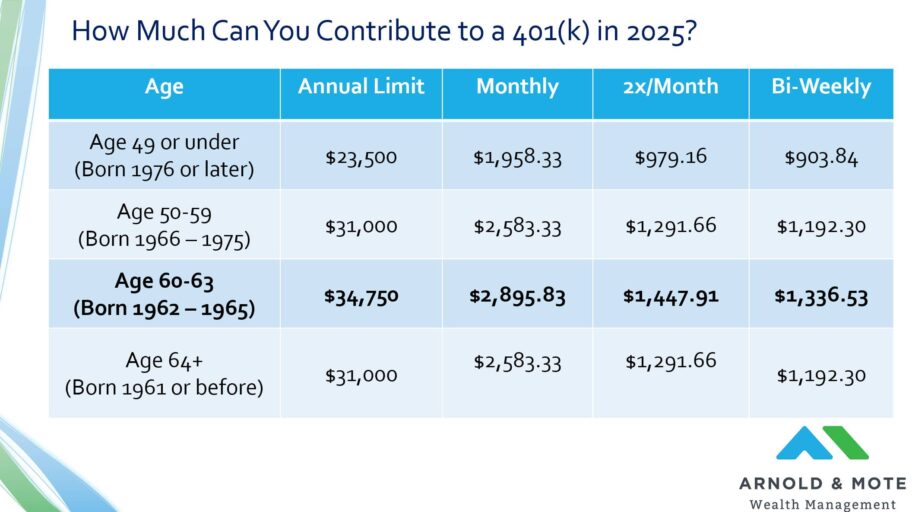

A major highlight for 2025 is the enhanced catch-up contribution limits for individuals ages 60 to 63. If you're in this age group, you can now contribute up to $11,250 to your 401 (k), 403 (b. For 2025, you can defer up to $23,500 into your 401 (k), and workers age 50 and older can make an extra $7,500 in catch-up contributions.

Starting this year, workers age 60 to 63 can make "super. A super catch-up contribution, originating from the SECURE 2.0 Act of 2022, is a higher catch-up contribution amount that's available to you if you're age 60 to 63 and are enrolled in a participating retirement plan. Super catch.

The IRS sets the maximum that you and your employer can contribute to your 401 (k) each year. For tax year 2025, the most you can contribute to a Roth 401 (k), a traditional 401 (k), or a combination of the two is $23,500. For 2026, this rises to $24,500 for 2026.

Those 50 and older can contribute an additional $7,500 in 2025, and $8,000 in 2026. As the IRS noted, employees younger than 50 have an annual contribution limit of $23,500 in 2025, up from $23,000 last year. With the super funding option, employees 60-63 can now contribute up to $34,750 a year.

If you're behind on your retirement savings, now is a good time to take advantage of the higher contribution limits. If you're age 50 or older, you are eligible to make additional contributions to your 401 (k). There are even "super" catch.

IR-2025-111, Nov. 13, 2025 - The Internal Revenue Service announced today that the amount individuals can contribute to their 401 (k) plans in 2026 has increased to $24,500, up from $23,500 for 2025. The intel on catch-up contributions Each year, the IRS releases updated guidance on how much individuals can contribute to their 401 (k)s.

The Secure 2.0 Act introduced additional changes to retirement savings, in particular, the "super-catch-up" contribution provision. Effective January 1, 2025, this provision makes it possible to contribute more toward your retirement in the years that you are age 60. They can contribute up to $11,250 next year - an additional $3,750 in catch-up contributions - beyond the general 2025 deferral limit of $23,500, the Internal Revenue Service said.