Navigating the nuances of NIC contributions can be challenging, but understanding how much additional NIC contributions entail is key to responsible financial management for employers and employees alike.

How Much Are Additional NIC Contributions?

Additional NIC contributions refer to surcharges imposed beyond standard NIC rates, often required for specific employee benefits or regulatory adjustments. Typically, the standard NIC rate stands at 13.8% for employees and 13.8% for employers, but additional contributions may range from 0.5% to 2.5%, depending on the jurisdiction and benefit scheme. These vary by country and employment type, so consulting local guidelines is essential for accurate planning.

Factors Influencing Additional NIC Contributions

Several elements determine the final amount, including local tax laws, employee eligibility, and whether voluntary benefits are added. For example, some regions impose extra charges for extended healthcare or retirement contributions, increasing total NIC obligations. Employers must stay updated on regulatory changes to avoid penalties and ensure transparency in payroll processing.

Why Knowing These Costs Matters

Accurately calculating additional NIC contributions supports precise budgeting and compliance. Miscalculations can lead to unexpected expenses or legal risks. Whether expanding benefits or adjusting payroll, understanding the full scope empowers informed decisions, fostering trust and financial stability for both employers and employees.

Next Steps for Employers and Employees

Review your payroll system and consult tax advisors to clarify how much additional NIC contributions apply to your situation. Stay proactive with updates from government portals to maintain compliance and optimize your financial planning strategies.

Clarifying how much are additional NIC contributions ensures transparency and accuracy in payroll. By understanding the factors and staying compliant, employers and employees can manage costs effectively and build long-term financial confidence.

National Insurance contributions you can choose to pay when you have a gap in your National Insurance record. If you're aged between 45 and 73(ish), buying extra national insurance years could massively boost your state pension. If it works for you, the returns can be huge.

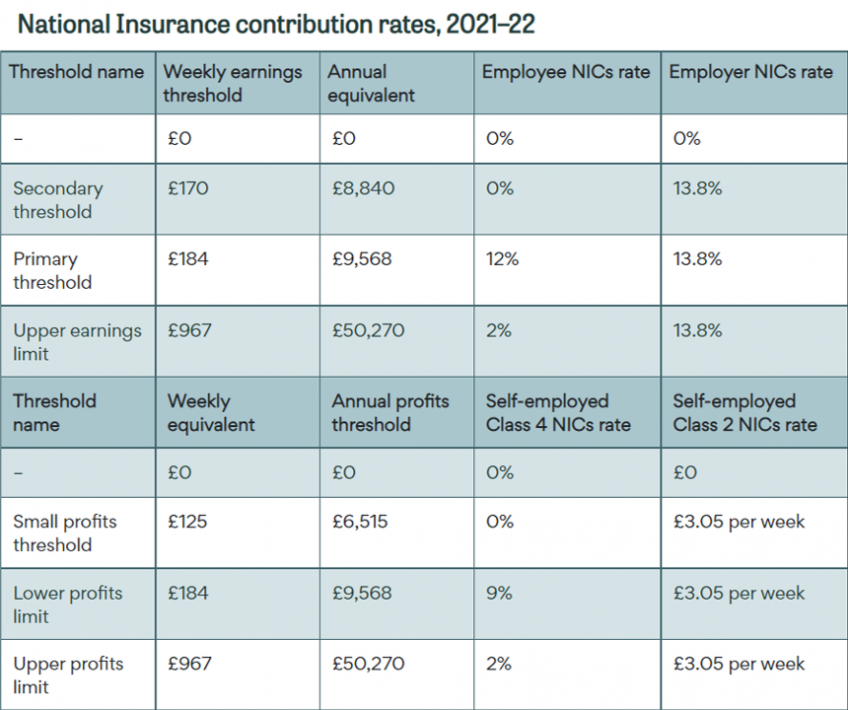

National Insurance contribution rates%2C 2021–22.png?itok=iGs8c8Ix)

about who should do it, and how to do it. However, there are various scenarios where buying voluntary NI contributions might not be beneficial - for example, if you were 'contracted out' of the additional state pension before 2016. This meant you paid a lower rate of NI (and therefore received a lower state pension) in exchange for a higher contribution to your private pension.

A guide to Class 3 NI contributions. Learn costs, deadlines & whether topping up missing years could boost your State Pension from Abode Financial Planning. You usually need 35 qualifying years of National Insurance (NI) contributions to get the full State Pension.

If you don't have enough, you can pay to fill gaps in your record to boost how much you get - even if you're already getting your State Pension. Here's what to do, including how to pay voluntary NI contributions online. in our article Deadline to boost State Pension extended to April 2025.

Buying extra years involves paying what are known as 'voluntary class 3 NI contributions', and the rate is currently £907.40 for a full year (£17.45 per week), which will boost your State Pension by around £302 a year (£5.82 a week). Topping up your pension contributions can be very lucrative, and below we discuss some of the considerations you should make. Why top up your National Insurance record? How many full National Insurance qualifying years you have is important, as it goes some way to determining how much state pension you will receive when you retire.

Free UK National Insurance calculator. Calculate Class 1, 2, 3, and 4 NI contributions for employees, self-employed, and employers in 2025/26 tax year. Information about National Insurance contributions, qualifying for the State Pension, understanding your National Insurance record and whether you should fill gaps in your record.

How much does it cost? Making up for one year of missed NI contributions will cost you up to £907.40 (2024/25), which will add about £302.64 per year (£5.82 per week) to your pre-tax State Pension. There might be occasions where you don't need to pay the full amount.