Navigating the path to homeownership often involves understanding the intricate relationship between your financial standing and the physical property you wish to acquire. A question that frequently arises, particularly for first-time buyers and investors, is what the minimum apartment size for mortgage approval typically is. While there is no single, universal number enforced by every lender, the reality is that property size plays a significant role in the risk assessment process, influencing everything from loan-to-value ratios to a bank's willingness to finance your dream.

The Lender's Perspective: Risk Assessment and Property Value

Banks and mortgage institutions are fundamentally in the business of managing risk. When they approve a loan, they are securing an asset against the borrowed money; if the borrower defaults, the property is repossessed and sold to recover the debt. Consequently, the size and desirability of an apartment directly impact its marketability and resale value. A larger property generally commands a higher price point, which provides the lender with a more substantial buffer, or loan-to-value (LTV) ratio, should they need to repossess and sell the unit.

How Size Influences LTV Ratios

The loan-to-value ratio is a critical metric for lenders. It is calculated by dividing the loan amount by the property's value. A smaller apartment might struggle to meet a lender's preferred LTV threshold, often capped at 80% or lower for prime loans. If a property is deemed too small, it may be classified as a high-risk asset because it could be harder to sell quickly or might not fetch a price high enough to cover the outstanding loan, leading lenders to either deny the application or require a larger deposit.

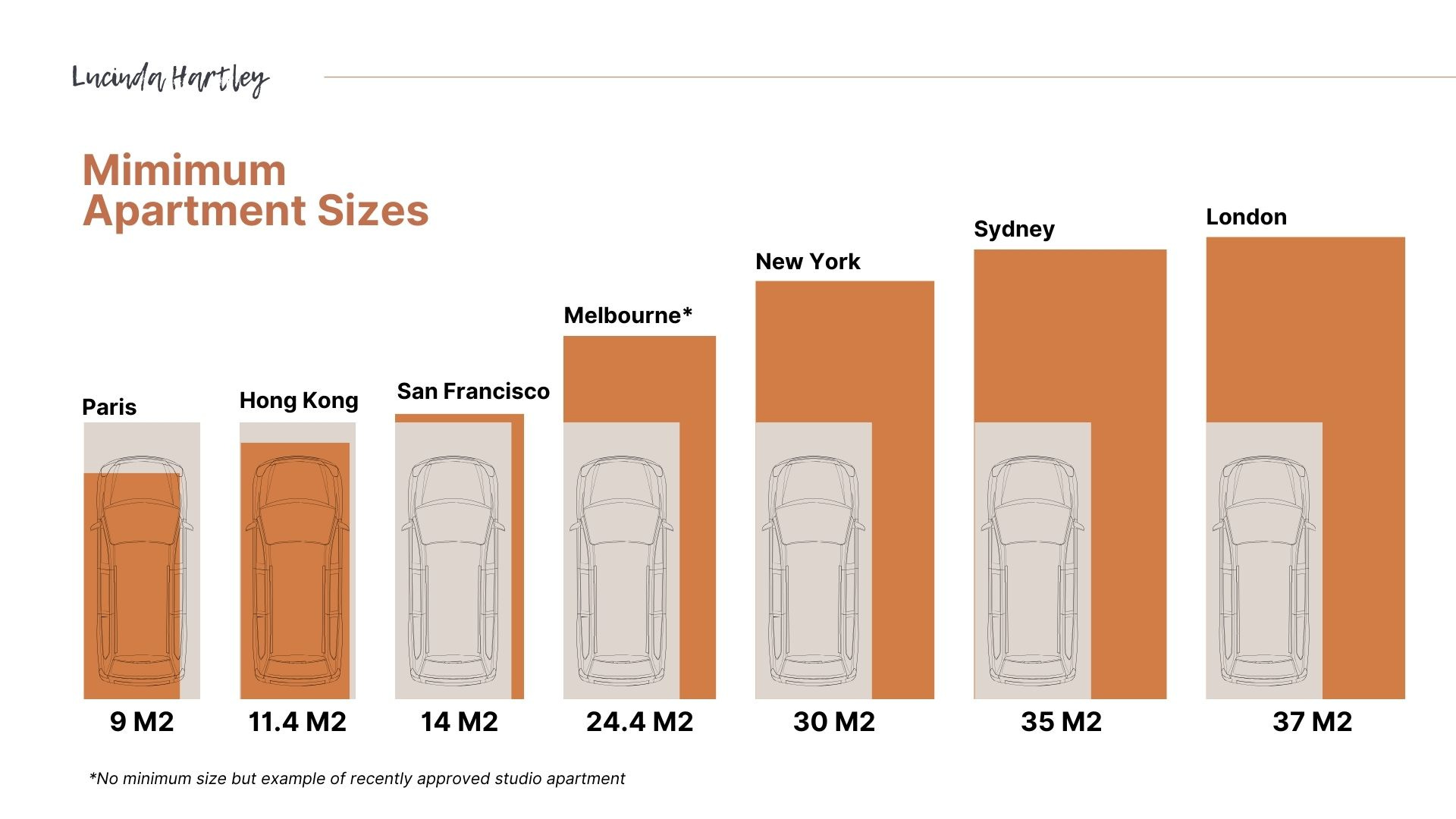

Market Standards and Typical Thresholds

While regulations vary by country, most major financial centers have established market standards that act as de facto minimums. In many urban areas, the threshold for a "standard" residential mortgage often falls around 30 to 40 square meters (approximately 320 to 430 square feet). Apartments below this size are frequently categorized as "micro-units" or studio conversions, which can trigger stricter lending criteria.

- Below 30 sqm (323 sq ft): Typically requires specialist lenders or non-standard mortgages, often with higher interest rates.

- 30–45 sqm (323–484 sq ft): Considered the absolute minimum range for standard mortgage products.

- 45+ sqm (484+ sq ft): Generally offers the widest selection of lenders and most favorable terms.

The Role of Location and Desirability

Size alone does not dictate mortgage approval; location is an equally powerful factor. A compact apartment in a highly sought-after neighborhood with strong transport links and excellent amenities might be easier to finance than a larger unit in a developing or remote area. Lenders assess the "re-saleability" of the property, and a desirable small apartment in a prime location often carries less risk than a larger property in a stagnant market.

Style and Functionality

Not all square meters are created equal, and the layout of the apartment can impact its mortgage eligibility. A well-designed studio with a separate kitchen and a distinct living area may be viewed more favorably than a cramped one-bedroom where the living room and bedroom flow directly into the kitchen. Banks look for evidence of efficient space utilization; a property that feels spacious and functional is easier to value and sell than one that appears inefficient or poorly planned.

Documentation and Valuation Requirements

Securing a mortgage for a smaller property usually involves rigorous valuation processes. Lenders will require a formal property appraisal to confirm the square footage and ensure the stated size is accurate. You will need to provide evidence such as floor plans or architectural certificates. If the size is misreported, the lender may immediately withdraw their offer, making transparency and accurate measurement essential steps in the application process.

Strategic Considerations for Buyers

If you are set on purchasing a property below the typical size threshold, strategic planning is essential. Buyers should consider increasing their deposit to lower the LTV ratio, demonstrating to the lender that they are taking on less risk. Alternatively, exploring specialized lenders who focus on non-standard properties or renovation loans can be a viable path, though these often come with higher interest rates or fees. Ultimately, understanding the minimum apartment size for mortgage involves balancing your budget with market realities to find a property that is both affordable and financeable.