Maximizing your super contribution can significantly boost long-term retirement savings, but determining the right amount often feels overwhelming. Understanding how much additional super to contribute ensures you’re balancing current needs with future security.

How Much Additional Super Should I Contribute in Practice?

The optimal additional super contribution varies by income level, employment status, and retirement timeline. On average, contributing 10% to 15% of your gross income is recommended for steady growth, though increasing to 15%–20% may accelerate retirement readiness. Factors like employer matching, tax advantages, and personal financial health influence this decision—start with employer guidelines and assess how much can be comfortably allocated without strain.

Employer Matching as a Free Incentive

Many employers offer free super through matching contributions, effectively adding 3%–6% for every dollar you contribute up to a cap. Contributing at least enough to capture full employer match is critical, as forfeiting this benefit reduces long-term gains. Evaluate your company’s policy and adjust your contributions accordingly to maximize this immediate return.

Balancing Risk and Return with Additional Contributions

Beyond employer matches, additional super should align with your risk tolerance and time horizon. Younger contributors may afford higher percentages for growth, while those nearing retirement might prioritize stability. Consider consulting a financial advisor to tailor contributions that balance investment risk with steady accumulation, ensuring contributions enhance—not hinder—overall financial well-being.

Measuring Impact: Projected Growth vs. Current Contribution

Using retirement calculators, even small increases in super contributions can yield substantial long-term gains. For example, adding 2% annually over 30 years with 7% average returns may add over $200,000 to your nest egg. Regularly review and adjust your contribution level based on salary changes, life events, and market conditions to stay on track toward financial goals.

Determining your ideal additional super contribution involves aligning personal finances, employer benefits, and retirement aspirations. Start with employer matching, assess your risk profile, and adjust as needed—small, consistent increases can transform your financial future. Begin evaluating your current contribution today to unlock greater long-term value.

Adding to your super You can boost your retirement savings by making voluntary super contributions, such as by: setting up a salary sacrifice arrangement with your employer making personal super contributions (and a non-concessional contribution may make you eligible for the government's super co-contribution) transferring any super you have in a foreign super fund arranging for your spouse to. If you're considering putting more money into your super, and want to know more about how the whole system works, here are the basics. Check you're being paid the right amount of super, and find out how to make extra, voluntary contributions yourself.

Making extra super contributions will build your retirement nest-egg, as well as provide immediate and long-term tax benefits. So, what are extra super contributions and how much extra super contributions can you make? Super co-contributions If you earn less than $60,400 a year and make an after-tax contribution to your super in 2024-25, the Government may add up to $500 extra to your super, if you're eligible.

This calculator can help you: Work out how much your contributions may benefit your super balance. Discover the most effective way to contribute to your super based on current information. Work towards a retirement goal.

Before you start, here are some things to think about: How much you can spare to contribute to your super. When you'd like to retire. A retirement goal.

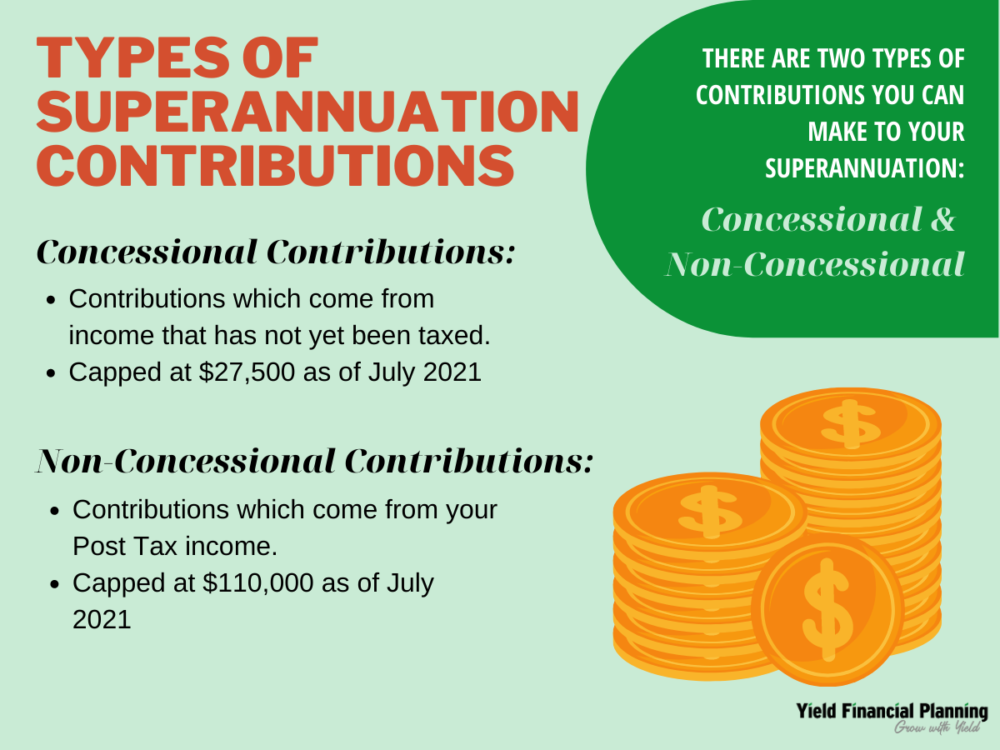

It's important to. Find out how much you can contribute to your superannuation (super) fund each year without paying extra tax. Learn about the different types of contributions and how they are taxed.

Use Australian Retirement Trust's super contributions calculator to see how adding more into your super could grow your balance and reduce your tax. It's basically a way to minimise your tax bill. When you salary sacrifice, you arrange with your employer to contribute an additional amount to your super out of your pre.

How to make personal super contributions, including claiming a tax deduction so they are concessional contributions.