home is often seen as a single transaction, but the total cost includes more than the purchase price. Understanding the full financial picture helps buyers budget wisely and avoid surprises.

Total Additional Costs Beyond the Purchase Price

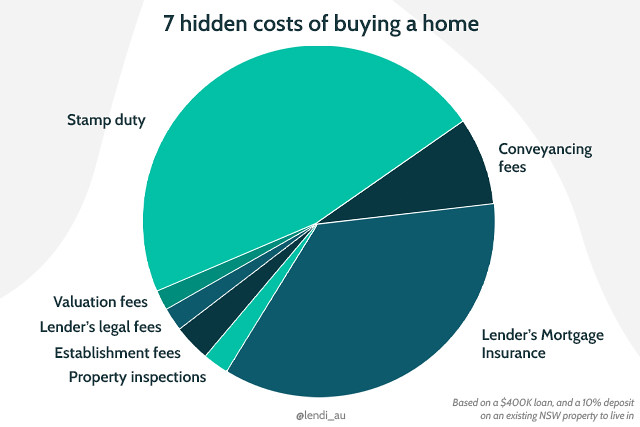

Beyond the listed price, homebuyers face significant extra expenses that can increase the total investment by 10% to 20%. These include closing costs (typically 2-5% of the home value), inspections, appraisals, title insurance, and real estate agent fees. Additional hidden costs may involve moving expenses, new insurance policies, and unexpected repairs revealed during inspections. These layers are critical to factor into your budget to prevent financial strain.

Key Hidden Costs That Add to Homeownership

While the purchase price dominates headlines, buyers should prepare for several recurring and one-time fees. Closing costs cover legal and administrative fees—averaging around 3-5% of the loan amount. Home inspections, essential for identifying structural or electrical issues, usually range from $300 to $700. Appraisals ensure the property value matches the sale price, adding $300 to $500. Title insurance protects against ownership disputes, costing $500 to $1,000. These expenses, combined with agent commissions (often 5-6% of the sale price), create a substantial financial layer beyond the home’s sticker price.

.png)

Planning for Long-Term Affordability

Anticipating these additional costs ensures realistic budgeting and long-term affordability. Allocate 1-2% of the home’s value for inspections, 3-5% for closing costs, and 1-3% for unexpected repairs. Researching local market norms and consulting with lenders or real estate professionals helps mitigate surprises. Proper planning transforms the home-buying journey from a single outlay into a well-informed investment.

Final Thoughts: Transparent Budgeting Leads to Confidence

Understanding the full spectrum of additional costs when buying a house empowers buyers to make confident decisions. By accounting for closing fees, inspections, appraisals, and other expenses, homeowners avoid financial shocks and build a sustainable foundation. Transparency today means peace of mind tomorrow—so review every cost line item with clarity and foresight.

The true cost of buying a house extends far beyond the purchase price. By recognizing and preparing for hidden expenses, buyers protect their finances and enter homeownership with clarity and confidence. Start planning now for a seamless and affordable transition into your new home.

Buying a home comes with unavoidable costs. Learn about 10 hidden costs you'll need to cover upfront-so you're prepared before you get the keys. The costs of buying a home go well beyond the actual purchase price.

Knowing these 10 costs of buying a home ahead of time can ease that check. To determine how much house you can afford, it's important to factor in all the additional expenses, such as closing costs, insurance, taxes and maintenance, before committing to a purchase. The Bottom Line The true cost of owning a home involves a lot more than just a down payment and a monthly mortgage payment.

If you're looking to buy, factor in both the upfront costs and the ongoing expenses. Always look deeper than just the sales price when shopping for how much home you can truly afford. Review the complete costs of buying a home, including down payment, closing costs and moving costs.

Plus review the ongoing costs of home ownership. These hidden costs of buying a home could leave you feeling buyer's remorse. Many underestimate the total expense of owning a home, including taxes, insurance, and other unexpected disbursements.

In fact, almost 41% of first. The average cost for a local move ranges from $900 to $2,800, while a long-distance move costs $1,300 to $9,500, depending on the distance and weight. Alternatively, moving truck rental costs $20 to $500 per day.

A real estate agent shaking hands with a couple buying a new house Ongoing / Monthly costs of owning a home. How much should I save to buy a house? It's recommended to save at least 5% of a home's purchase price to cover upfront costs like a down payment, moving expenses and closing costs. This means to buy a $300,000 home, you'd want to save up $15,000 (5%).

Additional costs may involve attorney fees for legal documentation, escrow fees for handling funds, and prepaid property taxes and homeowners insurance. Depending on the location and complexity of the transaction, these expenses when buying a house usually range from 2% to 5% of the home's purchase price.