When securing critical illness coverage, many policyholders wonder how much more they need to pay for enhanced protection that goes beyond standard benefits. Understanding the true cost and value of additional critical illness cover empowers informed decisions.

Additional Critical Illness Cover: Expanded Benefits Explained

Beyond basic coverage for common conditions like cancer or heart attack, additional critical illness cover extends protection to rare but severe illnesses such as pancreatitis, stroke complications, or autoimmune disorders. These riders often include shorter waiting periods, higher payout limits, and broader definitions, offering more timely financial relief during emotional and medical crises. The extra cost reflects the increased risk and expanded scope, but the peace of mind is invaluable.

Understanding the Cost of Extra Coverage

The additional expense for expanded critical illness protection typically ranges from 10% to 30% above your core policy premium, depending on age, health, and the number of added conditions. Factors like lifestyle, medical history, and policy duration significantly influence pricing. While upfront, this investment safeguards against catastrophic expenses during critical health events, reducing out-of-pocket burdens when they matter most.

Maximizing Value Through Tailored Add-Ons

Strategically choose additional cover based on personal risk factors—such as family history or high-stress occupations—to ensure your policy aligns with real needs. Bundling multiple riders can offer cost savings, while reviewing policy terms annually ensures optimal coverage. The goal is not just spending more, but gaining meaningful protection that strengthens your financial resilience.

Adding critical illness cover goes beyond paying extra—it’s a strategic investment in holistic health security. With clear insights into costs and tailored options, you can secure comprehensive coverage that truly protects what matters most. Start protecting more, paying smarter, and gaining confidence through enhanced policy benefits today.

Table of Contents: Critical illness insurance is often purchased to cover the financial burden of medical expenses resulting from serious illnesses. However, the amount of coverage needed depends on factors such as medical expenses, income replacement, and the diagnosis of specified illnesses. How Much Does Critical Illness Insurance Cost? The cost of critical illness insurance depends on the amount of coverage, your health, age, gender, nicotine use and how you get coverage.

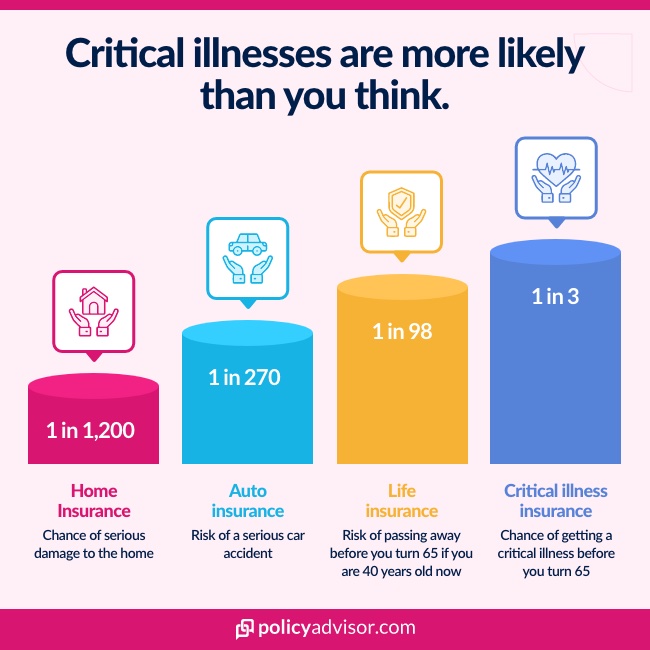

If you. Is critical illness insurance worth it? If you're at risk for cancer, a stroke or another critical illness, here's how you could benefit from coverage. Exactly how much your critical illness plan pays out will depend on your insurance provider and the type of plan you've selected.

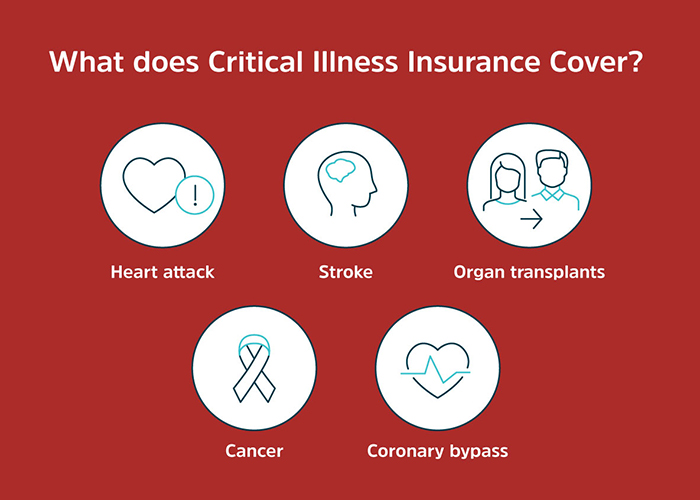

What does critical illness insurance typically cover? Critical illness plans are designed to provide coverage for illnesses and injuries that have a significant impact on your quality of life. Critical Illness insurance provides a lump. Learn about critical illness insurance, what it is, how it works, and why it is worth it.

Choose Anthem for your individual and family insurance coverage today. Learn how much critical illness cover you really need, what it pays for, & how to choose the right policy for your lifestyle, income, & health needs. Discover the importance of critical illness insurance.

Learn what it covers, how it works, and if you need it. Get insights to make an informed decisions. Critical Illness Insurance Costs and Benefits Critical Illness Insurance Costs and Benefits If you suddenly get a critical illness, you might not be prepared to cover out-of-pocket medical costs.

Luckily, a critical illness insurance plan can help. This policy type is designed to help provide coverage for critical illnesses. What is critical illness insurance? Critical illness insurance is a type of policy that provides a lump-sum payment if you're diagnosed with a serious illness covered by your policy.

It can help you financially when you need it most by covering medical expenses and other costs at a time in which health insurance is likely to fall short.